Deere & Company (DE) vs Caterpillar Inc (CAT): Which Is the Better Buy in 2026?

Caterpillar's data center tailwinds clash with Deere's agricultural cycle. We break down the financials to find the superior industrial play.

The matchup

Deere & Company remains the dominant force in high-horsepower agricultural equipment, leveraging a proprietary software ecosystem to drive long-term retention. The company is currently navigating a cyclical trough in North American large-ag demand, which has pressured recent operating margins to 16.9%.

Caterpillar Inc is currently benefiting from a massive $63 billion backlog, fueled by unprecedented demand for power-generation equipment in AI data centers. The company reported 22% year-over-year revenue growth in Q1 2026, signaling a structural shift in its end-market exposure toward energy and infrastructure.

- Deere & Company (DE): Market cap of $166.93 billion with a focus on precision agriculture and autonomous machinery.

- Caterpillar Inc (CAT): Market cap of $318.64 billion with a diversified footprint in construction, mining, and power generation.

- Strategic Divergence: DE is tied to agricultural commodity cycles, while CAT is increasingly tethered to the secular growth of data center energy infrastructure.

Numbers side by side

The valuation gap between the two firms reflects their current growth trajectories and market sentiment regarding their respective end-markets. Caterpillar commands a higher price-to-earnings ratio, reflecting investor confidence in its backlog and power-gen exposure.

Deere's lower P/E ratio suggests a market waiting for a recovery in the agricultural sector before assigning a higher multiple to its precision technology segment.

- Price: DE $579.25 vs CAT $909.81.

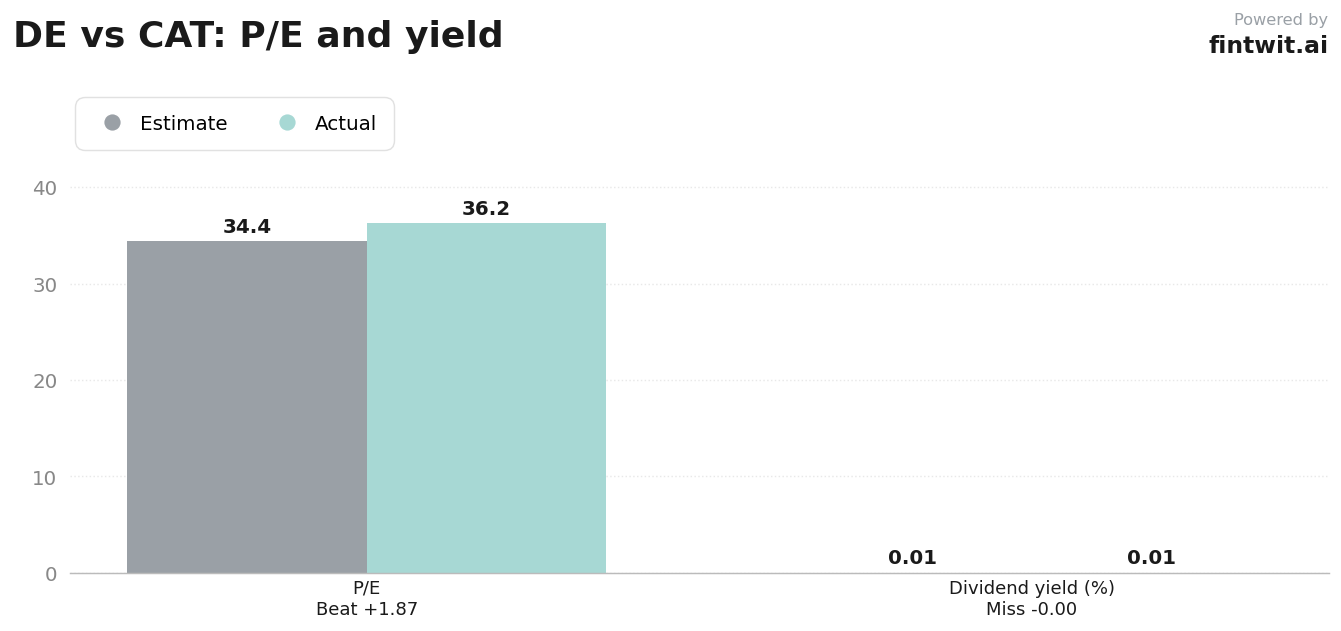

- P/E Ratio: DE 34.37 vs CAT 36.24.

- Revenue Growth: DE 5% YoY (Q2 2026) vs CAT 22% YoY (Q1 2026).

- Operating Margin: DE 16.9% vs CAT 18.0%.

- Dividend Yield: DE 1.06% vs CAT 0.86%.

Bull and bear on each

Analysts remain divided on the sustainability of the current industrial cycle, particularly as tariff-related manufacturing costs impact both firms. The following points summarize the core arguments for and against each industrial giant.

- DE Bull Case: Successful monetization of precision agriculture software and autonomous solutions.

- DE Bull Case: Recovery in large agricultural equipment demand following the 2026 cycle trough.

- DE Bear Case: Prolonged weakness in North American large-ag demand.

- DE Bear Case: Regulatory and legal challenges to the proprietary service model.

- CAT Bull Case: Surging demand for power-generation equipment tied to AI data centers.

- CAT Bull Case: Record $63 billion backlog providing high revenue visibility.

- CAT Bear Case: High sensitivity to global GDP and commodity prices.

- CAT Bear Case: Significant tariff-related cost headwinds projected for 2026.

The verdict

Caterpillar's strategic pivot toward AI-driven power infrastructure provides a superior growth momentum that currently outweighs the cyclical agricultural headwinds facing Deere. While Deere offers a compelling long-term play on precision agriculture, the immediate revenue visibility provided by Caterpillar's backlog makes it the more attractive option for investors seeking growth in 2026.

A sharp recovery in global agricultural commodity prices and rapid adoption of Deere's high-margin precision ag software could lead to a significant valuation re-rating for DE, potentially narrowing the gap with Caterpillar. Investors should monitor these variables closely as the fiscal year progresses.