Zscaler Inc (ZS) Q3 Earnings Preview: What to Watch

Zscaler enters Q3 with 40 upward EPS revisions. We analyze the key metrics, competitive pressures, and management guidance ahead of the May 26 report.

The setup

Zscaler enters the Q3 print with significant momentum, evidenced by 40 upward EPS revisions over the last three months. The company is currently valued at a $24.35 billion market capitalization, reflecting investor confidence in its long-term Zero Trust strategy.

Management faces a complex environment characterized by enterprise IT budget scrutiny and shifting competitive dynamics. While the firm remains a primary player in cloud security, the market is closely watching for signs of organic growth deceleration.

- Management previously guided for Q3 fiscal 2026 EPS of $1.00 to $1.01.

- Revenue guidance for the quarter is set between $834 million and $836 million.

- The company maintains a strong footprint with over 45% of Fortune 500 companies as existing customers.

- Non-seat-based pricing now accounts for more than 25% of new annual contract value.

Consensus numbers

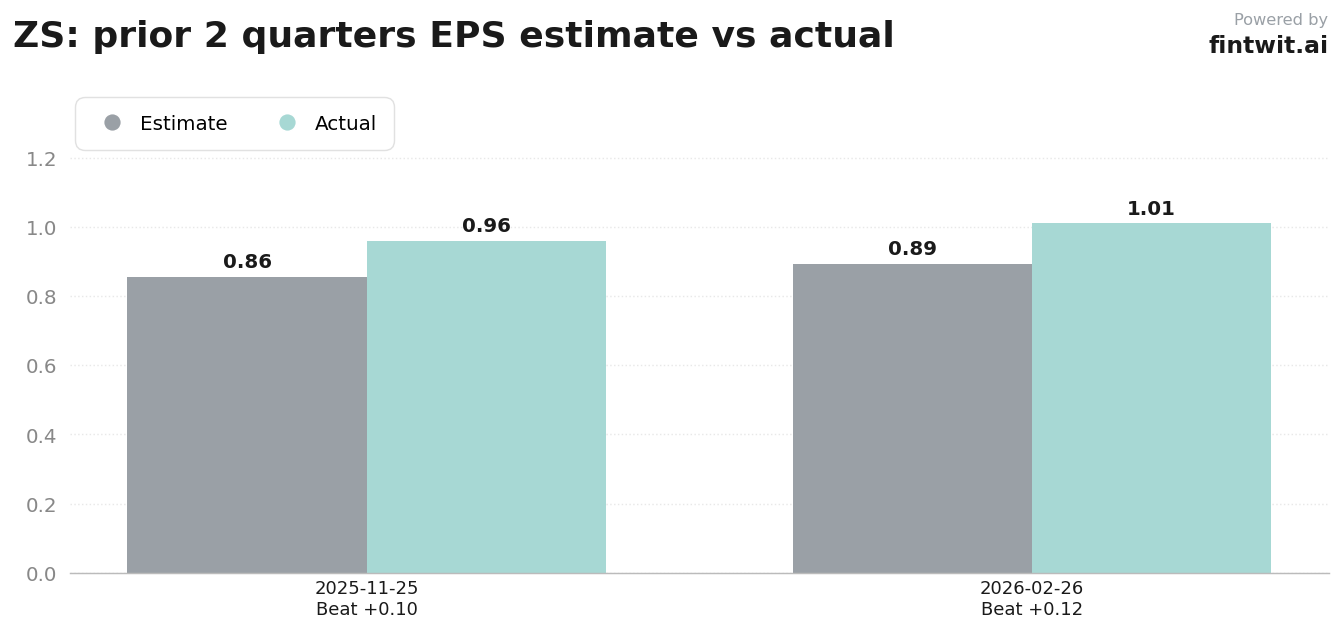

Wall Street consensus currently sits at $1.01 EPS and $835.6 million in revenue for the third quarter. The company has a history of exceeding expectations, having posted $0.96 EPS against an $0.856 estimate in November 2025 and $1.01 against $0.894 in February 2026.

Analyst sentiment remains split but generally constructive. Cantor Fitzgerald maintains an Overweight rating with a $300 price target, while KeyBanc recently raised its target to $190 from $160.

- Consensus EPS: $1.01

- Consensus Revenue: $835.6M

- Cantor Fitzgerald Rating: Overweight ($300 target)

- KeyBanc Rating: Overweight ($190 target)

- Guggenheim Rating: Neutral

What we'll watch on the call

Investors are looking for clarity on whether Zscaler can accelerate organic net new ARR growth beyond the 10% pace observed in the first half of the fiscal year. The integration of recent acquisitions, including SquareX and Symmetry Systems, remains a focal point for assessing future product scalability.

The competitive landscape in the mid-market is another area of concern. Analysts are questioning whether rivals like Cloudflare and Netskope are exerting downward pressure on pricing power.

- AI Security ARR performance, with management targeting over $500 million in FY2026.

- Conversion rates of AI-driven demand into booked ARR.

- Progress on Federal sector bookings and potential stabilization.

- Impact of non-seat-based pricing models on long-term revenue scalability.

Fintwit's AI verdict

The quantitative models suggest a favorable setup for the upcoming print, driven by consistent earnings beats and strong enterprise adoption. While macroeconomic headwinds persist, the underlying demand for secure cloud infrastructure appears to provide a floor for the company's valuation.

Investors should weigh the potential for a guidance raise against the risks of increased competition in the cybersecurity space. The path forward depends on the company's ability to maintain its premium growth profile in a tightening IT spending environment.