CrowdStrike Holdings Inc (CRWD) Q1 Earnings Preview: What to Watch

CrowdStrike (CRWD) enters Q1 FY2027 with high expectations. We break down the consensus, key metrics, and the path forward for the cybersecurity leader.

The setup

CrowdStrike enters this report with significant tailwinds from the ongoing consolidation of cybersecurity vendors. The company's ability to displace legacy competitors through its Falcon platform remains the primary narrative for institutional investors.

Market sentiment is currently supported by broader strength in the SaaS sector, which has helped mitigate concerns regarding high valuation multiples. However, the stock's premium pricing leaves little room for error if management guidance fails to impress.

- Jefferies analyst Joseph Gallo maintains a $775 target, noting that near-term performance requires clear signals of ARR growth acceleration.

- Wedbush analyst Daniel Ives holds a $700 target, citing robust channel checks and confidence in the company's agentic AI strategy.

- Oppenheimer analyst Ittai Kidron points to a $750 target, emphasizing strong new logo acquisition and cross-selling momentum.

- The company faces a 60% probability of beating consensus estimates, according to current market modeling.

Consensus numbers

Wall Street analysts have converged on a consensus EPS of $1.07 for the first quarter of fiscal year 2027. Revenue is expected to reach $1.36 billion, representing a 23.5% increase compared to the same period last year.

The company's history of exceeding expectations provides a baseline for investor optimism, though the bar for outperformance has risen significantly.

- Q1 FY2027 EPS Estimate: $1.07

- Q1 FY2027 Revenue Estimate: $1.36 billion

- Full-year FY2027 ARR Target: $6.466 billion to $6.516 billion

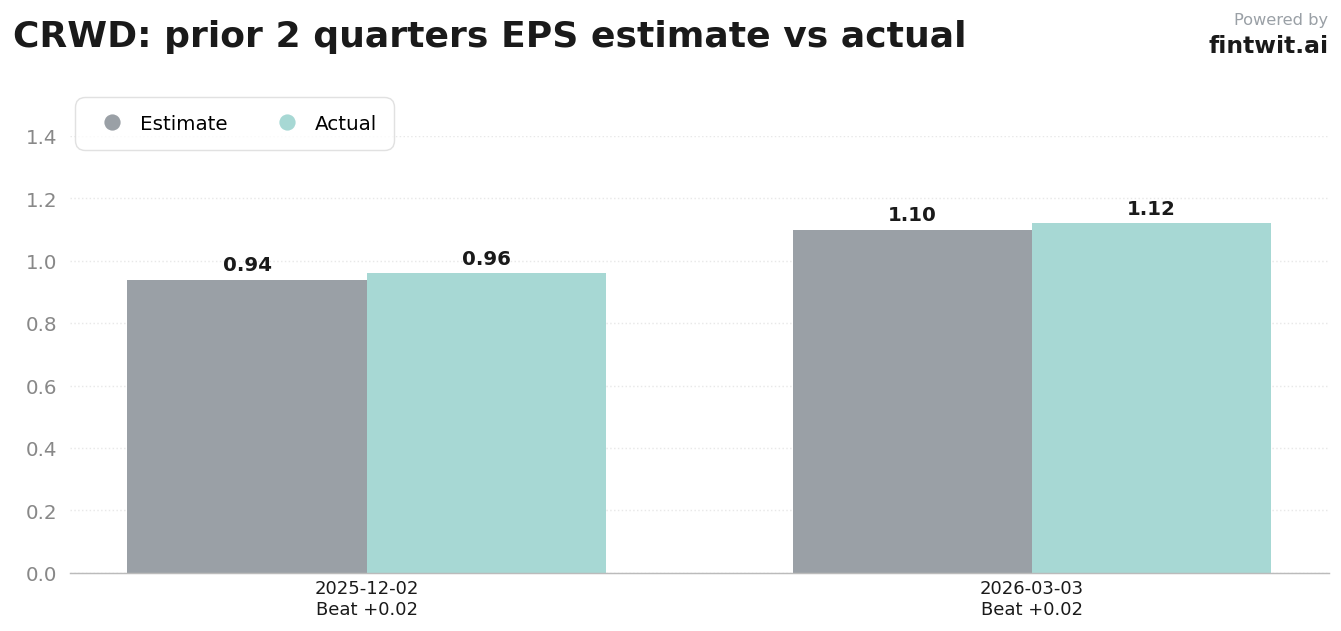

- Q4 FY2026 Actual EPS: $1.12 (vs $1.10 estimate)

- Q3 FY2026 Actual EPS: $0.96 (vs $0.939 estimate)

What we'll watch on the call

Management's commentary on the second half of the fiscal year will be the most important data point for the market. Investors are looking for a clear path toward accelerating ARR growth to justify the current valuation.

The integration of recent acquisitions, including SGNL and Seraphic Security, will be scrutinized for their contribution to the broader platform ecosystem.

- Net New ARR: Analysts are targeting approximately $275 million in net new ARR for the quarter.

- Falcon Flex Adoption: Monitoring the contribution of this subscription model to deal size and platform consolidation.

- Cross-selling Efficiency: Tracking the adoption rates of Next-Gen SIEM, Cloud, and Identity modules.

- Sales and Marketing Efficiency: Evaluating if the company is improving its operating leverage as it scales.

- Competitive Landscape: Assessing the impact of AI-driven security offerings from peer firms.

Fintwit's AI verdict

The quantitative models tracking CrowdStrike's momentum suggest that the market is positioned for a potential breakout if the company can clear the high hurdles set for its ARR growth. While the valuation is undeniably stretched, the underlying demand for consolidated security platforms remains a powerful force that continues to defy bearish expectations.

Investors should monitor the reaction to the guidance closely, as the delta between management's outlook and analyst models will likely dictate the price action in the coming sessions.