Costco Wholesale Corp (COST) Q3 Earnings Preview: What to Watch

Costco (COST) enters Q3 earnings with a 65% probability of a beat, but premium valuation leaves little room for error. Here is the data you need.

The setup

Costco Wholesale Corp (COST) is set to report its fiscal third-quarter results on May 28, 2026, after the market closes. Investors are focused on whether the company can sustain its high-single-digit to low-double-digit revenue growth while navigating a complex macroeconomic environment.

The company maintains a focus on its core value-driven model, prioritizing long-term membership loyalty over short-term margin maximization. Management continues to emphasize international expansion and digital investments to capture market share from competitors.

Market participants are particularly sensitive to the stock's premium valuation. Even strong operational results may trigger a sell-the-news reaction if guidance fails to exceed high expectations.

- Oppenheimer analyst Rupesh Parikh Parikh maintains an Outperform rating with a $1,160 price target, citing potential short-term friction from fuel margins.

- Bank of America analyst Christopher Nardone reiterates a Buy rating and $1,185 target, highlighting steady traffic from higher-income consumers.

- BTIG Research maintains a Buy rating with a $1,115 target, reflecting confidence in the long-term growth trajectory.

- Inflation and potential tariff policies remain key macro risks that could pressure merchandise margins.

- Geopolitical tensions in the Middle East continue to impact global shipping schedules and energy costs.

Consensus numbers

Wall Street consensus estimates for the third quarter reflect continued operational resilience. The company has a history of exceeding expectations, as demonstrated by its performance in the previous three quarters.

Investors should monitor the gap between reported figures and these consensus targets to gauge the market's reaction. The following data points represent the current expectations for the upcoming release.

- EPS Estimate: $4.98 per share.

- Revenue Estimate: $69.61 billion.

- Beat Probability: 65% chance of beating, 25% chance of missing, 10% chance of meeting expectations.

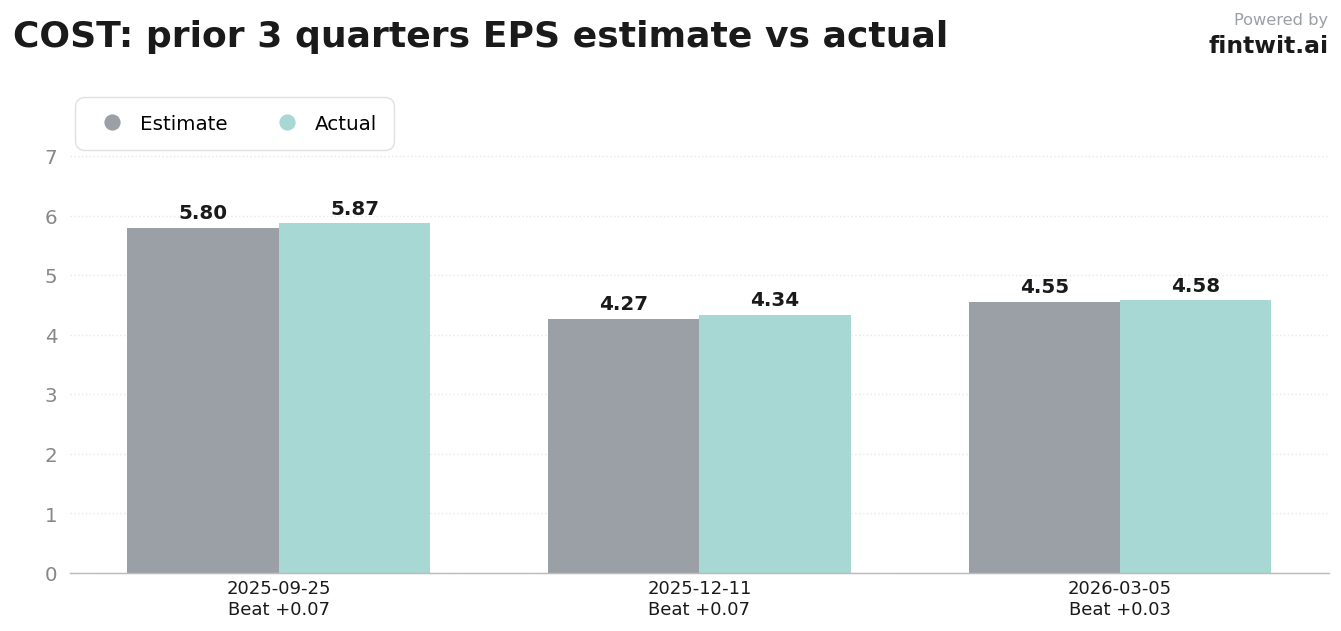

- Q1 2026 Performance: $5.87 EPS vs $5.80 estimate; $86.16 billion revenue.

- Q2 2026 Performance: $4.34 EPS vs $4.27 estimate; $67.31 billion revenue.

- Q3 2026 Performance (Prior Quarter): $4.58 EPS vs $4.55 estimate; $69.60 billion revenue.

What we'll watch on the call

The earnings call will provide critical insight into the health of the membership model and the efficiency of digital operations. Analysts are looking for specific commentary on how rising fulfillment costs are impacting operating margins.

Management's tone regarding consumer spending patterns will be scrutinized for any signs of softening. Any updates on capital return programs, such as potential special dividends or stock splits, will also be a major focal point for retail investors.

- Membership Fee Income: Monitoring renewal rates, which have historically remained above 90%.

- E-commerce Growth: Assessing the sustainability of recent double-digit growth in digitally enabled sales.

- Fuel Operations: Evaluating the impact of fuel price volatility on foot traffic versus margin compression.

- Operating Margins: Tracking the impact of rising fulfillment costs for online orders.

- Consumer Spending: Identifying any shifts in purchasing behavior among higher-income demographics.

Fintwit's AI verdict

The quantitative models suggest that Costco remains a standout in the consumer defensive sector, supported by a loyal member base and consistent traffic. While the valuation is undeniably stretched compared to historical averages, the company's ability to execute on its core value proposition provides a unique buffer against broader market volatility.

Investors should weigh the high probability of an earnings beat against the risk of a market correction if the forward guidance does not provide enough upside to justify the current multiple. The data indicates that the market is pricing in near-perfection, leaving little room for operational hiccups in the upcoming report.