Cheapest Large-Cap Stocks by P/E Ratio: A Deep Dive

Screening for the cheapest large-cap stocks reveals opportunities in telecom, insurance, and materials. Understand the risks and catalysts.

How we screened

We screened for large-capitalization companies with a Price-to-Earnings (P/E) ratio below 7.5. This threshold identifies companies trading at a significant discount relative to their earnings.

The screen focused on identifying stocks where the market may be undervaluing current earnings power, potentially due to temporary headwinds or sector-wide pessimism.

We prioritized companies with available Free Cash Flow (FCF) data to provide an additional layer of financial health assessment.

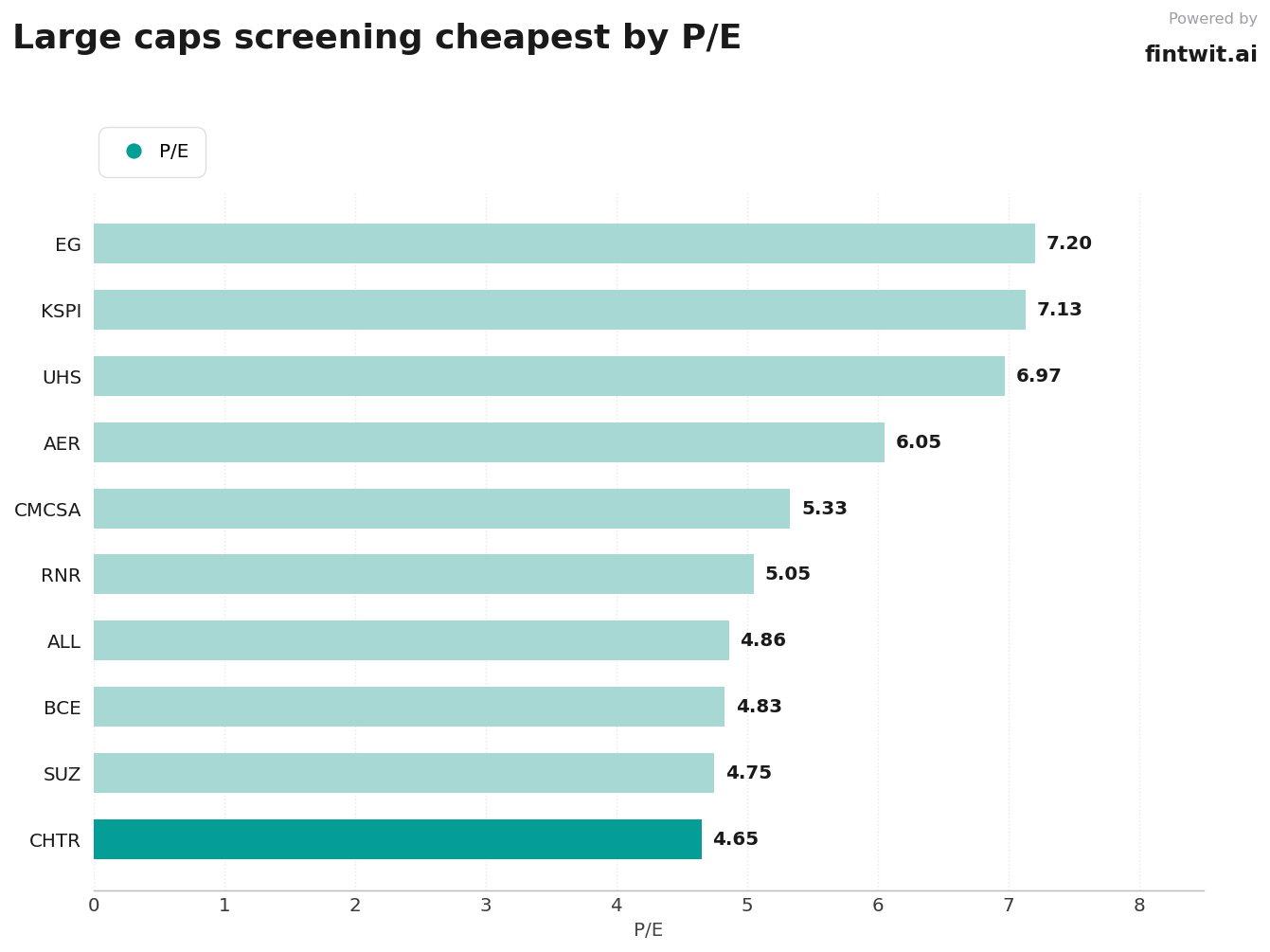

The list

Several companies stand out with exceptionally low P/E ratios, indicating potential value opportunities. However, these low multiples often signal underlying business challenges or market concerns.

- Charter Communications (CHTR): P/E 4.65. Why cheap: Trades at a low forward EV/EBITDA multiple due to persistent broadband subscriber losses. Analyst Take: 'The concern is legitimate. Broadband subscriber losses have persisted across multiple quarters, AT&T has expanded fixed wireless in Charter's footprint, fiber overbuilds continue at a steady pace, and Charter carries approximately $94 billion in debt.' Verdict: Deteriorating fundamentals.

- Suzano Papel e Celulose SA ADR (SUZ): P/E 4.75. Why cheap: N/A. Analyst Take: No specific information found for SUZ. Verdict: Insufficient data.

- BCE Inc (BCE): P/E 4.83. Why cheap: Analysts have lowered earnings estimates, and the company is expected to show a year-over-year earnings decline, facing headwinds from increased competition. Analyst Take: 'BCE is facing challenges in its Wireline segment, as competition in the Canadian telecommunications market continues to intensify. With only a marginal decline expected in the company's leverage ratio despite strong FCF production, there is a concern that BCE is not doing enough to reduce its debt and maintain a healthy balance sheet.' Verdict: Deteriorating fundamentals.

- The Allstate Corporation (ALL): P/E 4.86. Why cheap: Trades at a PE below 6x and a PEG of 0.04x, below peers, with strong recent earnings and margin expansion. Analyst Take: 'Allstate Corp. is rated Hold, reflecting strong recent earnings and margin expansion but limited premium growth, especially in auto. ALL's profitability has improved via disciplined underwriting and catastrophe management, with combined ratios and margins trending positively over the past 10 quarters.' Verdict: Sentiment/Sector Out-of-Favor.

- Renaissancere Holdings Ltd (RNR): P/E 5.05. Why cheap: Consensus price target suggests potential upside, and the stock is trading near its fair value estimate. Analyst Take: 'Bears say. RenaissanceRe Holdings Ltd is expected to face challenges due to soft pricing in its key lines of business, which may constrain the company's valuation multiple and limit near-term upside potential. Additionally, an observed sensitivity of earnings per share (EPS) estimates suggests that any fluctuations could significantly impact the company's price target, indicating high volatility in financial performance.' Verdict: Sentiment/Sector Out-of-Favor.

- Comcast Corp (CMCSA): P/E 5.33. Why cheap: Trades at a forward P/E ratio that is a premium to the sector median, but some analyses suggest undervaluation based on DCF. Analyst Take: 'From a valuation perspective, even after Friday's 13% drop, CMCSA trades at a 14x forward P/E ratio, a 10% premium to the U.S. communication services sector median of 12.7x, suggesting that further downside risk remains if additional analysts revise their estimates lower in the coming weeks.' Verdict: Deteriorating fundamentals.

- AerCap Holdings NV (AER): P/E 6.05. Why cheap: N/A. Analyst Take: N/A. Verdict: Insufficient data.

- Universal Health Services Inc (UHS): P/E 6.97. Why cheap: Trades at a decade-low valuation despite strong EPS growth and robust capital returns, with a consensus 'Hold' rating. Analyst Take: 'Bears say. Universal Health Services is experiencing a decline in core EBITDA growth and a potential gap in their 2026 guidance, leading to skepticism and a sell-off. This is due to a number of factors, including lower than expected flu and weather impacts, lower HIX volumes, and higher staffing costs.' Verdict: Sentiment/Sector Out-of-Favor.

- Joint Stock Company Kaspi.kz (KSPI): P/E 7.13. Why cheap: N/A. Analyst Take: N/A. Verdict: Insufficient data.

- Everest Group Ltd (EG): P/E 7.20. Why cheap: Trades below book value, with some analysts seeing 15% upside and maintaining a 'Buy' rating. Analyst Take: 'Everest Group, Ltd. faces legacy insurance issues, prompting major reserve builds & strategic shift under new leadership. Read more on EG stock here ... RemainCo Fundamentals Are Actually Solid.' Verdict: Deteriorating fundamentals.

Caveats

Low P/E ratios can be a siren song, often indicating underlying business distress or significant market skepticism that may not be fully captured by the multiple.

Companies like Charter Communications (CHTR) and Comcast (CMCSA) face secular headwinds in their core broadband and media businesses, respectively, which could pressure future earnings.

The insurance and reinsurance sectors, represented by Allstate (ALL), RenaissanceRe (RNR), and Everest Group (EG), are cyclical and sensitive to catastrophe events and pricing power, making earnings volatile.

- Charter Communications (CHTR) carries substantial debt ($94 billion), increasing financial risk.

- BCE Inc (BCE) is navigating intense competition in the Canadian telecom market.

- Universal Health Services (UHS) faces labor inflation and reimbursement pressures.

- Everest Group (EG) is undergoing strategic repositioning due to legacy insurance issues.

How to use this screen

This screen serves as a starting point for identifying potentially undervalued companies, not a definitive buy list. Further due diligence is essential.

Focus on the 'why cheap' and 'analyst take' to understand the market's concerns and assess if they are temporary or structural.

Consider the company's free cash flow generation and balance sheet strength to gauge its ability to weather challenges and return capital to shareholders.

- For Charter (CHTR), assess the impact of fixed wireless competition and fiber overbuilds.

- For Allstate (ALL), evaluate the sustainability of underwriting improvements and premium growth.

- For Universal Health Services (UHS), monitor trends in labor costs and reimbursement rates.