The Home Depot Inc (HD) Q1 2026 Earnings Preview: What to Watch

Home Depot faces a cautious Q1 2026 outlook. We analyze the Pro segment, acquisition integration, and the impact of stagnant housing turnover.

The setup

Management has maintained a cautious fiscal 2026 outlook, projecting total sales growth of 2.5% to 4.5%. Comparable sales growth is expected to remain flat to 2.0%, while EPS growth is forecasted at flat to 4%.

The company has explicitly warned that first-half EPS will be negatively impacted by the annualization of recent acquisitions and timing. Leadership notes that they have not yet identified a clear catalyst for an inflection in housing activity.

Macroeconomic headwinds remain the primary narrative. Elevated mortgage rates continue to limit home improvement demand, while consumer uncertainty regarding inflation and employment costs weighs on discretionary spending.

- Jaime M. Katz of Morningstar maintains a 3-star rating with a $335.00 price target, citing integration risks.

- Truist Financial maintains a buy rating but reduced its price target to $394.00 due to sector-wide headwinds.

- TD Cowen has reiterated a buy rating, reflecting continued positive sentiment despite the challenging environment.

Consensus numbers

Wall Street consensus estimates for the first quarter of 2026 reflect a period of consolidation. Revenue is expected to reach $41.61 billion, with EPS estimated at $3.42.

The market is closely monitoring the company's ability to maintain stable sales without a broad housing market recovery. Recent history shows a mixed track record regarding earnings surprises.

The following data points summarize the current expectations and recent performance trends.

- Q1 2026 EPS Estimate: $3.42.

- Q1 2026 Revenue Estimate: $41.61 billion.

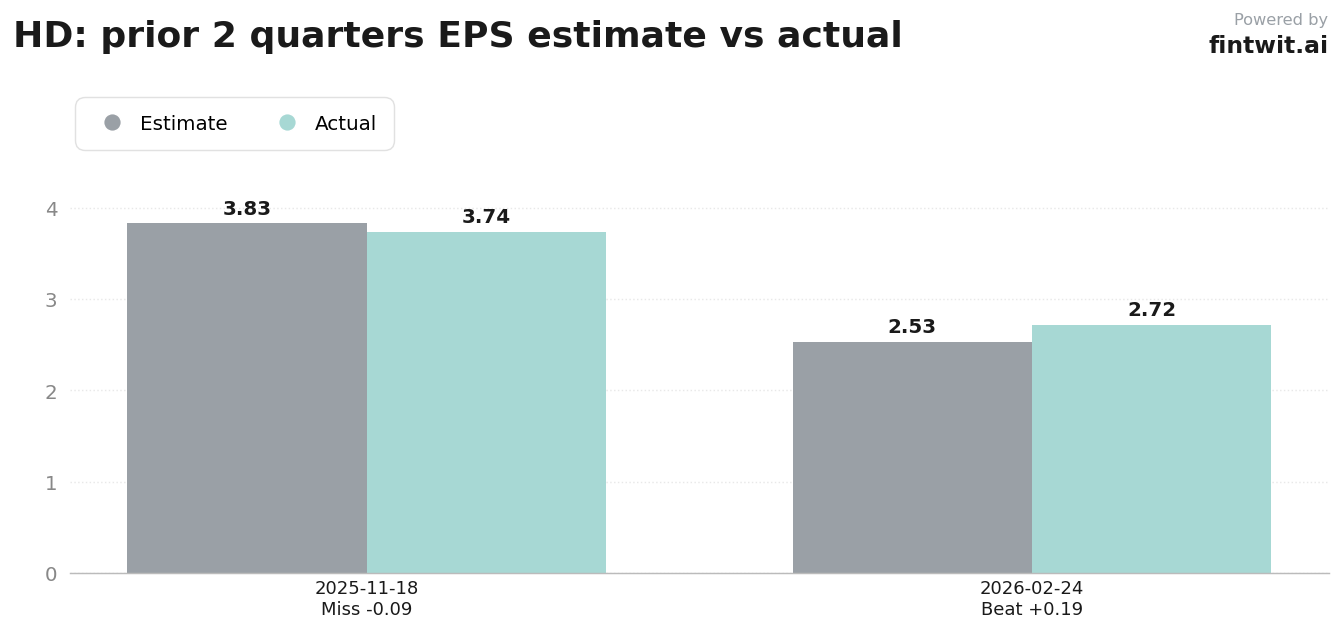

- Q4 2025 Actual EPS: $2.72 vs $2.53 estimate.

- Q3 2025 Actual EPS: $3.74 vs $3.83 estimate.

- Beat/Miss Probability: 35% chance of a beat, 45% chance of a miss, 20% chance of inline results.

What we'll watch on the call

The Pro segment remains the most critical strategic pillar for long-term growth. Analysts are looking for evidence that the integration of SRS Distribution and GMS can offset weakness in the DIY segment.

Big-ticket discretionary projects are highly sensitive to housing turnover. We will monitor management's commentary on whether consumers are shifting toward essential repair-and-maintenance tasks exclusively.

Operating margins are under pressure due to ongoing pricing investments and acquisition-related costs. Investors need clarity on how these expenses will trend throughout the remainder of the fiscal year.

- Can the company sustain positive comparable sales trends without a significant rebound in housing turnover?

- How are recent acquisitions like SRS and GMS performing in terms of contribution to the Pro ecosystem?

- Are there signs of improvement in big-ticket discretionary project demand?

- What is the specific outlook for operating margins given current pricing investments?

Fintwit's AI verdict

The sentiment surrounding the upcoming report is characterized by a blend of structural optimism regarding the Pro segment and tactical caution regarding the macro environment. While the housing market remains a significant drag, the company's strategic acquisitions provide a potential buffer that the market may be underestimating.

Investors are weighing the current valuation against the potential for a long-term recovery in home improvement activity. The upcoming earnings call will serve as a litmus test for whether the company's operational initiatives can successfully navigate these headwinds.