The Home Depot Inc (HD) Q1 2026 Earnings Preview: What to Watch

The Home Depot faces a housing market stalemate as it approaches Q1 2026 earnings. We break down the key metrics, analyst sentiment, and margin risks.

The setup

The Home Depot faces a challenging macroeconomic environment characterized by elevated mortgage rates and limited housing inventory. These factors continue to suppress big-ticket discretionary spending, which historically drives the company's top-line growth.

Management has provided a cautious outlook for fiscal 2026, projecting total sales growth between 2.5% and 4.5%. Comparable sales are expected to remain flat or grow by up to 2.0%, reflecting the ongoing uncertainty in the renovation sector.

- Management projects adjusted diluted EPS growth of 0% to 4% for the full year.

- First-half EPS faces year-over-year pressure from acquisition-related costs.

- The company is integrating large-scale acquisitions including SRS Distribution and GMS.

- Consumer sentiment remains weighed down by persistent inflation and high financing costs for large projects.

Consensus numbers

Wall Street analysts have set a cautious bar for the first quarter of 2026. The consensus estimate for earnings per share stands at $3.42, with revenue projected at $41.61 billion.

Recent analyst actions reflect a divergence in sentiment regarding the company's ability to navigate current sector headwinds. While some firms maintain buy ratings, price targets have been adjusted to account for margin compression.

- EPS Estimate: $3.42

- Revenue Estimate: $41.61 billion

- Bank of America maintains a buy rating with a $374.00 price target as of May 5, 2026.

- Truist Financial reduced its price target from $424 to $394 on May 13, 2026.

- TD Cowen reiterated a buy rating in March 2026.

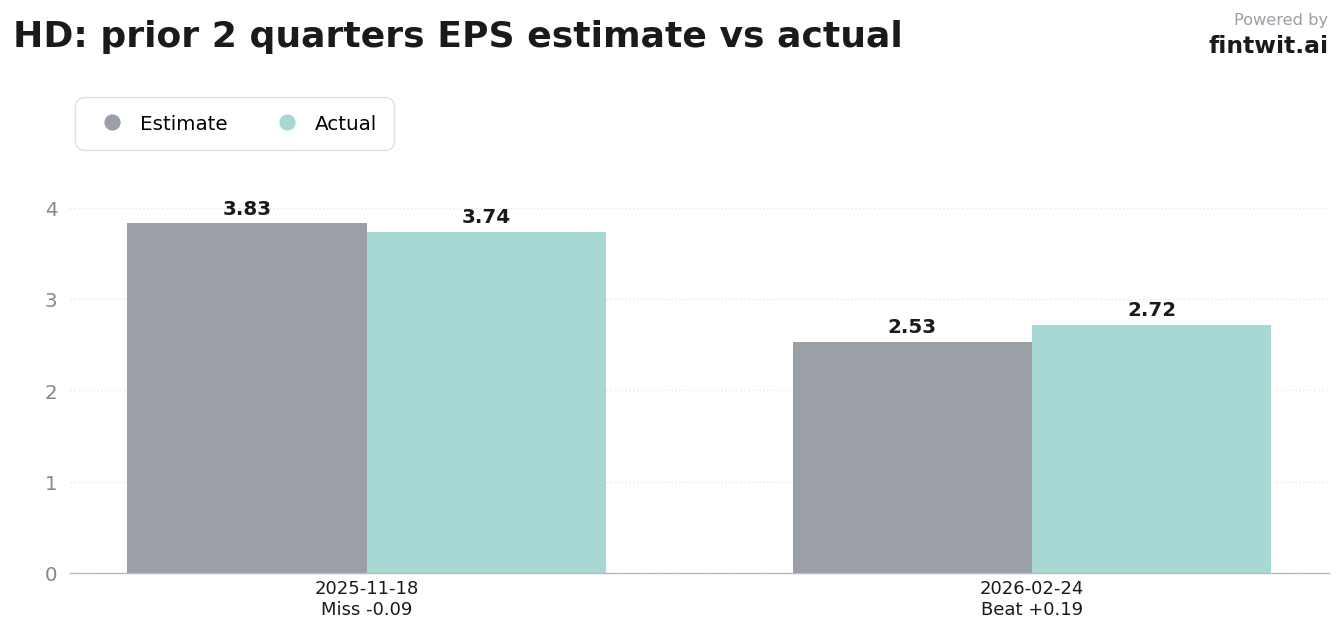

- Historical performance: Q4 2025 EPS was $2.72 vs $2.53 estimate; Q3 2025 EPS was $3.74 vs $3.83 estimate.

What we'll watch on the call

Investors are looking for evidence that the Pro segment can offset weakness in the DIY category. The performance of recent acquisitions like SRS Distribution will be a critical indicator of market share gains.

Gross margin trends remain a primary focus as the company absorbs the costs associated with its recent expansion. Analysts will scrutinize whether pricing investments are yielding the expected volume growth.

- Evidence of an inflection in housing activity or confirmation of a persistent stalemate.

- Impact of pricing investments in the SRS business on gross margins.

- Pro customer spending patterns across various categories and potential project delays.

- Current outlook for share repurchases in light of the leverage impact from recent acquisitions.

- Sensitivity of big-ticket discretionary projects to current interest rate levels.

Fintwit's AI verdict

The market sentiment surrounding the upcoming earnings release is characterized by a wait-and-see approach. While the structural long-term thesis remains intact for many institutional observers, the immediate pressure on margins and discretionary spending creates a complex backdrop for the stock.

Investors are weighing the potential for a surprise against the backdrop of a cooling housing market. The upcoming report will likely serve as a definitive gauge for whether the company can maintain its competitive edge during this cycle.