The Boeing Company (BA) vs Lockheed Martin (LMT): Which Is the Better Buy in 2026?

Boeing and Lockheed Martin represent two distinct paths in industrials. We break down the financials and risks to determine the better buy.

The matchup

Boeing and Lockheed Martin operate in the same aerospace and defense sector but face fundamentally different operational realities in 2026. Boeing is currently navigating a complex turnaround of its commercial aviation business while managing a $695B backlog.

Lockheed Martin maintains a more stable profile, anchored by its dominance in fifth-generation airpower and a $194B backlog. The company relies heavily on U.S. government budget cycles and global munitions demand to drive its consistent cash flow.

- Boeing (BA) focuses on 737 MAX and 787 production ramps alongside 777X certification.

- Lockheed Martin (LMT) prioritizes F-35 program stability and next-gen missile defense systems.

- Boeing's revenue grew 14% YoY in Q1 2026, while Lockheed Martin's revenue remained flat.

Numbers side by side

Financial metrics reveal the stark contrast between Boeing's growth-at-any-cost recovery and Lockheed's mature, dividend-paying model.

Investors should note the significant gap in P/E ratios and margin performance as of Q1 2026.

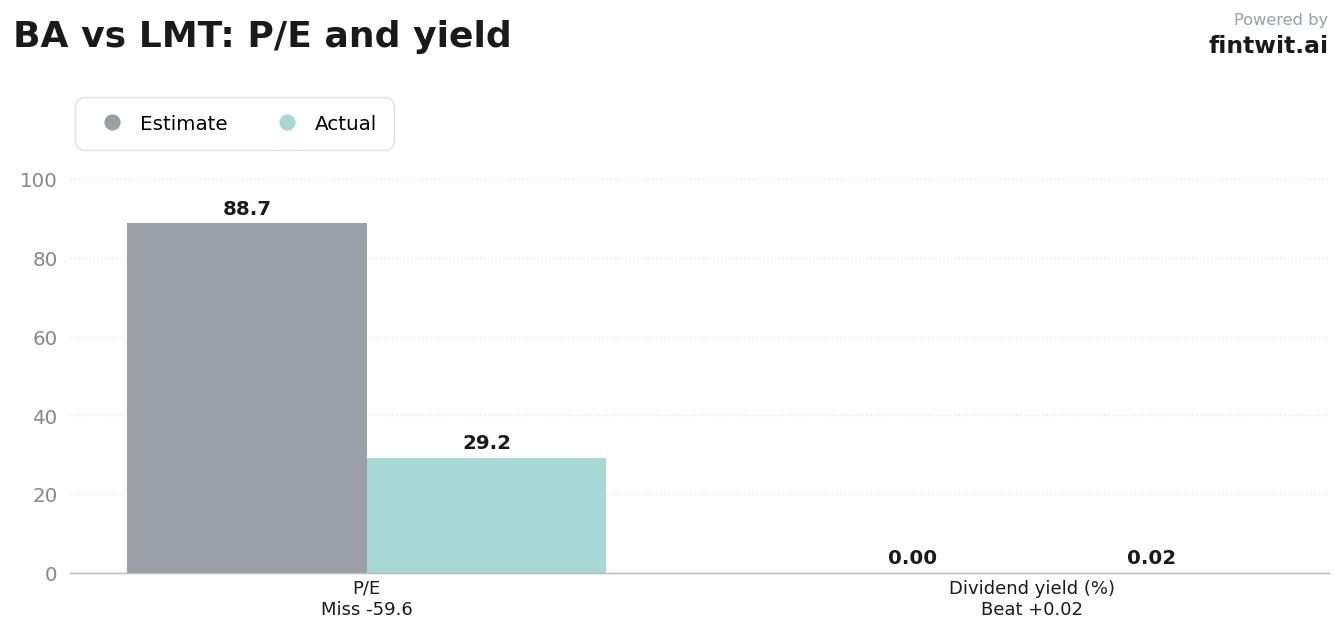

- Boeing P/E Ratio: 88.73 vs Lockheed Martin P/E Ratio: 29.16.

- Boeing Operating Margin: 1.7% (BCA segment at -6.1%) vs Lockheed Martin Operating Margin: 11.45%.

- Boeing Dividend Yield: 0.00% vs Lockheed Martin Dividend Yield: 2.09%.

- 1-Year Stock Performance: Boeing +7.96% vs Lockheed Martin +11.13%.

Bull and bear on each

The bull and bear cases for these firms hinge on execution and geopolitical stability. Boeing's future depends on clearing regulatory hurdles, whereas Lockheed's future depends on maintaining its technological lead in defense.

Both companies face significant supply chain constraints that could impact their 2026 delivery targets.

- BA Bull: Successful production ramp-up of 737 MAX and 787 programs.

- BA Bull: Entry into service of the 777X aircraft.

- BA Bear: Intense regulatory scrutiny and potential production caps.

- BA Bear: High debt burden limiting financial flexibility.

- LMT Bull: Increased global defense spending and munitions demand.

- LMT Bull: Strong free cash flow generation and dividend growth.

- LMT Bear: High valuation relative to near-term growth.

- LMT Bear: Supply chain bottlenecks and software delays on F-35 TR-3.

The verdict

Lockheed Martin remains the superior choice for investors prioritizing financial stability and consistent dividend growth. Its dominant market share in defense provides a defensive moat that Boeing currently lacks.

Boeing represents a high-risk, high-reward turnaround play that could see a massive valuation re-rating if management successfully executes its production goals and deleverages the balance sheet.