VistaGen Therapeutics Inc (VTGN) Q Earnings Preview: What to Watch

VistaGen Therapeutics (VTGN) faces a critical earnings report on June 16. We analyze the clinical pipeline, cash burn, and analyst sentiment.

The setup

VistaGen Therapeutics operates as a clinical-stage biopharmaceutical company focused on central nervous system disorders. The primary value driver is fasedienol, an investigational treatment for social anxiety disorder.

Management recently confirmed that current cash reserves are sufficient to fund operations through mid-2027. The company has hit minimum ICH E1 safety exposure recommendations for its fasedienol clinical program.

- Primary focus is the PALISADE-4 Phase 3 clinical trial for fasedienol.

- Operational enhancements include site retraining and AI-driven data strategies to mitigate placebo response.

- Refisolone remains a secondary pipeline asset with a planned IND submission.

- Macro headwinds include volatile interest rates affecting capital access for clinical-stage biotech firms.

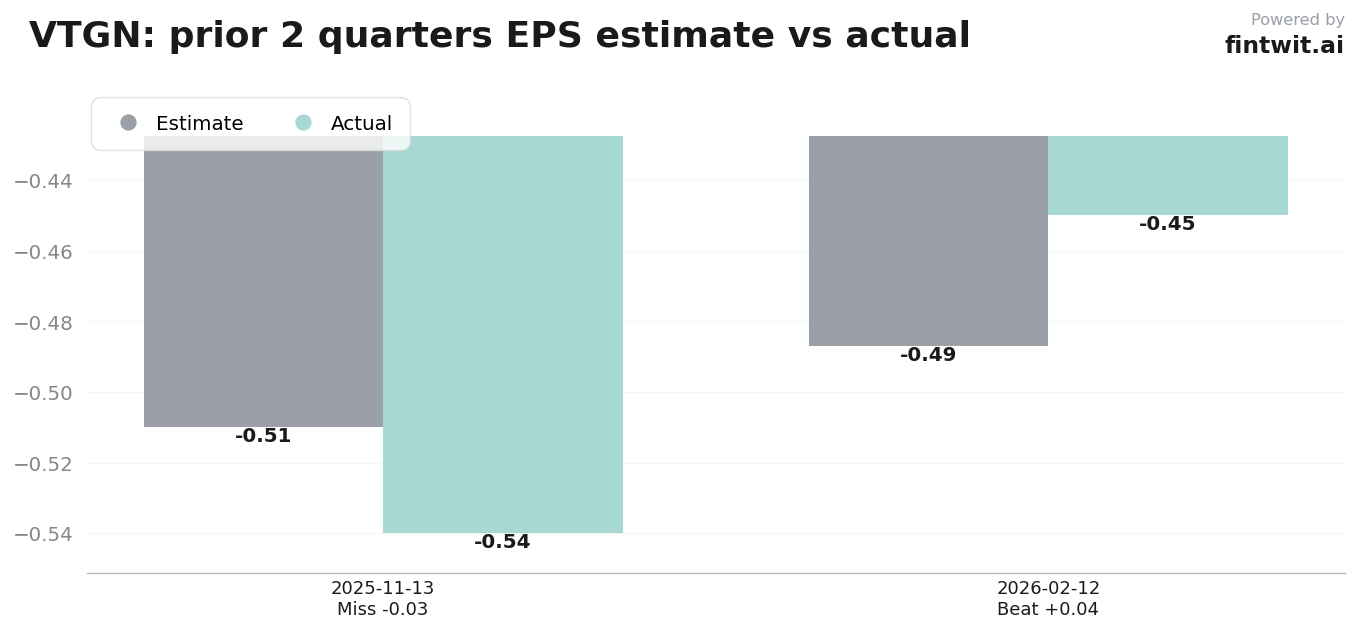

Consensus numbers

Analysts expect a net loss per share of $0.337 for the upcoming quarter. Revenue estimates are pegged at $399,900.

The company has shown a history of beating revenue estimates in the previous two quarters. However, EPS remains consistently negative as R&D spending drives cash burn.

- EPS Estimate: -$0.337

- Revenue Estimate: $399,900

- Q3 2025 Revenue: $258,000 (Beat estimate of $145,800)

- Q4 2025 Revenue: $303,000 (Beat estimate of $220,600)

- Stifel Nicolaus (Paul Matteis): Hold, $1.00 target

- Jefferies (Andrew Tsai): Hold, $0.90 target

- Lucid Capital (Elemer Piros): Hold, $1.00 target

What we'll watch on the call

Investors are looking for concrete updates on the PALISADE-4 trial timeline. The effectiveness of new AI-driven data strategies in reducing placebo response compared to PALISADE-3 is a key performance indicator.

Management commentary regarding the regulatory pathway for refisolone will be scrutinized. Any mention of non-dilutive funding or strategic partnerships will also be critical for extending the cash runway.

- What is the updated timeline for the topline results of the PALISADE-4 trial?

- How are AI/ML covariate identification tools impacting the placebo response rate?

- Can management provide clarity on the regulatory pathway for refisolone following the IND submission?

- Are there updates on potential strategic partnerships or non-dilutive funding opportunities?

Fintwit's AI verdict

The market sentiment remains cautious as the company navigates the binary risks associated with late-stage clinical trials. While the recent ICH safety milestones provide a foundation for progress, the lack of commercial revenue keeps the valuation tethered to speculative outcomes.

Investors should weigh the potential for M&A activity against the persistent cash burn and the dilution risks inherent in the current biotech funding environment. The upcoming report will likely serve as a volatility event for the stock's current trading range.