Should You Buy OKTA Right Now? A Deep Dive into the Identity Leader

Okta shares jumped 30.14% on a fiscal Q1 earnings beat. Is the identity security leader a buy for your portfolio?

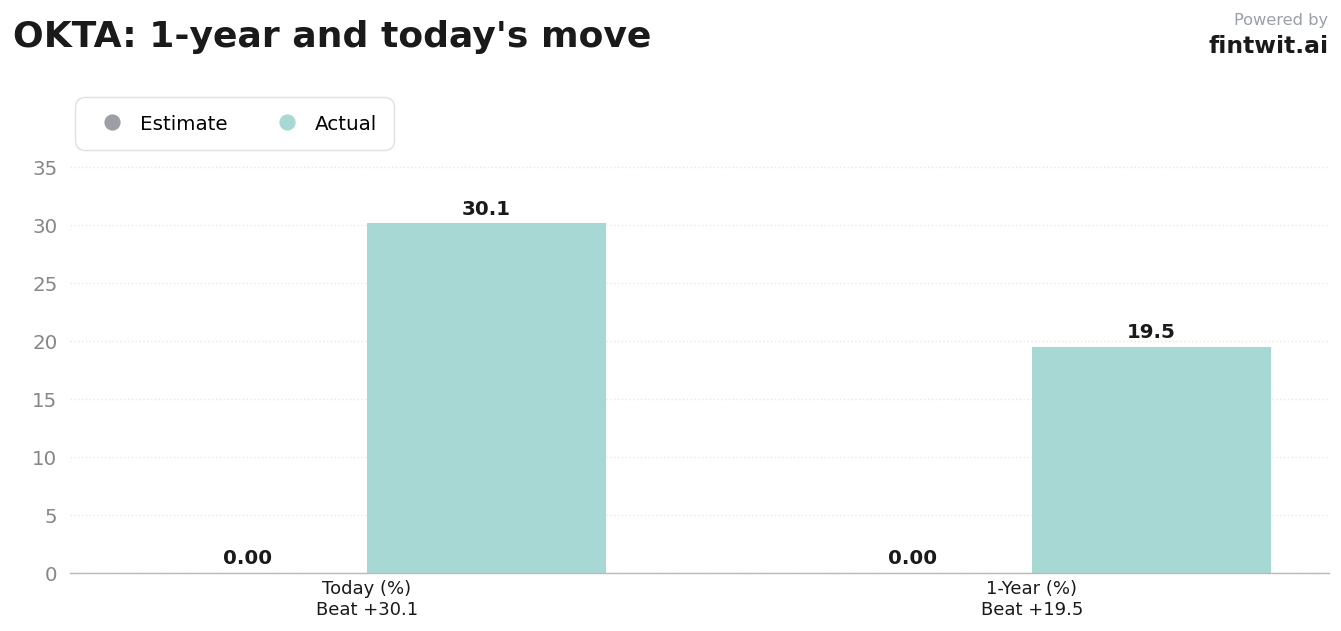

What just happened

Okta's fiscal Q1 2027 report served as a major catalyst for the stock, which broke out of a multi-week consolidation range between $75 and $95. The company demonstrated 11% year-over-year revenue growth and 12% current RPO growth.

The market response reflects a shift in perception, as Okta moves from a speculative story stock to a profitable compounder. Investors are reacting to improved free cash flow margins and GAAP profitability.

The stock is currently trading at $123.27, reflecting a 19.48% gain over the past year.

Bull case

- Okta for AI agents became generally available in April, establishing a new revenue stream.

- Strategic partnerships are now active with ServiceNow, Google, Amazon Bedrock, OpenAI, and Anthropic.

- Net revenue retention remains strong at 107%, indicating high customer stickiness.

- JPMorgan analyst Brian Essex maintains an Overweight rating with a $120 price target.

- Arete Research upgraded the stock to Buy with a $127 price target, citing agentic AI demand.

- Scotiabank raised its FY2027 EPS estimate to $1.65, up from the previous $1.60 forecast.

Bear case

- The stock currently trades at a P/E ratio of 59.85, which represents a premium valuation.

- Growth deceleration remains a risk if enterprise software spending slows in the second half of 2027.

- Scotiabank maintains a Sector Perform rating, suggesting limited upside from current levels.

- The company does not pay a dividend, making it unsuitable for income-focused portfolios.

- Execution risk persists as Okta attempts to integrate its identity solutions into complex AI agent workflows.

Fintwit's AI verdict

The sentiment surrounding Okta has shifted significantly following the recent earnings report. Analysts are increasingly focused on the company's ability to capture the identity security market for AI agents, which is viewed as a durable long-term tailwind.

While valuation concerns persist due to the high P/E ratio, the fundamental performance and raised guidance provide a strong narrative for continued growth. The market is currently weighing these growth prospects against the broader macroeconomic environment for software infrastructure.