Ciena Corp (CIEN) Q2 2026 Earnings Preview: What to Watch

Ciena enters Q2 2026 with strong AI momentum. We break down the consensus estimates, key segment drivers, and the $7 billion backlog.

The setup

Ciena is positioned as a primary beneficiary of the ongoing surge in hyperscaler capital expenditure. The company's role as a provider of critical optical interconnects has made it a central player in the build-out of AI-optimized data centers.

Management previously raised its full-year 2026 revenue guidance to a range of $5.9 billion to $6.3 billion. This optimism is underpinned by a record backlog of approximately $7 billion, which continues to provide visibility into future revenue streams.

Despite this demand, supply chain constraints remain a persistent bottleneck for the industry. Investors are focused on whether Ciena can successfully convert its massive order book into actual revenue during the second quarter.

- Hyperscaler AI infrastructure spending remains the primary macro tailwind for the firm.

- Ongoing industry-wide component shortages continue to limit production capacity.

- Gross margins are targeted between 43.5% and 44.5% for the fiscal year.

- Secondary risks include potential macroeconomic slowdowns affecting enterprise and service provider budgets.

Consensus numbers

Wall Street analysts have adjusted their expectations upward to reflect the company's strong positioning in the AI networking space. Recent price target hikes from major firms underscore the bullish sentiment surrounding the upcoming print.

The following analyst targets highlight the current market optimism:

TD Cowen raised its price target to $675 from $425.

Citi maintained a Buy rating and increased its target to $658 from $345.

Stifel lifted its price target to $585 from $430.

- EPS Estimate: $1.46 per share.

- Revenue Estimate: $1.50 billion.

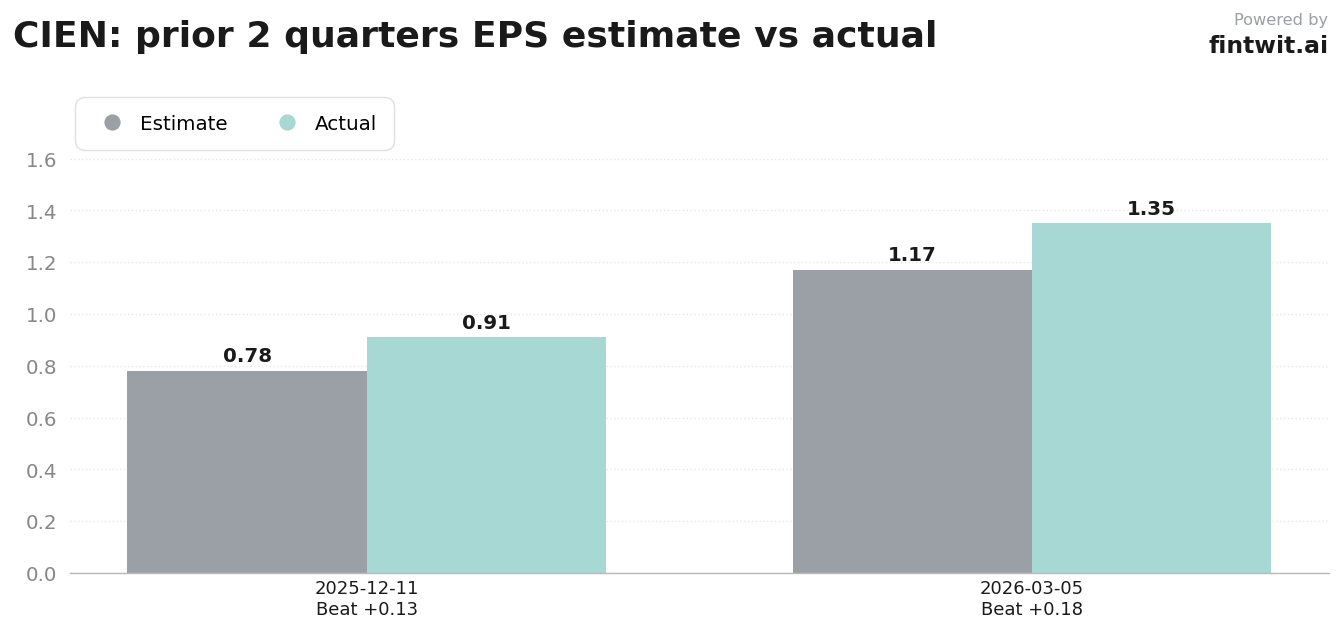

- Q1 2026 Actual EPS: $1.35 (vs $1.17 estimate).

- Q4 2025 Actual EPS: $0.91 (vs $0.78 estimate).

- Networking Platforms segment accounts for approximately 80% of total revenue.

What we'll watch on the call

The primary focus for investors will be the execution of the $7 billion backlog. Management's ability to navigate component availability will dictate the pace of revenue recognition for the remainder of the fiscal year.

Product mix shifts are also under scrutiny, particularly the adoption rate of WaveLogic 6 technology. Analysts want to see if this high-margin product can offset competitive pressures and maintain gross margin targets.

Visibility into the second half of 2026 is another critical data point. Any commentary regarding changes in hyperscaler spending patterns will be treated as a leading indicator for the broader optical networking sector.

- Supply chain impact on converting the $7 billion backlog into realized revenue.

- Current visibility into hyperscaler spending patterns for the second half of 2026.

- Gross margin sustainability amid potential product mix shifts.

- Adoption rates of WaveLogic 6, RLS, and 800G pluggables.

- Performance of the Global Services segment as a contributor to overall profitability.

Fintwit's AI verdict

The quantitative models tracking Ciena's performance suggest a favorable outlook heading into the June 4 print. The combination of consistent earnings beats and a massive, multi-billion dollar backlog provides a cushion that few peers in the networking space can match.

While supply chain volatility remains a factor, the structural demand for AI-optimized interconnects appears to outweigh near-term production hurdles. The market is pricing in a significant growth trajectory, and the upcoming report will serve as a test of whether the company can meet these elevated expectations.