The AI Infrastructure Trade: Why NVDA, AVGO, and TSM Are the Physical Backbone

The AI infrastructure trade is now a rigorous, capex-driven physical buildout. We analyze the hardware and industrial suppliers powering the compute arms race.

The thesis

The AI infrastructure thesis has transitioned from a speculative narrative to a rigorous, capex-driven physical investment cycle. Hyperscalers are deploying massive capital to build the compute, power, and thermal management capacity required for agentic AI.

This buildout creates a durable revenue stream for hardware and industrial suppliers. These companies provide the essential backbone for AI regardless of volatility in software adoption rates.

Why now

Sam Altman of OpenAI recently noted that the world needs significantly more energy than previously estimated to support the compute requirements of modern AI. This realization has forced a pivot toward securing the physical constraints of the technology.

The market is moving from a phase of speculative software excitement to a phase of utility-driven infrastructure deployment. This shift favors companies that control the physical bottlenecks of the AI era.

Stocks we're watching

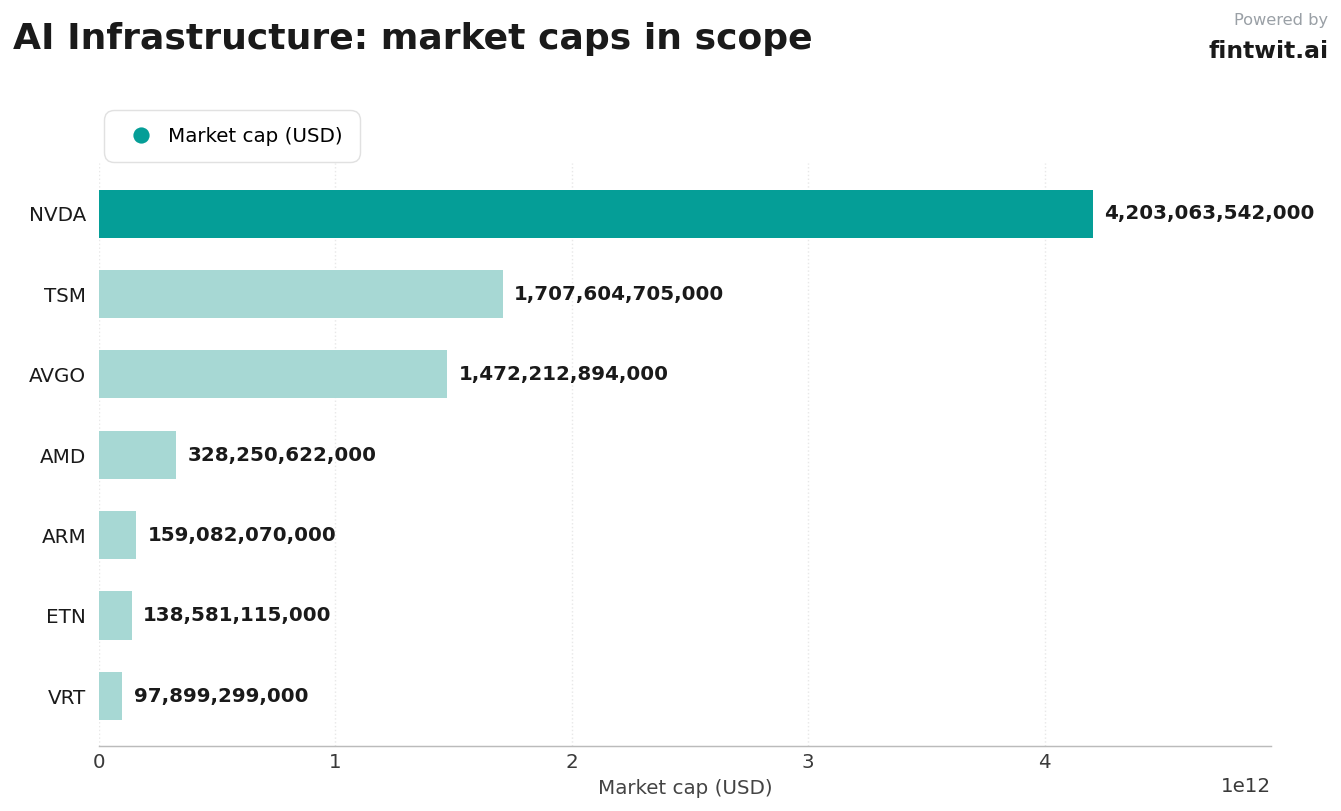

The following companies represent the core physical layer of the AI ecosystem, ranging from semiconductor design to grid management and cooling infrastructure.

Market capitalization data for these firms highlights the massive scale of the capital currently committed to this infrastructure buildout.

- NVDA (NVIDIA Corporation): The primary architect of the AI compute stack, providing the essential GPU hardware and CUDA software ecosystem.

- AVGO (Broadcom Inc): A critical partner for hyperscalers in designing custom ASICs and high-speed interconnects that enable massive AI clusters.

- TSM (Taiwan Semiconductor Manufacturing): The indispensable manufacturing backbone that produces the advanced semiconductors required by all major AI chip designers.

- ARM (Arm Holdings plc): Provides the power-efficient processor architecture that is increasingly central to custom AI chip designs and data center CPUs.

- AMD (Advanced Micro Devices Inc): The primary challenger to the GPU monopoly, offering scalable accelerator alternatives for training and inference workloads.

- VRT (Vertiv Holdings Co): Provides the essential cooling and power infrastructure required to keep high-density AI data centers operational.

- ETN (Eaton Corporation PLC): Supplies the critical electrical distribution and grid management equipment needed to power the massive AI data center buildout.

Risks that break it

While the infrastructure buildout is structurally sound, several factors could disrupt the current momentum. Investors must monitor these potential bottlenecks closely.

The transition from hype to utility is rarely linear, and equity valuations currently reflect high expectations for long-term compounding.

- Capex-digestion regime: A potential near-term slowdown in token consumption growth could lead hyperscalers to pause or throttle infrastructure spending.

- Physical and institutional bottlenecks: Grid constraints, permitting delays, and power scarcity may elongate project timelines, mismatching capital deployment with revenue generation.

- Margin compression and commoditization: As AI labs seek self-sufficiency and develop in-house custom silicon, the pricing power of current hardware incumbents may face long-term pressure.