Broadcom Inc (AVGO) Q2 Earnings Preview: What to Watch

Broadcom reports fiscal Q2 2026 earnings on June 3. Analysts expect $2.40 EPS as AI semiconductor demand remains the primary driver for the $1.47T firm.

The setup

Broadcom enters its June 3 earnings call with significant momentum in its AI semiconductor business. The company has previously signaled a long-term outlook for AI chip revenues exceeding $100 billion by 2027.

Management's prior guidance for Q2 revenue sits at approximately $22 billion with adjusted EBITDA margins targeted at 68%. Investors are looking for confirmation that the custom ASIC and networking silicon segments can maintain this trajectory.

- Broadcom market capitalization currently stands at $1.47 trillion.

- Management previously guided for $10.7 billion in AI semiconductor revenue for the current quarter.

- Analysts at HSBC, led by Frank Lee, recently raised their price target to $600.

- TD Cowen analyst Joshua Buchalter maintains a Buy rating with a $500 price target.

Consensus numbers

Market expectations are aggressive, reflecting the high growth profile of the company's custom silicon and networking divisions. Broadcom has consistently outperformed earnings estimates over the last two quarters.

The Semiconductor Solutions segment is projected to be the primary growth engine, with revenue expected to reach $14.8 billion, representing a 76% increase year-over-year.

- Consensus EPS estimate: $2.40.

- Consensus revenue estimate: $22.11 billion.

- Infrastructure Software revenue expectation: $7.2 billion, up 9% year-over-year.

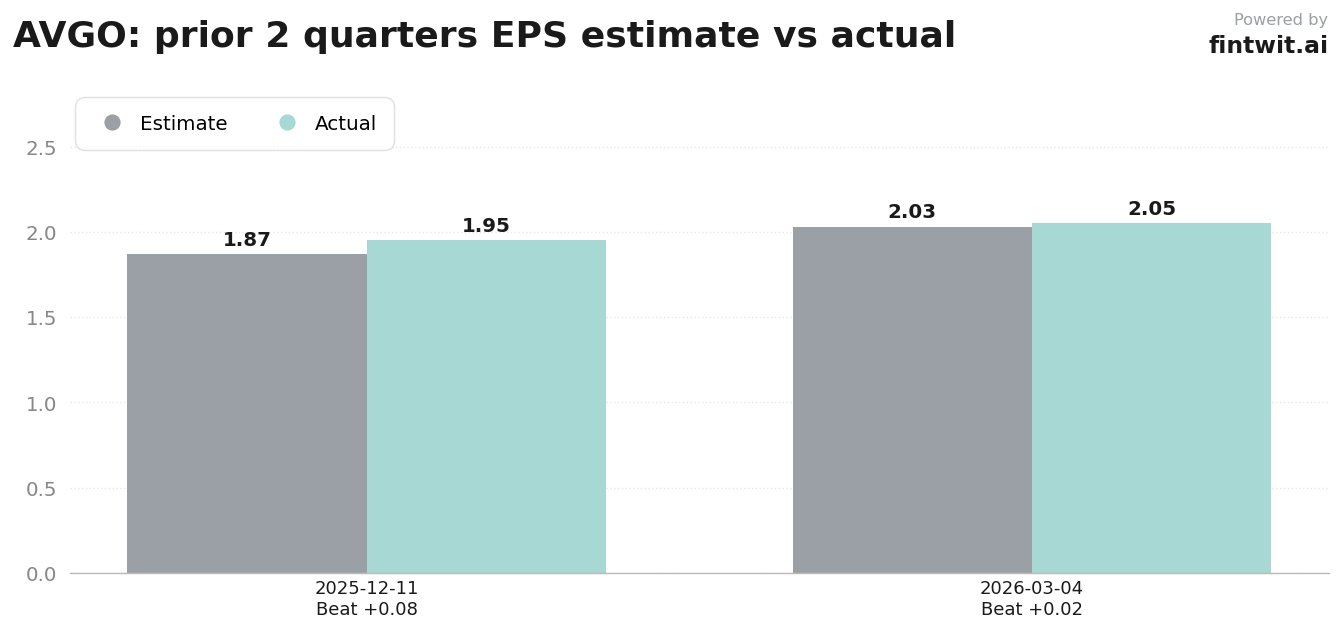

- Historical Q4 2025 EPS: $1.95 actual vs $1.87 estimated.

- Historical Q1 2026 EPS: $2.05 actual vs $2.03 estimated.

What we'll watch on the call

The primary focus remains on the sustainability of hyperscaler capital expenditure. Analysts are scrutinizing whether the current pace of investment in AI infrastructure will persist through the second half of 2026.

Integration progress regarding VMware is another critical line item. The market is looking for evidence that Broadcom is successfully monetizing its software stack within enterprise AI environments.

- Can Broadcom sustain outsized AI chip growth amid investor concerns regarding hyperscaler ROI?

- Are there signs of share erosion in custom silicon or networking against internal hyperscaler efforts?

- What is the latest outlook for AI semiconductor demand beyond 2026?

- How is the company managing global semiconductor supply chain resilience for high-end components?

- What is the impact of macroeconomic sensitivity on non-AI business segments like enterprise storage?

Fintwit's AI verdict

The sentiment surrounding Broadcom remains heavily skewed toward its dominant position in the AI hardware ecosystem. Institutional analysts continue to adjust their models upward, citing the company's unique ability to capture value from both custom silicon accelerators and high-speed networking.

While valuation concerns persist, the underlying growth metrics in the semiconductor segment provide a strong foundation for the current outlook. Investors are waiting to see if management can provide further clarity on the long-term scaling of its accelerator programs.