Broadcom Inc (AVGO) Q2 Earnings Preview: What to Watch

Broadcom enters its fiscal Q2 2026 earnings report with significant momentum. We break down the key AI metrics and analyst expectations.

The setup

Broadcom continues to leverage its dominant position in custom AI accelerators and networking infrastructure to drive growth. The market is focused on whether the company can sustain its aggressive AI revenue targets amid shifting hyperscaler capital expenditure budgets.

Management previously guided for Q2 revenue of approximately $22.0 billion. Investors are looking for confirmation that the company can maintain an adjusted EBITDA margin of roughly 68%.

- Frank Lee at HSBC raised his price target to $600, citing potential for AI revenue to exceed Street expectations in the second half of fiscal 2026.

- Christopher Rolland at Susquehanna maintains a Buy rating but adjusted his fiscal 2026 AI revenue estimate to $55 billion from $62.5 billion.

- Rick Schafer at Oppenheimer forecasts a 30% quarter-over-quarter increase in the AI segment, driven by demand for custom ASICs.

Consensus numbers

Wall Street consensus estimates point to a strong quarter, reflecting year-over-year growth of approximately 47-52%. The company has a history of exceeding expectations in recent quarters.

The following figures represent the current market consensus for the fiscal Q2 2026 report.

- EPS Estimate: $2.40

- Revenue Estimate: $22.11 billion

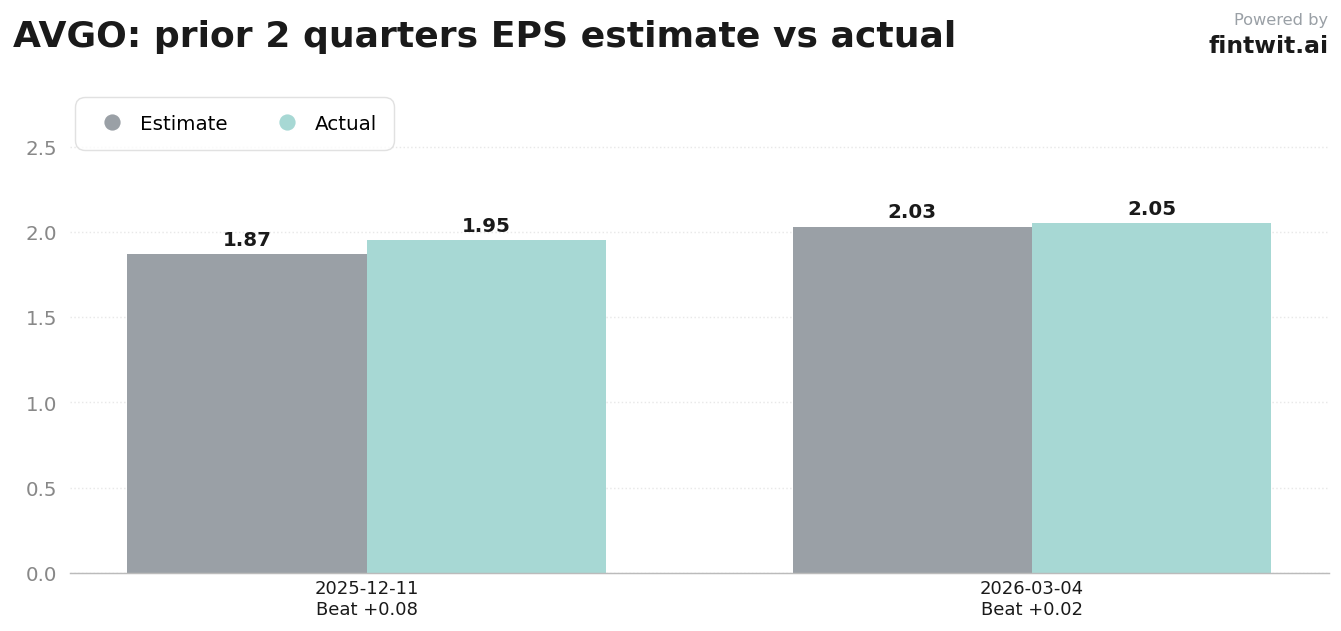

- Q4 2025 Actual EPS: $1.95 (Estimate: $1.87)

- Q1 2026 Actual EPS: $2.05 (Estimate: $2.03)

- Beat Probability: 75% beat, 20% inline, 5% miss

What we'll watch on the call

The primary focus remains the $10.7 billion AI revenue target for the quarter. Analysts are scrutinizing the sustainability of demand for custom AI accelerators and networking chips from major hyperscalers.

Integration of VMware into the enterprise software segment is a secondary but critical metric. Management commentary on supply chain capacity will be vital for assessing the remainder of the fiscal year.

- Can Broadcom sustain outsized AI chip growth despite investor concerns regarding hyperscaler ROI?

- What is the latest outlook for AI networking revenue compared to custom AI accelerators?

- How are gross margins trending given the shift in product mix toward AI-heavy solutions?

- What is the status of VMware integration and its contribution to enterprise AI software revenue?

- How are geopolitical tensions and export controls impacting semiconductor supply chains?

Fintwit's AI verdict

Sentiment across the financial community remains overwhelmingly bullish as the June 3 report approaches. The consensus narrative centers on the company's ability to scale its AI infrastructure business to meet hyperscaler demand.

While some analysts have trimmed specific AI revenue forecasts due to program adjustments, the broader outlook for fiscal 2026 remains elevated. Investors are positioning for potential upside surprises in the second half of the year.