Should You Buy IONQ Right Now? Analyzing the Quantum Computing Leader

IonQ shares fell 9.61% today despite record revenue growth. Is the current pullback a buying opportunity or a warning sign for quantum investors?

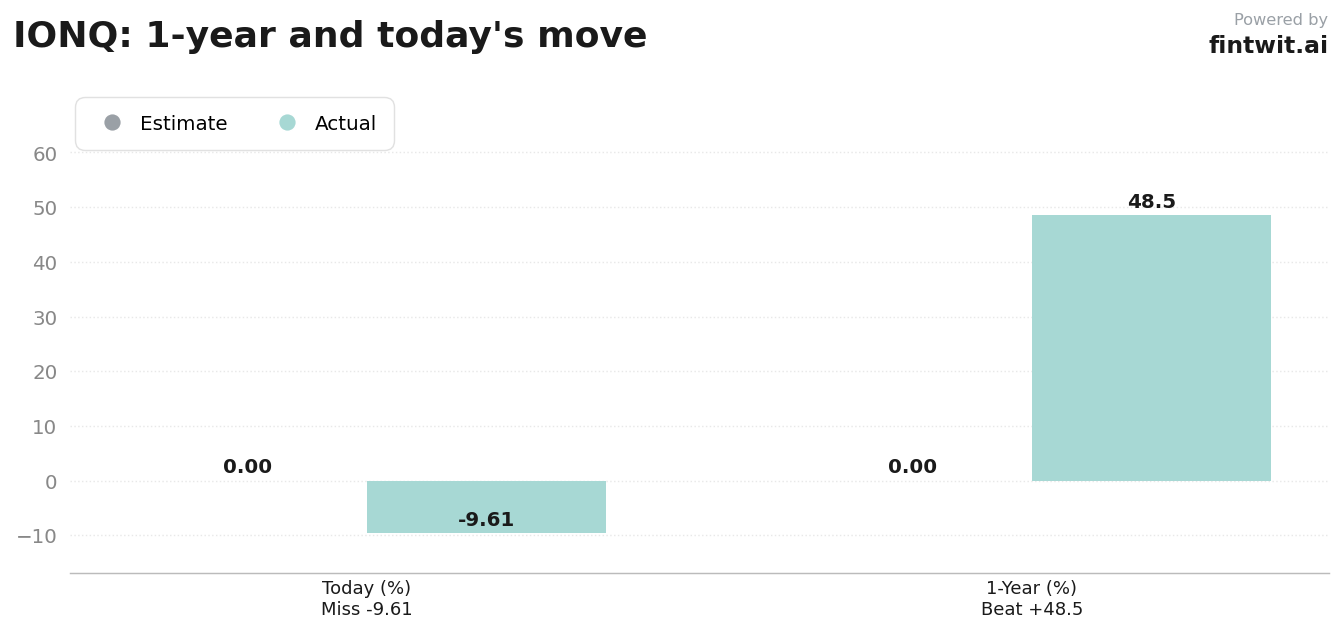

What just happened

The 9.61% decline marks a sharp reversal for IonQ, which had seen its shares climb 48.47% over the past 12 months. This volatility follows a 'sell the news' reaction to the company's Q1 2026 results, where strong top-line growth was offset by persistent concerns regarding cash burn.

Market participants are currently re-evaluating high-valuation technology assets as risk-off sentiment permeates the hardware sector. The price action suggests that even record-breaking revenue figures are insufficient to satisfy investors when adjusted EBITDA remains deeply negative.

Bull case

Proponents of IonQ point to the company's rapid commercial scaling and its ability to convert research milestones into tangible enterprise demand. The firm's revenue trajectory remains the primary driver for long-term bullish sentiment.

Analyst coverage remains split but highlights significant upside potential if the company meets its technical roadmap targets.

- Q1 2026 revenue reached a record $64.7 million, representing a 755% year-over-year increase.

- Remaining performance obligations (RPOs) surged 554% year-over-year to $470 million, indicating strong future demand.

- Full-year 2026 revenue guidance was raised to a range of $260 million to $270 million.

- John McPeake of Rosenblatt maintains a Buy rating with a $100.00 price target, citing technological leadership.

- Antoine Legault of Wedbush reiterates an Outperform rating with a $60.00 target, highlighting commercial diversification.

Bear case

Skeptics emphasize the structural risks inherent in the quantum computing industry, specifically the long timeline to achieve sustainable profitability. The current valuation multiples are difficult to justify for investors focused on traditional financial metrics.

The reliance on stock-based compensation and the lack of a clear path to positive EBITDA remain significant hurdles for the stock.

- The company continues to report deepening adjusted EBITDA losses despite top-line growth.

- Peter Peng of JP Morgan maintains a Neutral rating with a $50.00 price target, citing valuation concerns and profit uncertainty.

- High stock-based compensation continues to dilute shareholder value as the company burns cash to fund R&D.

- The sector-wide momentum unwind suggests that high-multiple stocks remain vulnerable to further downside in a risk-off environment.

Fintwit's AI verdict

The quantitative model evaluates IonQ based on its aggressive revenue scaling and market positioning within the quantum hardware space. While the current volatility is significant, the underlying growth metrics suggest a specific trajectory that warrants close attention from growth-oriented portfolios.

Investors must weigh the high-conviction growth narrative against the reality of pre-profit financials and sector-wide valuation compression. The following assessment provides a data-driven perspective on the current setup.