Replimune Group Inc (REPL) Q4 Earnings Preview: What to Watch

Replimune Group (REPL) reports Q4 earnings on June 11. Investors are focused on the RP1 regulatory path and cash management following the April 2026 CRL.

The setup

Replimune enters this earnings cycle under intense scrutiny after receiving a second Complete Response Letter (CRL) for RP1 in April 2026. Management has since signaled a path forward for a BLA resubmission, but the market remains skeptical of the timeline.

The company is currently a pre-revenue clinical-stage firm. Investor focus is entirely on the regulatory viability of its pipeline and the sustainability of its current cash position.

- The FDA issued a second CRL for RP1 in April 2026, citing concerns regarding the contribution of effect.

- Management recently held discussions with the FDA, characterizing the path to BLA resubmission as a priority.

- The current consensus rating on the stock is Hold, reflecting significant uncertainty regarding the regulatory outcome.

- Regulatory scrutiny on accelerated approval pathways for oncology therapies remains a major macro headwind for the sector.

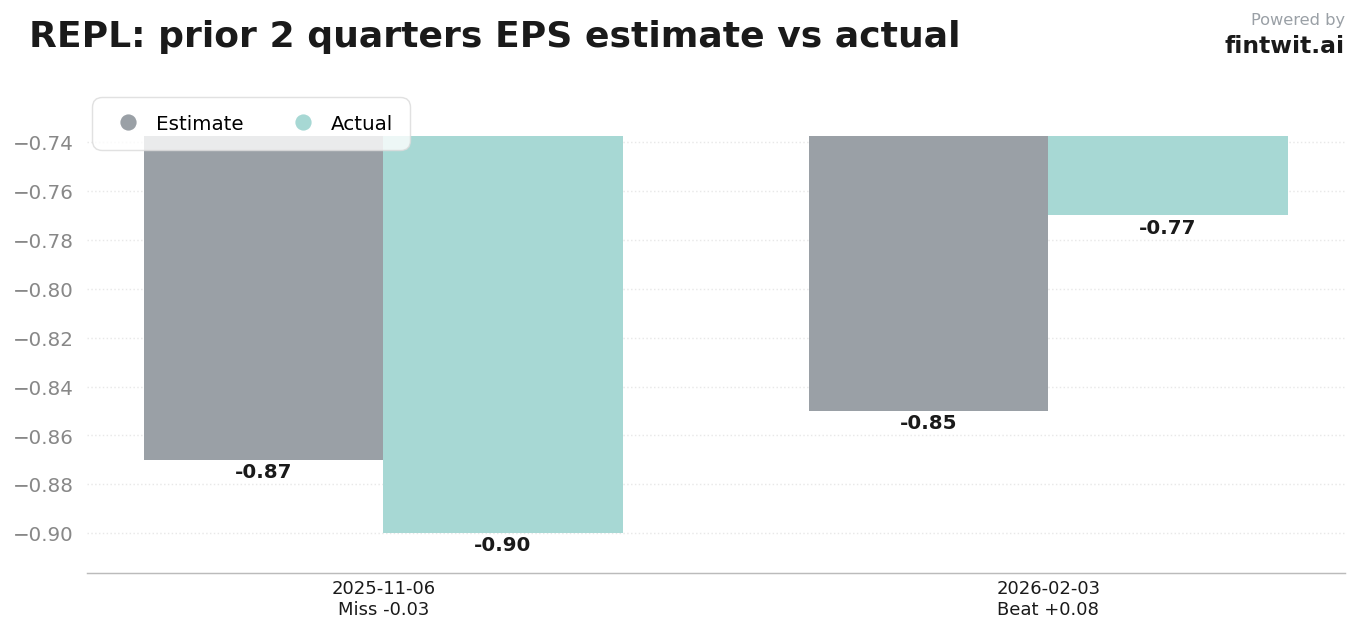

Consensus numbers

Wall Street analysts expect a loss per share of $0.73 for the quarter ending June 11, 2026. Revenue estimates are pegged at approximately $5.57 million.

The company has a history of missing earnings expectations, as seen in the November 2025 and February 2026 reports. The probability of a miss is currently estimated at 45%.

- EPS Estimate: -$0.73

- Revenue Estimate: $5.57 million

- Beat Probability: 35%

- Miss Probability: 45%

- Inline Probability: 20%

- Median Analyst Price Target: $4.00

What we'll watch on the call

Investors are looking for specific details on how the company plans to address the FDA's concerns regarding the contribution of effect for RP1. Clarity on the BLA resubmission timeline is the most critical factor for the stock's valuation.

Cash management is the secondary priority. With no commercial revenue, the burn rate against existing cash reserves will dictate how long the company can operate without further dilution.

- What specific data or analyses will be included in the BLA resubmission to address the FDA's concerns?

- Can management provide a more concrete timeline for the 'urgent' FDA review process?

- How does the company plan to manage its cash runway if the regulatory process extends further into 2027?

- Are there any updates on the IGNYTE-3 trial that could serve as a hedge if the BLA resubmission faces further hurdles?

- What is the status of the commercial organization and supply chain readiness for a potential RP1 launch?

Fintwit's AI verdict

The current valuation of Replimune appears to bake in a binary outcome that heavily discounts the potential for a successful RP1 approval. While the regulatory path is fraught with risk, the recent dialogue with the FDA suggests a more structured approach than previously anticipated.

Investors weighing the risk-reward profile should consider the implications of the upcoming BLA resubmission on the company's long-term liquidity. The market is currently pricing in a high probability of failure, which may create an asymmetric opportunity for those willing to tolerate high volatility.