Cisco Systems Inc (CSCO) Q3 Earnings Preview: What to Watch

Cisco Systems (CSCO) gears up for its Q3 earnings report. Analysts anticipate robust performance fueled by AI infrastructure demand and enterprise network upgrades. Key metrics and watch items detailed.

The setup

Cisco Systems (CSCO) is expected to deliver solid results in its upcoming third-quarter earnings report. The company's performance is anticipated to be bolstered by the ongoing demand for AI infrastructure and a broader refresh cycle in enterprise networking.

Recent guidance from Cisco indicates continued positive momentum. The company has a track record of exceeding earnings per share (EPS) and revenue expectations, setting a high bar for this quarter's performance.

While the company navigates some challenges, such as memory supply constraints and the cloud transition of its recently acquired Splunk business, the overall outlook remains optimistic, with AI opportunities and strategic investments expected to fuel future growth.

Consensus numbers

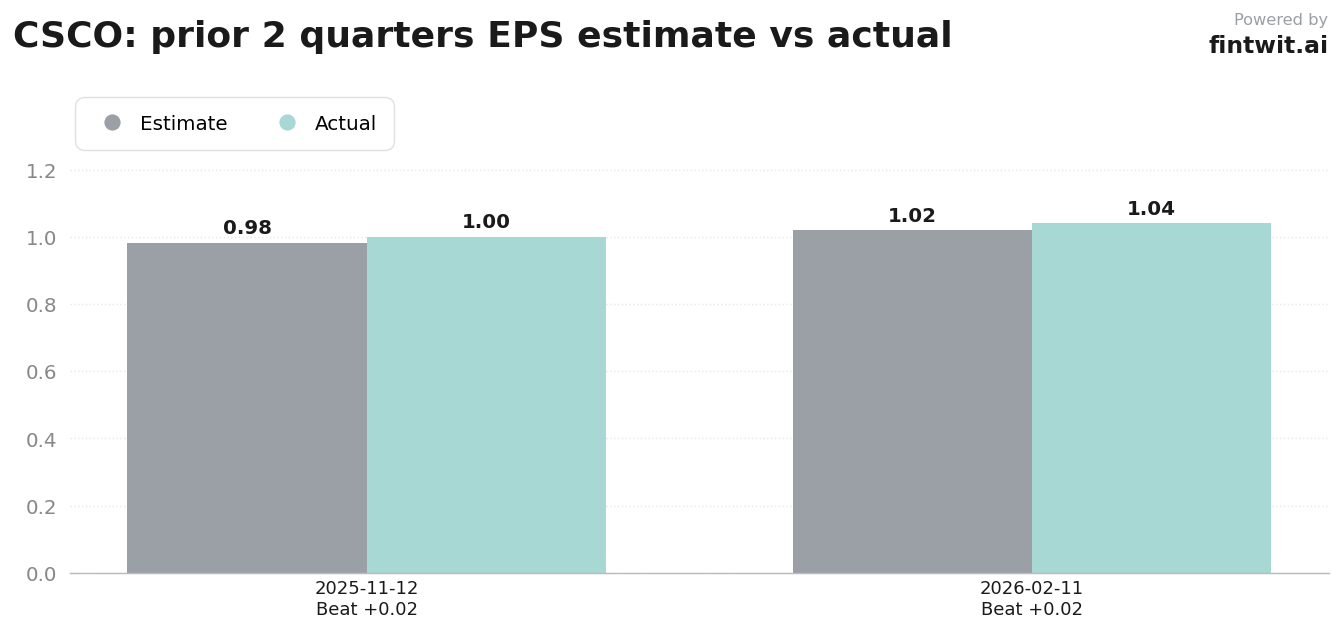

The consensus among analysts points to a beat for Cisco's third quarter. The company's history of exceeding expectations, as illustrated by the prior EPS surprises chart, suggests a likelihood of continued positive performance.

- EPS Estimate: $1.04 (vs. consensus $1.02)

- Revenue Estimate: $15.3 billion (vs. consensus $15.11 billion)

- AI Infrastructure: Expected to be a primary growth driver with significant order backlogs.

- Campus and Enterprise Networking: Demand for next-generation solutions is anticipated to contribute to growth.

- Security and Observability: Expected to show signs of stabilization and renewed growth as Splunk integration progresses.

- Beat/Miss Probability: 60% beat, 15% miss, 25% inline.

What we'll watch on the call

Investors will be keen to understand the conversion rate of AI infrastructure orders into recognized revenue. Cisco's recent guidance on February 12, 2026, projected full-year EPS between $4.13 and $4.17, exceeding the consensus of $3.80, and full-year revenue between $61.2 billion and $61.7 billion, surpassing the $60.7 billion consensus.

- Pace of AI infrastructure order conversion into recognized revenue.

- Evidence of sustained demand for next-generation campus networking solutions.

- Signs of stabilization or renewed growth in the security business post-Splunk cloud transition.

- Management's commentary on margin pressures from elevated component costs, particularly memory chips.

- Impact of the Splunk integration on revenue and profitability.

- Guidance for the fourth quarter and full fiscal year 2026, particularly concerning AI revenue streams.

Fintwit's AI verdict

The sentiment surrounding Cisco Systems (CSCO) is increasingly positive, with analysts highlighting strong AI momentum and a robust networking refresh cycle. While valuation is a consideration, the company's strategic investments and market position are seen as key drivers for sustained growth.

The market is closely observing Cisco's ability to capitalize on the AI infrastructure build-out and the successful integration of its recent acquisitions. The company's forward-looking guidance and historical performance suggest a favorable outlook for the coming quarters.