Should You Buy Akamai Technologies (AKAM) Stock Right Now?

Akamai (AKAM) stock jumped on a $1.8B AI deal. Is it a buy? We analyze the bull and bear cases and what investors should watch.

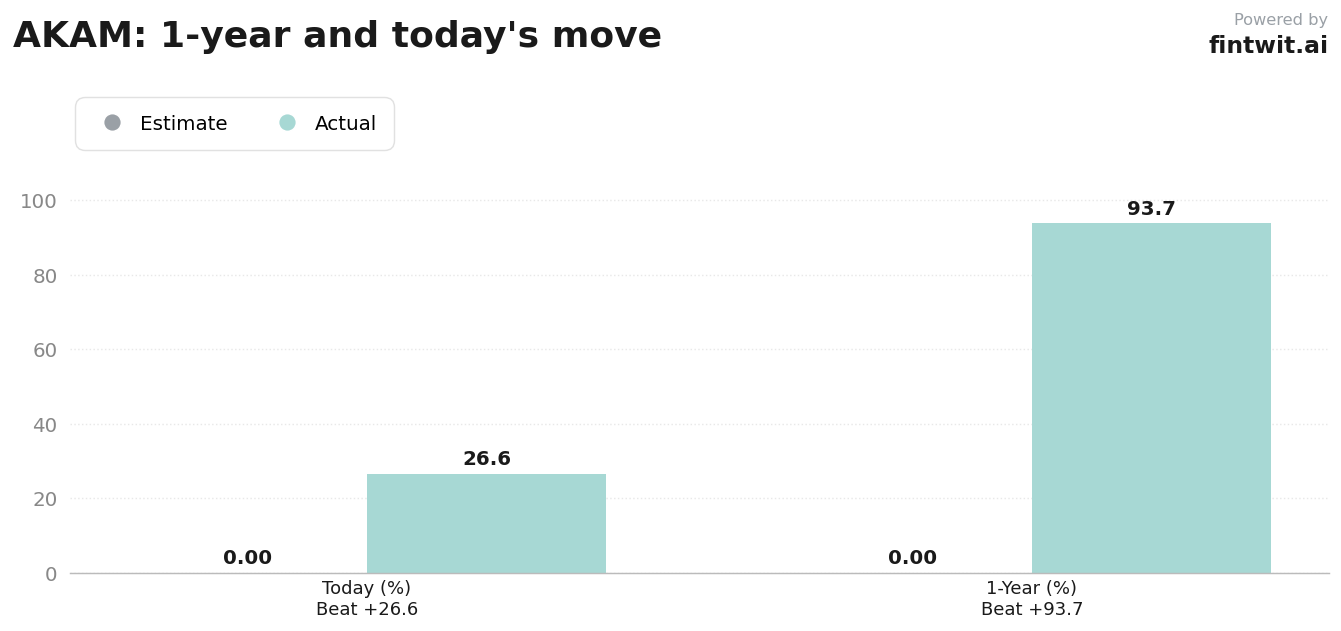

What just happened

Akamai Technologies Inc. stock experienced a significant surge, climbing 26.58% following the announcement of a substantial new contract. This deal, valued at $1.8 billion over seven years, is for Cloud Infrastructure Services (CIS) with a major AI model provider.

The company's Q1 2026 earnings report also contributed to the positive momentum. Revenue grew 6% year-over-year to $1.074 billion, with non-GAAP EPS at $1.61. Security revenue saw an 11% increase, and the CIS segment revenue surged by 40%.

- Today's price increase: 26.58%

- 1-year return: 93.72%

- Q1 2026 Revenue: $1.074 billion (+6% YoY)

- Q1 2026 Non-GAAP EPS: $1.61

- Q1 2026 Security Revenue: +11% YoY

- Q1 2026 CIS Revenue: +40% YoY

Bull case

The primary driver for Akamai's bullish outlook is its strategic positioning to benefit from the artificial intelligence boom. The newly secured $1.8 billion, seven-year deal for Cloud Infrastructure Services directly taps into the massive demand for AI-powered computing.

Akamai's management has raised its outlook for the CIS segment, now anticipating at least 50% year-over-year growth. This, combined with a rapidly accelerating pipeline, has led the company to forecast double-digit annual revenue growth in 2027.

Beyond AI infrastructure, Akamai's core security business continues to perform strongly. With the increasing sophistication of cyber threats, particularly those driven by AI, Akamai's robust security solutions are in high demand, providing a stable and growing revenue stream.

- New $1.8 billion, 7-year AI infrastructure deal.

- CIS segment growth outlook raised to 50%+ YoY.

- Projected double-digit annual revenue growth in 2027.

- Strong demand for cybersecurity solutions.

- Increased capital expenditures to support GPU infrastructure and colocation for AI demand.

Bear case

Despite the recent surge and positive AI deal, concerns remain about margin compression. Pressure in the traditional content delivery network (CDN) business and increased investment in infrastructure to support AI could weigh on profitability.

The competitive landscape for CDN services is intense, and while Akamai is a leader, slower trends in this segment have historically tempered growth expectations. This could limit the upside from its core business.

Current valuations, especially after the significant price jump, may not fully reflect the execution risks associated with scaling new infrastructure and integrating large AI-related projects. Investors should monitor the company's ability to translate these investments into sustainable, profitable growth.

- Margin pressure in the delivery business.

- Intense competition in the CDN market.

- Rising costs associated with infrastructure investments for AI.

- Potential for slower growth in traditional CDN services.

- Valuation concerns after a significant stock price increase.

Fintwit's AI verdict

The market's reaction to Akamai's latest announcement underscores the significant investor appetite for companies positioned to capitalize on the AI revolution. The substantial commitment from a major AI provider signals a new growth chapter for the company.

However, the path forward involves navigating increased capital expenditures and potential margin pressures. The question for investors is whether the long-term AI infrastructure opportunity outweighs these near-term challenges and the current valuation.