Amazon.com Inc (AMZN) vs Walmart Inc. (WMT): Which Is the Better Buy in 2026?

Amazon's cloud-driven growth faces off against Walmart's omnichannel retail dominance. We break down the numbers to find the better buy.

The matchup

Amazon operates a high-margin flywheel centered on AWS and advertising, which currently drives 17% year-over-year revenue growth. The company is aggressively scaling its infrastructure to support AI demand, positioning itself as the primary utility layer for the modern digital economy.

Walmart relies on its massive physical footprint to execute an omnichannel strategy that saw 24% e-commerce growth in Q4 2026. The firm is pivoting toward high-margin retail media through Walmart Connect to diversify away from thin-margin grocery sales.

- Amazon market capitalization stands at $2.27 trillion.

- Walmart market capitalization stands at $948.88 billion.

- Amazon revenue growth is 17% YoY as of Q1 2026.

- Walmart revenue growth is 5.6% YoY as of Q4 2026.

- Amazon operates in the high-growth internet retail and cloud sectors.

- Walmart maintains a defensive position in the discount store industry.

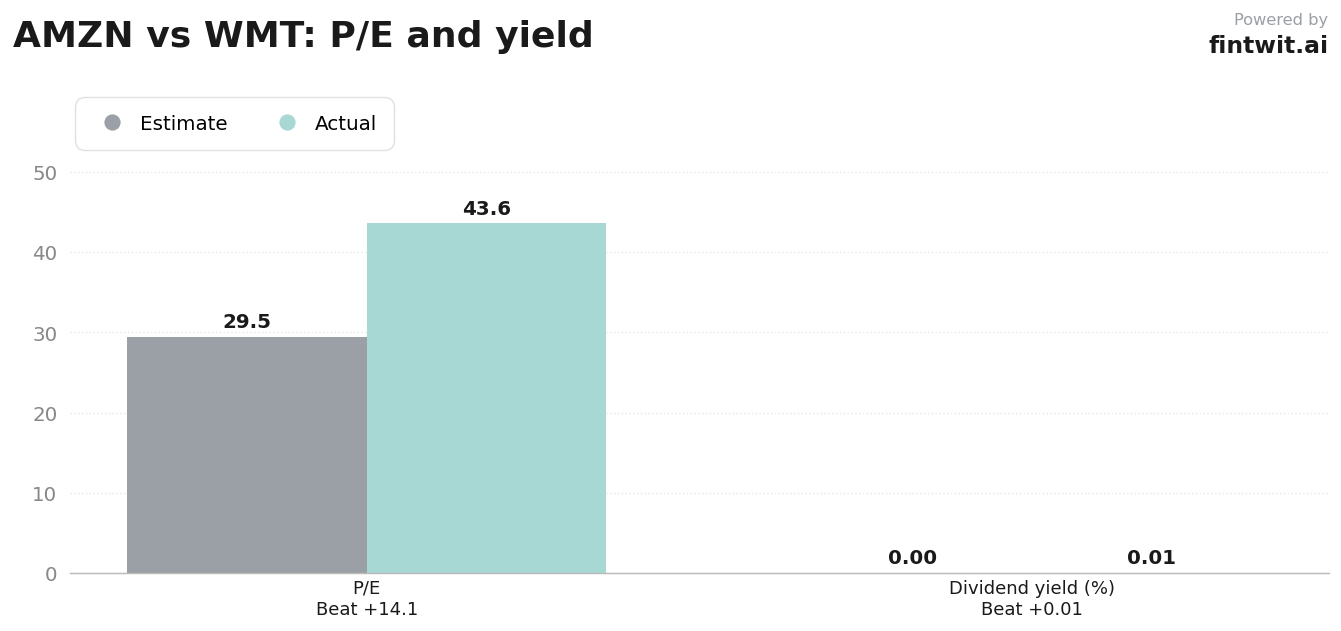

Numbers side by side

Valuation metrics reveal a significant divergence in how the market prices these two retail giants. Amazon trades at a P/E ratio of 29.49, reflecting its status as a growth-oriented technology play.

Walmart commands a higher P/E ratio of 43.60, suggesting investors are paying a premium for its defensive stability and consistent dividend yield of 0.78%.

- Amazon P/E ratio: 29.49.

- Walmart P/E ratio: 43.60.

- Amazon 1-year stock performance: +27.08%.

- Walmart 1-year stock performance: +37.22%.

- Amazon 90-day stock performance: +23.43%.

- Walmart 90-day stock performance: +9.11%.

Bull and bear on each

Amazon's bull case rests on AWS reacceleration driven by AI demand and custom silicon efficiency. Conversely, bears point to the massive $200 billion annual capex cycle that threatens near-term free cash flow.

Walmart's bull case is built on successful omnichannel pivots and the growth of Walmart Connect. Bears highlight the structural limitations on pricing power and the high capital intensity required to maintain physical automation.

- AMZN Bull: AWS reacceleration and high-margin advertising growth.

- AMZN Bear: $200B annual capex pressuring profitability.

- AMZN Bear: Heightened regulatory and antitrust scrutiny.

- WMT Bull: Omnichannel delivery driving market share gains.

- WMT Bull: Rapid growth in retail media and membership services.

- WMT Bear: Structural limits on pricing power in value retail.

- WMT Bear: Potential margin dilution from e-commerce fulfillment costs.

The verdict

Amazon offers superior growth potential through its high-margin cloud and advertising segments, whereas Walmart remains a defensive, lower-growth retail play. The choice depends on whether an investor prioritizes aggressive expansion or capital preservation.

Walmart could outperform if a prolonged economic downturn forces consumers to trade down aggressively to value retailers while simultaneously punishing Amazon's high-capex valuation. Analysts remain generally bullish on both, with targets reflecting current market sentiment.

- TD Cowen analyst John Blackledge maintains a Buy rating on AMZN with a $350.00 target.

- Stifel analyst Mark Kelley maintains a Buy rating on AMZN with a $319.00 target.

- RBC analyst Brad Erickson maintains a Buy rating on AMZN with a $320.00 target.

- Truist Securities analyst Scot Ciccarelli maintains a Buy rating on WMT with a $150.00 target.

- RBC Capital analyst Steven Shemesh maintains a Hold rating on WMT with a $62.00 target.