The Cheapest Large Caps Right Now: A P/E Screen

A look at ten large-cap stocks with P/E ratios under 8, evaluating the fundamental drivers behind their current market valuations.

How we screened

This screen identifies large-cap equities with market capitalizations exceeding $10 billion and P/E ratios below 8.0. We prioritize companies with significant free cash flow generation to distinguish between genuine value plays and potential value traps.

The data set focuses on companies where market sentiment has diverged from fundamental cash flow metrics. We categorize these discounts as either earned, where structural headwinds justify the low multiple, or unearned, where market overreaction may present an opportunity.

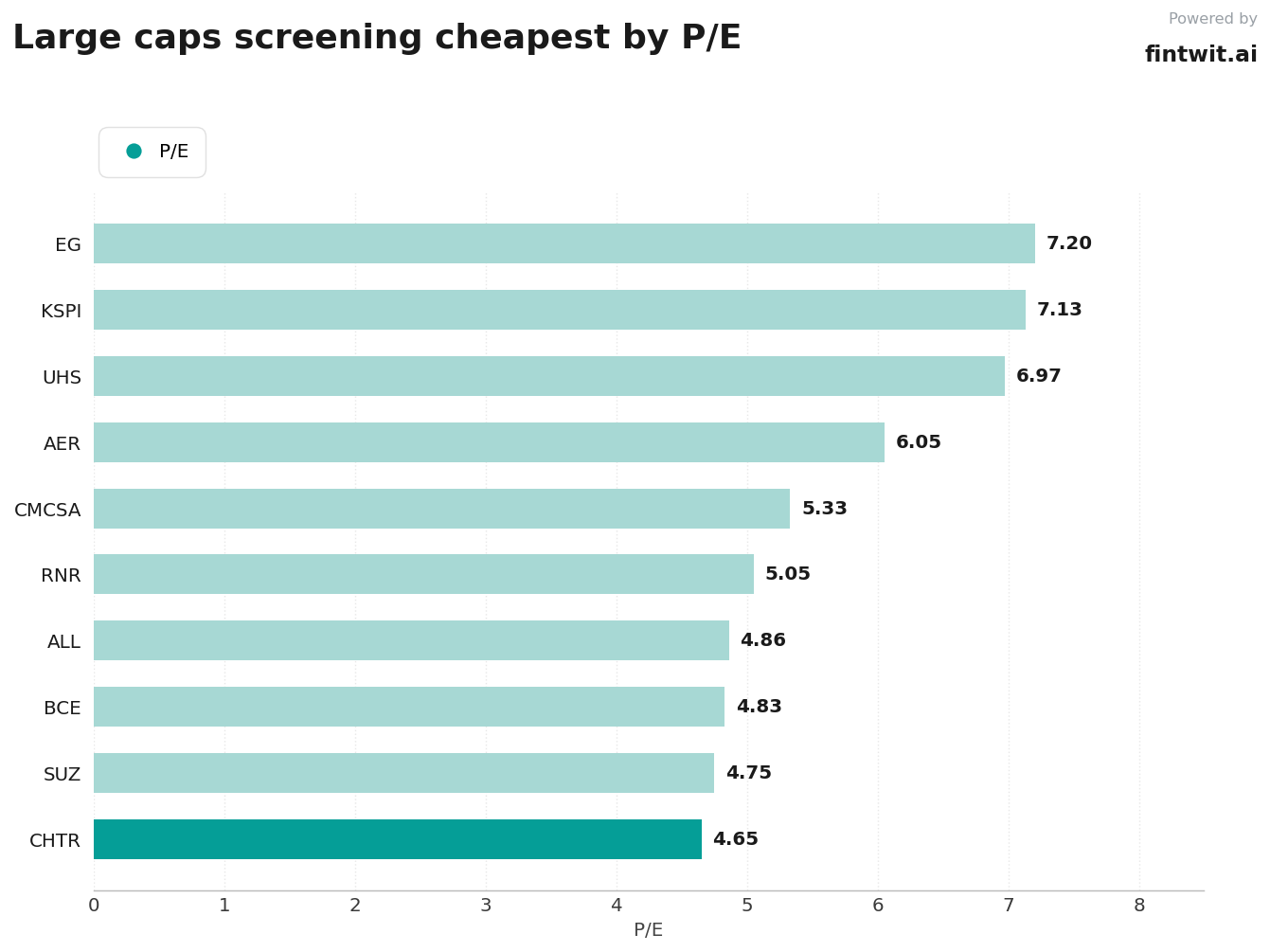

The list

The following list highlights ten companies currently trading at low multiples relative to their earnings. These valuations reflect varying degrees of market skepticism regarding future growth and sector-specific risks.

- Charter Communications (CHTR): 4.65 P/E. Earned discount due to broadband subscriber decline and high leverage. Bernstein cites ongoing pressure on fundamentals.

- Suzano (SUZ): 4.75 P/E. Unearned discount driven by cyclical pulp price volatility. Seeking Alpha notes the capital cycle is shifting toward harvest mode.

- BCE Inc (BCE): 4.83 P/E. Earned discount following a significant dividend cut and intense Canadian telecom competition.

- Allstate (ALL): 4.86 P/E. Unearned discount despite strong underwriting profitability. KBW downgraded the stock citing a peak in auto policy growth.

- Renaissancere (RNR): 5.05 P/E. Unearned discount. Citi argues the company is well-positioned to handle both benign and elevated catastrophe losses.

- Comcast (CMCSA): 5.33 P/E. Unearned discount. Reddit value investors highlight $19.2 billion in annual FCF against market fears of decline.

- AerCap (AER): 6.05 P/E. Unearned discount. Sentiment-driven pressure rather than fundamental weakness in the leasing business.

- Universal Health Services (UHS): 6.97 P/E. Earned discount due to ongoing regulatory and legal scrutiny regarding patient safety.

- Kaspi.kz (KSPI): 7.13 P/E. Earned discount reflecting macro uncertainty in Kazakhstan and currency volatility.

- Everest Group (EG): 7.20 P/E. Unearned discount. Disciplined terms in the hard reinsurance market support the current valuation gap.

Caveats

Low P/E ratios are frequently a signal of underlying business deterioration rather than a bargain. Investors must distinguish between cyclical troughs and permanent impairment of the business model.

Debt levels and interest coverage ratios are critical for companies like Charter and BCE. A low earnings multiple provides no protection if a company faces a liquidity crisis or a forced deleveraging event.

- High free cash flow yield can be misleading if capital expenditures are deferred or if the company faces significant litigation liabilities.

- Regulatory risks in sectors like healthcare and telecom can permanently compress valuation multiples regardless of current earnings performance.

- Currency volatility and geopolitical exposure for international ADRs like Kaspi.kz and Suzano introduce risks not captured in standard P/E metrics.

How to use this screen

Use this list as a starting point for fundamental analysis rather than a buy list. Compare the free cash flow yield against the P/E ratio to identify companies that are generating more cash than their earnings suggest.

Verify the sustainability of the dividend yield for companies like BCE and Comcast, as high yields in low-P/E stocks often precede dividend cuts. Focus on companies where the discount is unearned, as these offer the highest potential for multiple expansion when market sentiment shifts.