ViaSat Inc (VSAT) Q4 Earnings Preview: What to Watch

ViaSat Inc (VSAT) reports Q4 2026 earnings on May 25. Analysts focus on ViaSat-3 F3 utilization, Inmarsat integration, and the path to free cash flow inflection.

The setup

ViaSat is currently executing a multi-year operational turnaround centered on the integration of Inmarsat and the optimization of its satellite constellation. Management has previously guided for low single-digit year-over-year revenue growth and flattish adjusted EBITDA for fiscal 2026.

The company has taken aggressive steps to reduce capital intensity, recently revising full-year CapEx guidance downward to approximately $1.2 billion. This pivot is designed to support a free cash flow inflection in the second half of the fiscal year.

- Board composition changed recently following an agreement with activist investor Carronade Capital.

- The stock has experienced a significant year-to-date rally, prompting debate among analysts regarding current valuation levels.

- Geopolitical tensions continue to drive demand for the company's secure government and defense connectivity solutions.

Consensus numbers

Wall Street expectations for the upcoming quarter reflect a focus on operational efficiency and the successful deployment of new satellite assets. The following figures represent the current consensus estimates for the Q4 reporting period.

The company has demonstrated a strong track record of exceeding expectations in recent quarters, as shown in the historical performance data.

- EPS Estimate: $0.25

- Revenue Estimate: $1.196 billion

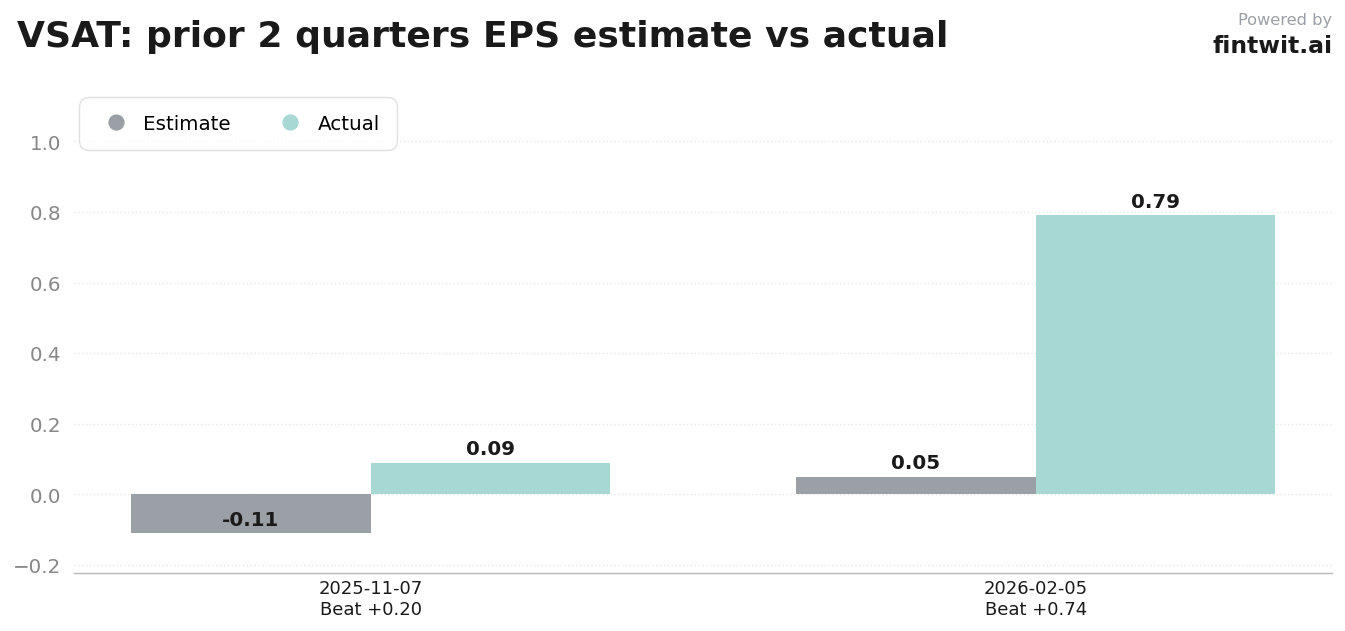

- Q3 2026 EPS: $0.79 (beat estimate of $0.05)

- Q2 2026 EPS: $0.09 (beat estimate of -$0.11)

- Mike Crawford (B. Riley Securities) maintains a $94.00 price target.

- Mathieu Robilliard (Barclays) maintains a $49.00 price target.

- Ryan Koontz (Needham) maintains a $58.00 price target.

What we'll watch on the call

Investors are looking for concrete evidence that the company's high capital expenditure is translating into tangible financial results. The management team will need to address the balance between growth in aviation connectivity and the decline in fixed broadband subscribers.

Debt management remains a primary concern given the current interest rate environment and the company's capital structure. Analysts will be listening for updates on how the firm plans to manage its leverage while continuing to fund its satellite programs.

- Utilization rates and revenue contribution from the newly launched ViaSat-3 F3 satellite.

- Specific timeline for sustainable free cash flow inflection and further debt reduction.

- Management's strategy for mitigating competitive pressures from LEO/GEO hybrid networks.

- Progress on Inmarsat integration synergies and their expected impact on fiscal 2027 profitability.

- Momentum in the Defense and Advanced Technologies segment, specifically regarding cybersecurity and tactical networking contracts.

Fintwit's AI verdict

The market sentiment surrounding ViaSat remains polarized as investors weigh the company's technological advancements against its significant debt load and valuation concerns. While the recent rally suggests optimism regarding the satellite deployment schedule, the upcoming earnings call will serve as a litmus test for whether the operational turnaround is truly gaining traction.

The interplay between defense contract execution and the competitive landscape of satellite communications will likely dictate the stock's trajectory in the coming months.