The Boeing Company (BA) vs Lockheed Martin (LMT): Which Is the Better Buy in 2026?

Comparing BA and LMT: A deep dive into the duopoly of commercial aerospace versus the stability of government-backed defense platforms.

The matchup

Boeing operates as a critical player in the commercial aerospace duopoly, currently managing a massive $695 billion backlog. The company is navigating a complex turnaround focused on stabilizing the 737 MAX and 787 production lines.

Lockheed Martin maintains a dominant position in the defense sector, anchored by the F-35 program and long-term missile defense contracts. Its business model relies on a $186 billion backlog and consistent government sustainment work.

- Boeing faces significant execution risks including FAA regulatory scrutiny and a $46.9 billion debt load.

- Lockheed Martin faces customer concentration risks, with 93% of its revenue derived from government contracts.

- Boeing aims for positive BCA operating margins by mid-2027.

- Lockheed Martin prioritizes capital allocation through consistent dividends and share buybacks.

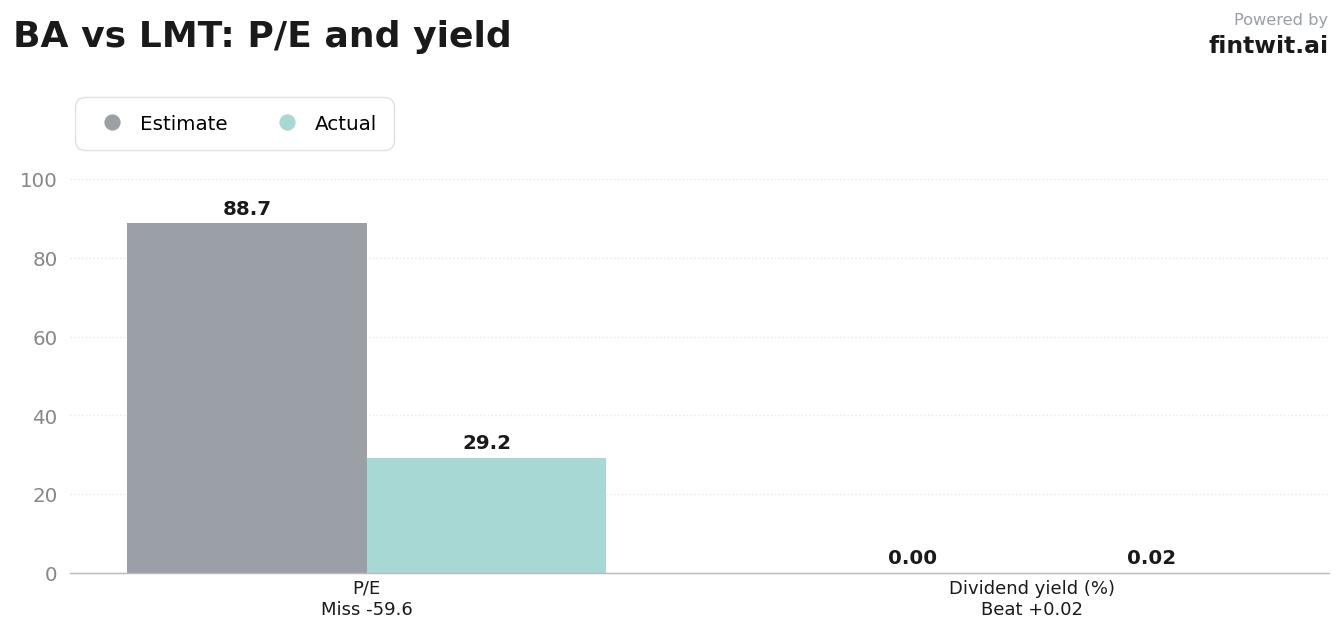

Numbers side by side

The financial profiles of these two industrial giants diverge significantly, reflecting their different operational stages and market roles. Boeing is currently priced for a turnaround, while Lockheed Martin reflects the valuation of a mature defense contractor.

See the valuation-side-by-side chart below for a direct comparison of key metrics.

- Boeing (BA) P/E Ratio: 88.73

- Lockheed Martin (LMT) P/E Ratio: 29.16

- Boeing (BA) Revenue Growth: 14% YoY (Q1 2026)

- Lockheed Martin (LMT) Revenue Growth: 0% YoY (Q1 2026)

- Boeing (BA) 1-Year Price Change: 13.60%

- Lockheed Martin (LMT) 1-Year Price Change: 11.81%

- Lockheed Martin (LMT) Dividend Yield: 2.09%

Bull and bear on each

The investment thesis for both companies hinges on their ability to manage specific operational and macroeconomic headwinds.

Analysts remain divided on the timing of a full recovery for Boeing versus the growth ceiling for Lockheed Martin.

- BA Bull: Successful 737 MAX and 787 production ramps will drive significant free cash flow inflection.

- BA Bull: Vertical integration via the Spirit AeroSystems acquisition improves long-term quality control.

- BA Bear: Persistent execution risks and ongoing losses on fixed-price defense contracts pressure margins.

- LMT Bull: Strong demand for next-gen defense platforms and munitions supports multi-year revenue visibility.

- LMT Bull: Disciplined capital allocation provides a reliable floor for shareholder returns.

- LMT Bear: High government revenue concentration creates vulnerability to federal budget shifts.

The verdict

Choosing between these two requires an assessment of risk appetite. Boeing offers high-beta exposure to a potential industrial recovery, while Lockheed Martin provides a defensive hedge with predictable cash flows.

Investors should monitor the upcoming quarterly production reports to gauge whether Boeing can meet its margin targets or if Lockheed Martin will face further pressure from government spending caps.