Kinross Gold (KGC) Undervalued? Analyst Targets Suggest Upside

Kinross Gold (KGC) trades at a discount to peers, with analysts seeing significant upside. Explore the valuation and key factors.

The headline number

Kinross Gold Corporation (KGC) reported a P/E ratio of 13.61, which is notably lower than the Basic Materials sector average of 24.73.

This valuation metric also positions KGC favorably against its specific industry, with the US Metals and Mining industry average P/E at 21.9x.

The company's current market price of $31.81 reflects this discount, with a market capitalization of $3.2 billion.

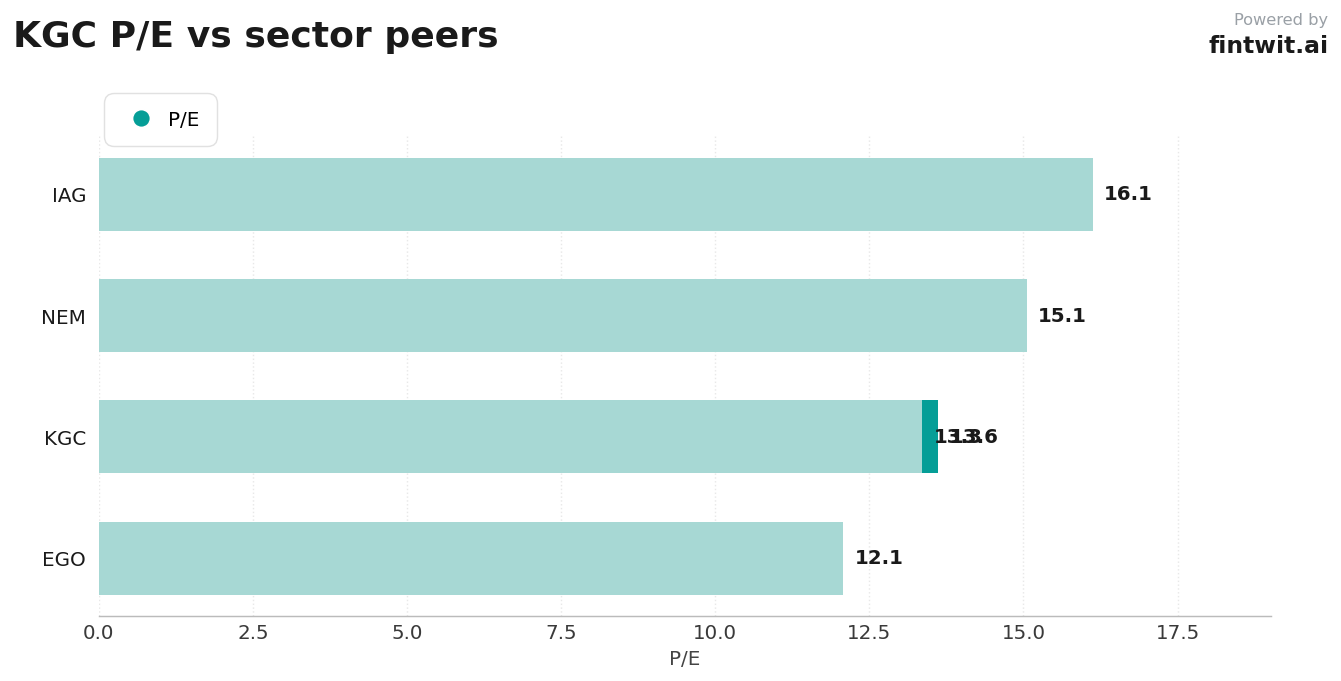

Peer comparison

Kinross Gold (KGC) trades at a P/E ratio of 13.61, making it appear undervalued relative to some peers.

Eldorado Gold Corp. (EGO) presents a lower P/E of 12.07, indicating a potentially cheaper valuation for that company.

Newmont Corp. (NEM) has a slightly higher P/E of 15.05, suggesting KGC is more attractively priced on this metric.

Iamgold Corp. (IAG) trades at a higher P/E of 16.12, further highlighting KGC's relative discount.

Bull vs bear

The bull case for Kinross Gold centers on its current undervaluation, supported by a P/E ratio below industry and peer averages. Analysts generally agree, with a consensus 'Buy' rating and a median price target of $43.50, implying a 38.1% potential upside. Strong free cash flow generation, record FCF of $2.5 billion in 2025 and $837.5 million in Q1 2026, alongside promising growth projects like Great Bear and Lobo-Marte, bolster this optimistic outlook. A solid balance sheet and commitment to shareholder returns further strengthen the argument for upside.

- Bull Case: Undervalued P/E ratio (8x forward P/E vs. industry 11x).

- Bull Case: Strong free cash flow generation, with $837.5M in Q1 2026.

- Bull Case: Key growth projects like Great Bear and Lobo-Marte.

- Bull Case: Favorable EV/EBITDA of 7.3x compared to sector median of 7.93.

- Bear Case: Stable production guidance (2.0M oz annually) lacks significant growth catalysts.

- Bear Case: Thesis heavily reliant on sustained high gold prices.

- Bear Case: Potential for rising operating and capital costs to pressure margins.

- Bear Case: Medium-term growth is less dynamic, with Great Bear's impact not until 2030.

- Bear Case: One analyst (Jefferies) has a very conservative price target of $10.00.

Fintwit's AI verdict

Artificial intelligence models analyzing Kinross Gold's financial data and market sentiment point towards a favorable outlook. The company's valuation metrics, particularly its price-to-earnings ratio and enterprise value to EBITDA, are seen as attractive when compared to industry benchmarks and its own historical performance. Furthermore, the consistent free cash flow generation and strategic development of future production assets are key positive indicators.

While the AI acknowledges potential headwinds such as gold price volatility and the timeline for new project contributions, the overall assessment leans positive. The consensus among analysts, combined with the company's financial health and growth pipeline, suggests that the current market price may not fully reflect Kinross Gold's intrinsic value.