Visa Inc. (V) vs. Mastercard Inc. (MA): Which Is the Better Buy in 2026?

Visa and Mastercard remain the duopoly of global finance. We break down the growth, margins, and risks to see which stock leads the pack in 2026.

The matchup

Visa and Mastercard operate as the primary rails for global commerce, maintaining a combined market cap exceeding $1 trillion. Both firms leverage massive network effects, with Visa processing transactions across 130 million merchant locations globally.

Mastercard has shifted its strategy toward a network of networks approach, integrating stablecoin infrastructure and real-time payment rails. This pivot aims to capture volume beyond traditional credit card processing, which faces increasing scrutiny from regulators.

- Visa (V) market capitalization: $581.54 billion.

- Mastercard (MA) market capitalization: $442.93 billion.

- Visa operating margin: ~67%.

- Mastercard adjusted operating margin: ~60.8%.

Numbers side by side

Valuation metrics for both firms remain elevated, reflecting their status as high-quality compounders. Mastercard trades at a slightly higher P/E ratio, reflecting investor confidence in its faster revenue growth and higher-yielding cross-border services.

Visa offers a more defensive profile with lower beta, making it a preferred choice for investors prioritizing stability during market volatility. Both companies continue to return significant capital to shareholders through aggressive buybacks and consistent dividend growth.

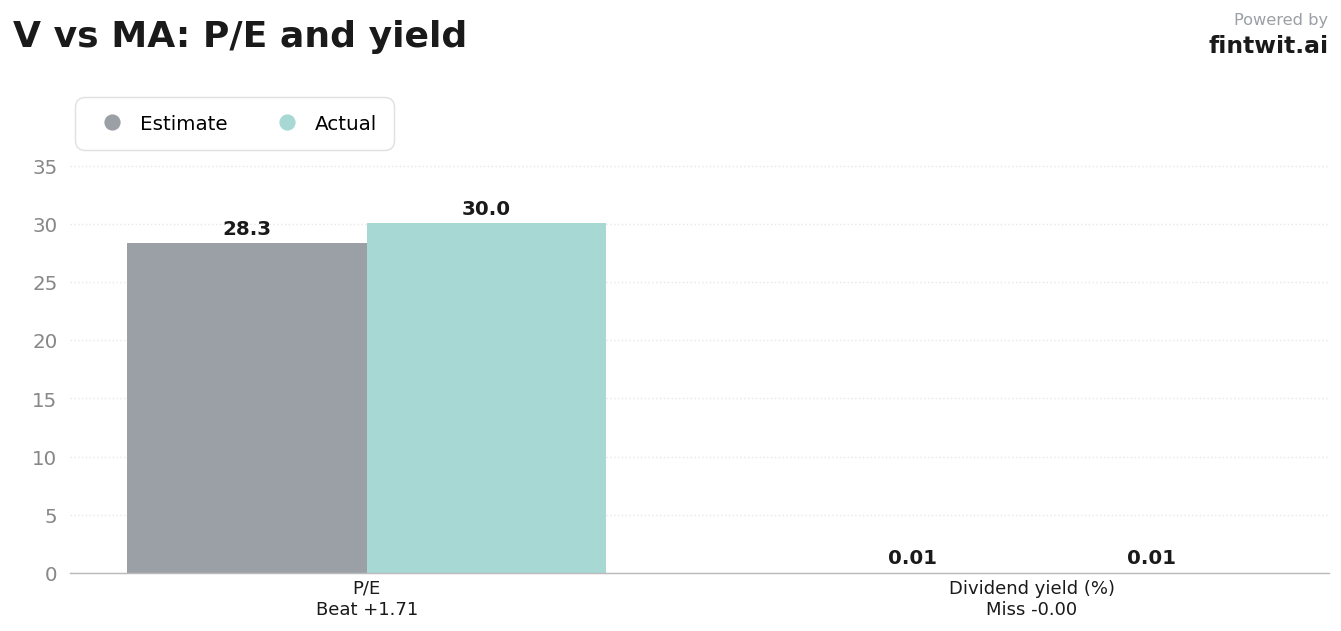

- Visa P/E Ratio: 28.32.

- Mastercard P/E Ratio: 30.03.

- Visa 1-year price performance: -10.33%.

- Mastercard 1-year price performance: -14.54%.

- Visa dividend yield: 0.84%.

- Mastercard dividend yield: 0.64%.

Bull and bear on each

Visa's bull case centers on its unmatched global scale and the expansion of its value-added services, which grew 33% YoY. Conversely, the bear case highlights the Credit Card Competition Act and the threat of alternative payment methods like account-to-account transfers.

Mastercard's bull case is driven by its superior growth in cross-border transactions and its strategic acquisition of stablecoin infrastructure. The primary bear case involves its higher exposure to geopolitical tensions and potential margin compression if enterprise spending slows.

- Visa Bull: Dominant B2B and cross-border whitespace.

- Visa Bear: Regulatory pressure on interchange fees.

- Mastercard Bull: High-margin value-added services up 22% YoY.

- Mastercard Bear: Sensitivity to cross-border volatility.

- Truist Securities analyst Matthew Coad rates both as Buy, with targets of $371 for Visa and $561 for Mastercard.

The verdict

The choice between these two giants depends on an investor's preference for scale versus growth velocity. Mastercard's ability to integrate new payment rails provides a more dynamic outlook, while Visa remains the bedrock of global financial infrastructure.

Investors should monitor how regulatory developments impact interchange fees in the coming quarters. Both companies demonstrate the ability to maintain high margins despite macroeconomic headwinds.