Accenture plc (ACN) Q3 Earnings Preview: What to Watch

Accenture reports Q3 FY26 earnings on June 18. Analysts focus on AI-driven IT budget shifts and discretionary spending recovery.

The setup

Accenture enters the Q3 report with a complex narrative regarding its AI integration strategy. While the company has historically outperformed expectations, the current market environment is defined by stagnant IT services budget growth, projected at approximately 2% for calendar year 2026.

Investors are looking for evidence that the company's pivot toward large-scale AI implementation is moving beyond pilot programs. Management previously raised its FY26 revenue growth guidance to 3% to 5% in local currency, but recent macro volatility and regional geopolitical tensions have introduced new risks to this outlook.

- Morgan Stanley analyst James Faucette downgraded the stock, noting that the anticipated inflection in AI-driven IT budget growth has not materialized.

- MarketBeat consensus currently reflects a Moderate Buy rating with an average price target of $260.81.

- Zacks Equity Research maintains a positive outlook, citing the company's consistent history of earnings surprises and strong bookings momentum.

Consensus numbers

Market expectations for the third quarter are anchored by a consensus EPS of $3.71 and revenue of $18.78 billion. The company has a strong track record of exceeding these estimates, as seen in the previous two quarters where both EPS and revenue figures surpassed analyst projections.

The following metrics serve as the primary benchmarks for the upcoming release on June 18.

- Consensus EPS estimate: $3.71.

- Consensus revenue estimate: $18.78 billion.

- Managed Services segment growth: Expected to show 8% year-over-year expansion.

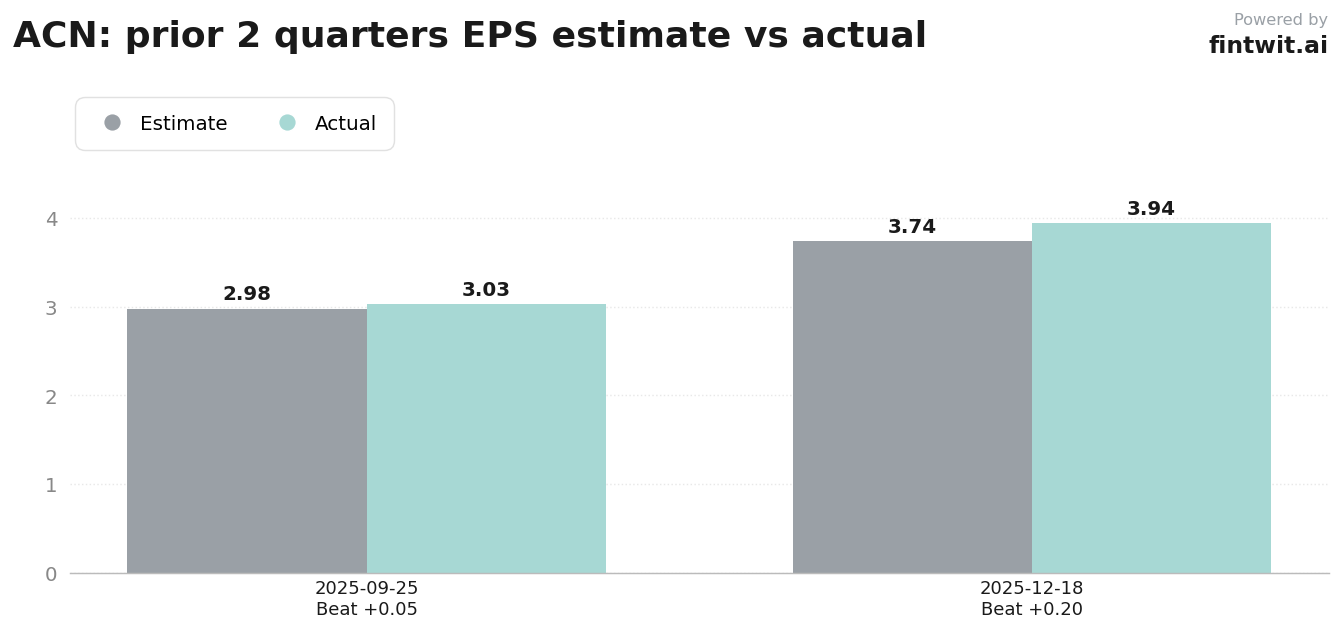

- Q1 FY26 performance: $3.03 EPS vs $2.98 estimated; $17.59 billion revenue vs $17.37 billion estimated.

- Q2 FY26 performance: $3.94 EPS vs $3.74 estimated; $18.74 billion revenue vs $18.52 billion estimated.

What we'll watch on the call

The primary focus for the earnings call will be the tension between AI-driven delivery efficiency and the potential compression of labor-based revenue models. Analysts are specifically looking for clarity on how the company is managing its consulting segment in the face of shifting client priorities.

Management's commentary on the sustainability of long-term revenue streams will be critical for maintaining the current valuation. The following items are the most significant variables for the upcoming discussion.

- Progress on the transition from AI pilots to measurable, large-scale revenue-generating projects.

- Evidence of discretionary IT spending recovery versus continued cannibalization by AI-specific investments.

- Updates on the FY26 revenue growth guidance of 3% to 5% in local currency.

- Impact of interest rate environments on the acceleration of large-scale digital transformation projects.

- Management's strategy for maintaining margins while scaling AI-driven delivery models.

Fintwit's AI verdict

The sentiment surrounding Accenture remains polarized as the market attempts to reconcile the company's long-term AI positioning with near-term macro headwinds. While the consensus remains cautious regarding the immediate impact of IT budget constraints, the firm's historical ability to navigate complex enterprise transitions provides a unique floor for investor expectations.

The upcoming earnings report will likely serve as a definitive indicator of whether the current valuation accurately reflects the company's ability to monetize its AI investments.