NVIDIA Corporation (NVDA): The Deep Dive Into AI Infrastructure Dominance

NVIDIA (NVDA) continues to define the AI infrastructure era. We break down the firm's 92% revenue growth and the competitive risks facing its market lead.

Why it's trending

NVIDIA's recent performance is defined by the explosive demand for its Blackwell and Hopper GPU architectures. The company has successfully transitioned from a gaming-focused hardware provider to a full-stack AI infrastructure utility.

Market sentiment remains overwhelmingly positive, as evidenced by the high volume of recent institutional activity. Analysts continue to monitor the firm's ability to maintain supply chain throughput against record-breaking demand from hyperscalers.

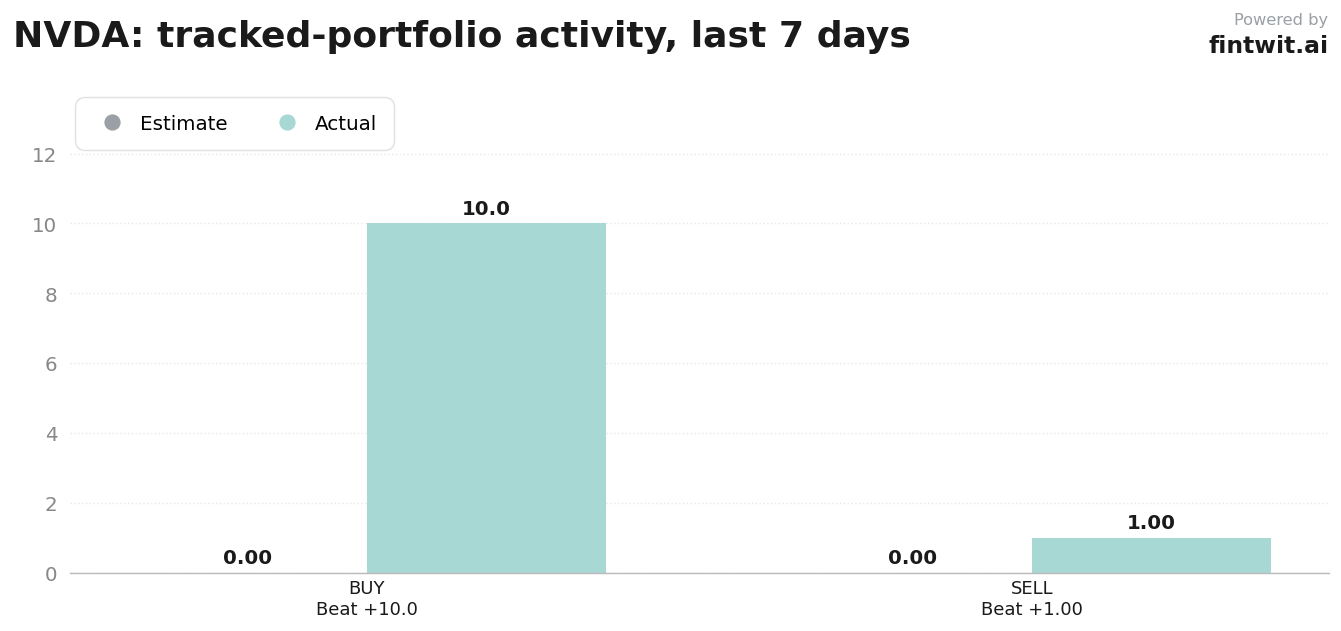

- Recent 7-day trading activity shows 10 buys compared to only 1 sell.

- The stock has delivered a 17.24% return over the last 180 days.

- Institutional holders count currently stands at 11 major entities.

The business in numbers

NVIDIA's financial profile is characterized by massive scale and high-margin revenue streams. The company's shift toward data center dominance has fundamentally altered its valuation multiple.

Management has prioritized shareholder returns, utilizing its robust free cash flow to fund aggressive buybacks and dividend growth.

- Data Center segment revenue reached $75.2B in Q1 FY2027, up 92% year-over-year.

- Data Center hardware accounts for 92.1% of total revenue.

- Forward P/E ratio sits at approximately 30.5x as of May 2026.

- Free cash flow margins range between 47% and 59%.

- The company authorized an $80B share repurchase program in Q1 FY2027.

- Quarterly dividend increased from $0.01 to $0.25 per share.

Bull vs bear

The bull case centers on the company's insurmountable lead in the AI software ecosystem and the persistent supply-demand imbalance. Conversely, bears point to the inherent risks of customer concentration and the rise of internal silicon development by major clients.

Investors must balance the potential for continued growth against the volatility associated with a high-beta asset.

- Bull: Wedbush Securities notes that GPU demand continues to outpace capacity, supporting long-term pricing power.

- Bull: UBS reports that Blackwell demand remains stronger than historical cycles, particularly within cloud infrastructure.

- Bull: MarketBeat consensus suggests a 50% upside with an average price target of $311.

- Bear: Intellectia AI highlights the threat of custom silicon solutions developed by hyperscalers.

- Bear: Geoffrey Seiler of The Motley Fool warns that major customers are increasingly becoming direct competitors.

- Bear: The stock's 2.22 beta indicates significant volatility risk compared to the broader market.

Fintwit's AI verdict

The consensus across the financial community remains focused on the sustainability of NVIDIA's moat. While valuation concerns persist, the sheer scale of capital expenditure from hyperscalers provides a floor for future earnings expectations.

Market participants are closely watching the interplay between interest rate sensitivity and the long-term adoption of generative AI. The following indicator summarizes the current sentiment regarding the stock's trajectory.