Should You Buy DELL Right Now? Analyzing the AI Infrastructure Surge

Dell Technologies shares surged 32.76% after a record-breaking earnings report. We analyze the AI server demand, analyst targets, and the path forward for DELL.

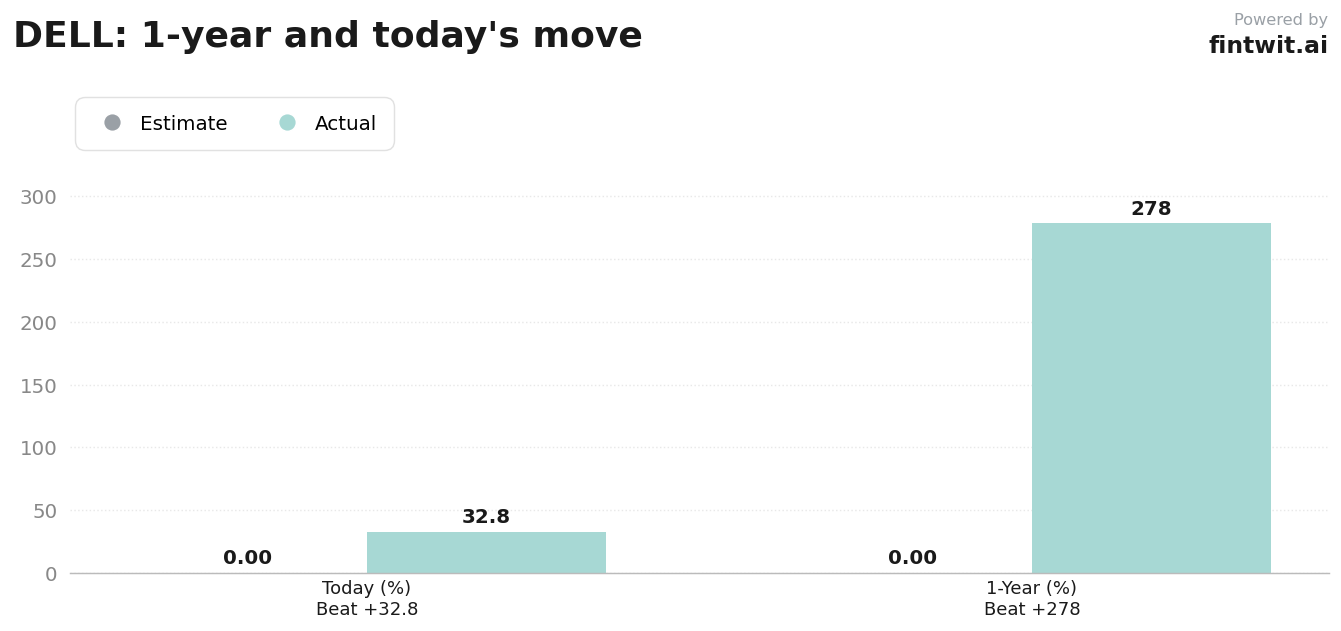

What just happened

Dell reported Q1 revenue of $43.84 billion, representing an 88% increase compared to the same period last year. The primary driver was the Infrastructure Solutions Group, which saw AI-optimized server revenue skyrocket 757% to $16.13 billion.

Management raised its full-year revenue guidance to a range of $165 billion to $169 billion. This outlook reflects the company's massive $43 billion-plus backlog for AI-optimized servers that continues to grow as hyperscalers expand their data center capacity.

The market response was immediate, with shares jumping over 32% in a single session. This move confirms Dell's transition from a legacy PC manufacturer to a critical player in the global AI supply chain.

Bull case

The bullish thesis centers on Dell's ability to convert its massive order backlog into sustained revenue growth throughout FY27. Analysts have aggressively revised their price targets to reflect this improved earnings trajectory.

Key drivers for the bull case include:

- JPMorgan raised its price target to $500, maintaining an Overweight rating.

- Citi analyst Asiya Merchant increased her target to $475, citing strong ISG operating margins.

- AI-optimized server revenue grew 757% YoY, signaling a structural shift in enterprise spending.

- The company's ability to scale infrastructure production remains a key competitive advantage against smaller hardware rivals.

Bear case

Skeptics point to the rapid valuation expansion, which has pushed the stock to a P/E ratio of 18.14 after the recent rally. While growth is high, the hardware sector is historically cyclical and prone to margin compression if demand plateaus.

Risks to the current momentum include:

- UBS maintains a Neutral rating, setting a $440 price target despite the earnings beat.

- Supply chain constraints for high-end GPUs could limit the speed at which the $43 billion backlog is converted to revenue.

- Macroeconomic headwinds could force enterprise clients to pull back on long-term data center capital expenditures.

- The dividend yield remains low at 1.34%, as capital is prioritized for aggressive share repurchases and R&D.

Fintwit's AI verdict

The sentiment across financial social media platforms remains overwhelmingly positive, with many traders viewing the recent price action as a breakout rather than a blow-off top. The consensus among institutional analysts and retail sentiment trackers suggests that the fundamental shift in Dell's business model justifies the current valuation premium.

While the stock has experienced a significant run, the underlying demand for AI infrastructure shows no signs of cooling. Investors are now looking toward the upcoming June 25, 2026, Annual Meeting of Stockholders to gauge management's long-term capital allocation strategy and the proposed redomestication to Texas.