The Home Depot (HD) vs Lowe's (LOW): Which Is the Better Buy in 2026?

HD and LOW are fighting for dominance in the home improvement sector. We break down the financials and strategic outlook for both retail giants.

The matchup

The home improvement sector remains defined by the duopoly of The Home Depot and Lowe's. Both companies are currently navigating a challenging housing market characterized by low transaction volumes and high interest rates.

Home Depot has leaned into its Pro-customer strategy, which now accounts for approximately 55% of its total revenue mix. The recent integration of SRS and GMS acquisitions is designed to solidify its dominance in the professional contractor space.

Lowe's is pursuing a Total Home strategy, focusing on expanding its own Pro-segment through the FBM and ADG acquisitions. The company is attempting to close the performance gap by optimizing its store network and improving supply chain efficiency.

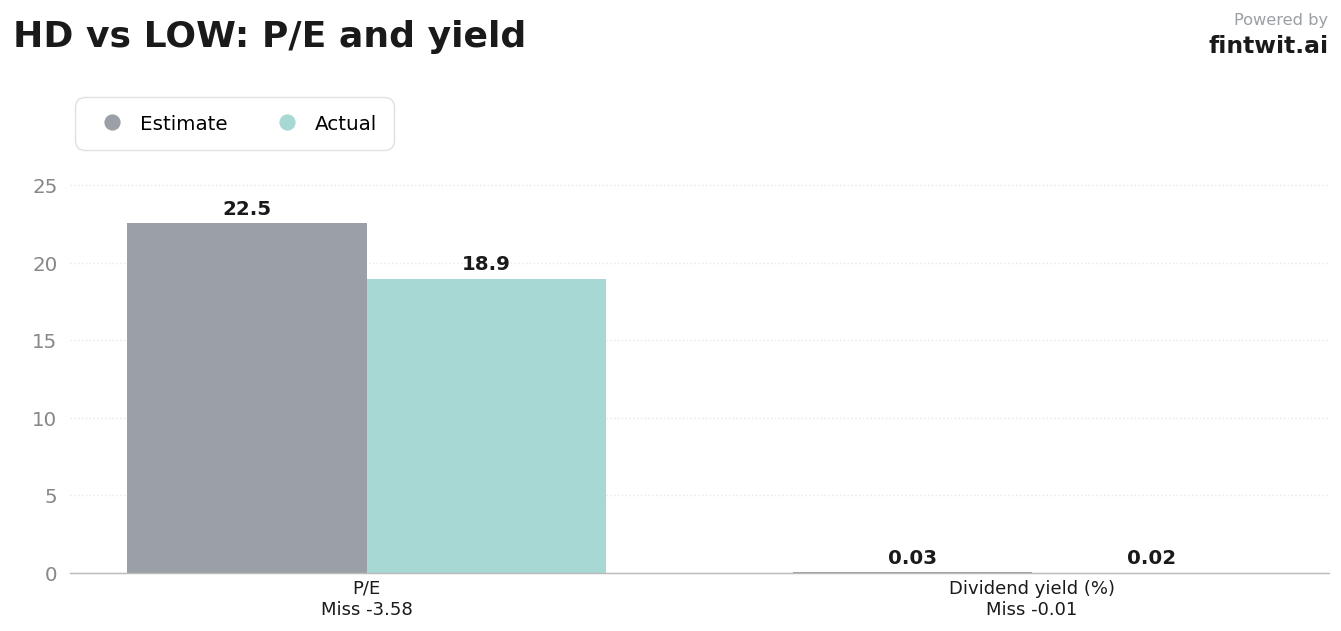

- Home Depot (HD) maintains a P/E ratio of 22.52x.

- Lowe's (LOW) trades at a more attractive P/E ratio of 18.94x.

- Home Depot's dividend yield stands at 2.81%.

- Lowe's dividend yield is currently 2.07%.

- UBS analyst Michael Lasser maintains a Buy rating on HD with a $450.00 price target.

- Citigroup analysts maintain a Buy rating on LOW with a $285.00 price target.

Numbers side by side

Financial performance for both retailers shows the impact of a cooling housing market. Home Depot reported Q4 revenue of $38.2 billion, reflecting a 3.8% decline due to calendar shifts, while Lowe's posted Q4 revenue of $20.58 billion, up 10.95% year-over-year.

Operating margins remain a key point of differentiation. Home Depot guides for adjusted operating margins between 12.8% and 13.0%, whereas Lowe's anticipates margins between 11.6% and 11.8% as it absorbs integration costs from recent acquisitions.

The following data highlights the valuation and performance divergence between the two firms.

- HD 1-year price change: -16.90%.

- LOW 1-year price change: -2.71%.

- HD 90-day price change: -20.61%.

- LOW 90-day price change: -21.88%.

- HD FY2026 projected revenue growth: 3.2%.

- LOW FY2026 projected revenue growth: 3.1%.

Bull and bear on each

Investment theses for both companies hinge on their ability to capture share in a fragmented market while managing debt and integration risks.

Home Depot's bull case rests on its fortress balance sheet and the successful scaling of its Pro-focused acquisitions. Conversely, the bear case highlights the company's vulnerability to the 'locked-in' housing effect where homeowners refuse to move or renovate.

Lowe's bull case centers on its valuation discount and the potential for margin expansion as FBM and ADG synergies materialize. The bear case focuses on the company's higher debt load and the strain on shareholders' equity.

- HD Bull: SRS/GMS integration expands total addressable market to over $1 trillion.

- HD Bull: Strong Pro-customer loyalty drives consistent share gains.

- HD Bear: Core retail business shows signs of stagnation with flat organic growth.

- LOW Bull: Valuation discount relative to HD offers significant upside potential.

- LOW Bull: Stronger recent comparable sales momentum in specific categories.

- LOW Bear: Heavy acquisition debt creates financial flexibility constraints.

- LOW Bear: Margin compression persists due to integration drag.

The verdict

Choosing between these two retailers requires balancing Home Depot's operational maturity against Lowe's potential for valuation-driven recovery. Home Depot provides a more stable foundation for investors seeking long-term exposure to the home improvement sector.

Lowe's remains a compelling alternative for those who believe the company can successfully navigate its current debt-heavy expansion phase. The outcome for both will likely be dictated by the trajectory of mortgage rates and the subsequent health of the housing market.