The Home Depot (HD) vs Lowe's (LOW): Which Is the Better Buy in 2026?

HD and LOW are battling for market share in a stagnant housing cycle. We break down the financials to see which stock is the superior long-term hold.

The matchup

The home improvement sector is navigating a $1.2 trillion addressable market defined by high interest rates and cautious consumer spending. The Home Depot has prioritized its Pro ecosystem, leveraging recent acquisitions like SRS Distribution and GMS to solidify its dominance with professional contractors.

Lowe's has countered with its Total Home strategy, focusing on digital integration and AI-driven customer engagement. The company's recent performance is heavily influenced by the integration of acquisitions like FBM and ADG, which have introduced both growth and margin volatility.

- The Home Depot (HD) market cap stands at $319.31 billion.

- Lowe's (LOW) market cap is significantly smaller at $126.01 billion.

- HD reported 4.8% YoY revenue growth in Q1 2026.

- LOW reported 10.3% YoY revenue growth in Q1 2026, largely driven by inorganic acquisition contributions.

Numbers side by side

Valuation metrics reveal a clear divergence in how the market prices these two retailers. HD commands a premium P/E ratio, reflecting investor confidence in its operational stability and dividend consistency.

Lowe's trades at a lower multiple, offering a potential value play if management can successfully navigate the margin dilution caused by recent integration efforts.

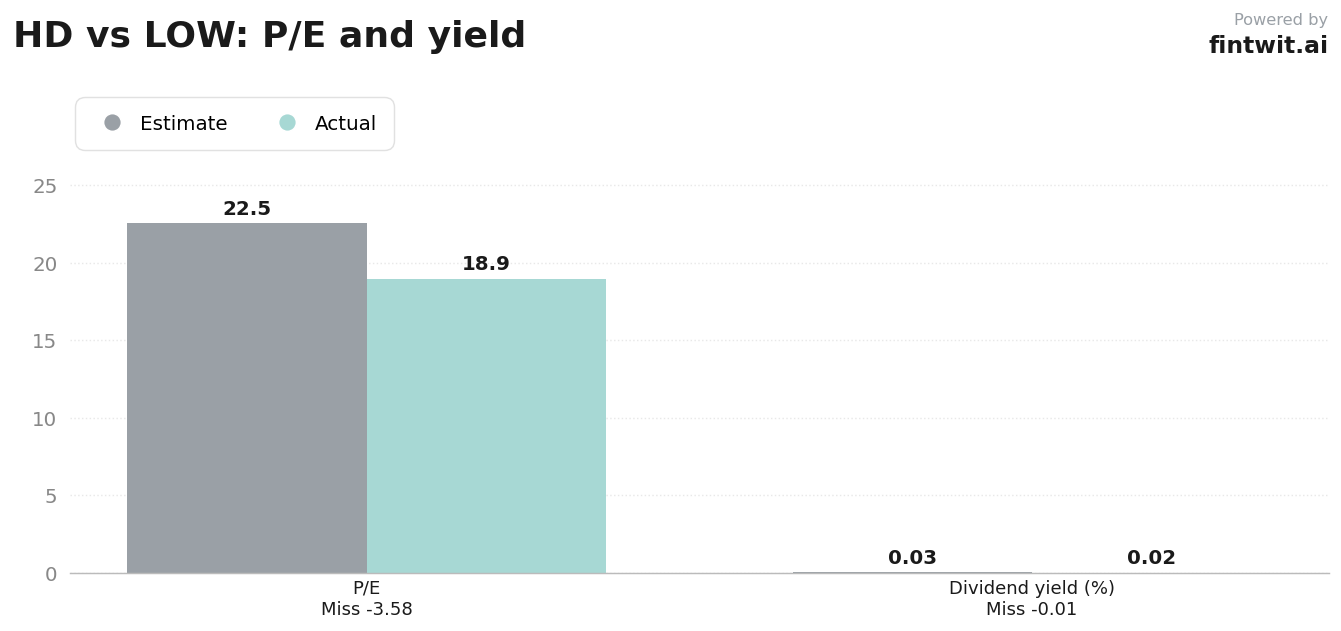

- HD P/E Ratio: 22.52x.

- LOW P/E Ratio: 18.94x.

- HD Dividend Yield: 2.81%.

- LOW Dividend Yield: 2.07%.

- HD 1-year price change: -12.66%.

- LOW 1-year price change: -3.34%.

Bull and bear on each

Analysts remain divided on the near-term trajectory for both firms. The consensus targets suggest moderate upside, provided the housing market stabilizes.

The following points summarize the primary investment theses for each ticker based on current analyst coverage.

- HD Bull Case: Successful integration of Pro-focused acquisitions driving long-term compounding.

- HD Bull Case: Resilient market share gains despite housing macro headwinds.

- HD Bear Case: Margin pressure from cost inflation and integration of lower-margin acquisitions.

- HD Bear Case: High valuation multiple relative to peers in a stagnant housing cycle.

- LOW Bull Case: Strong execution in Pro and online segments with 15.5% growth.

- LOW Bull Case: Attractive valuation relative to historical averages and peers.

- LOW Bear Case: Integration risks and margin dilution from recent acquisitions like FBM and ADG.

- LOW Bear Case: Sensitivity to high interest rates suppressing big-ticket DIY demand.

The verdict

The Home Depot remains the preferred choice for investors seeking operational stability and a mature Pro ecosystem. Its ability to maintain margins while scaling its Pro business provides a defensive buffer in a volatile housing environment.

Lowe's presents a compelling alternative if the DIY market recovers faster than the Pro segment. The company's aggressive digital transformation and disciplined capital allocation could drive significant alpha if integration costs subside.