Streaming and Media Sector Analysis: NFLX, DIS, WBD, SPOT, ROKU

Streaming is entering a stabilization phase where scale and AI-driven personalization define the winners. We analyze the key players and structural risks.

The thesis

The streaming industry has transitioned into a phase defined by profitability and consolidation. Scale, ad-supported monetization, and retention engineering are now the primary drivers of shareholder value.

As the market matures, power is shifting toward platform-level infrastructure and AI-driven discovery. Content providers are being forced to prioritize efficiency, bundling, and sustainable margins over sheer content volume.

Why now

Michael Nathanson of MoffettNathanson notes that the migration from profitable pay TV to unprofitable streaming has created a reckoning for subscale players. While Netflix and Disney have achieved scale, others are struggling to bridge the gap between content spend and revenue.

The industry is entering a period of stabilization where winners will be defined by their ability to integrate AI-driven personalization and manage churn through strategic bundling. Ad-tier optimization is now the central lever for maximizing average revenue per user (ARPU).

Stocks we're watching

The following companies represent the core pillars of the evolving media landscape, ranging from dominant incumbents to critical infrastructure providers.

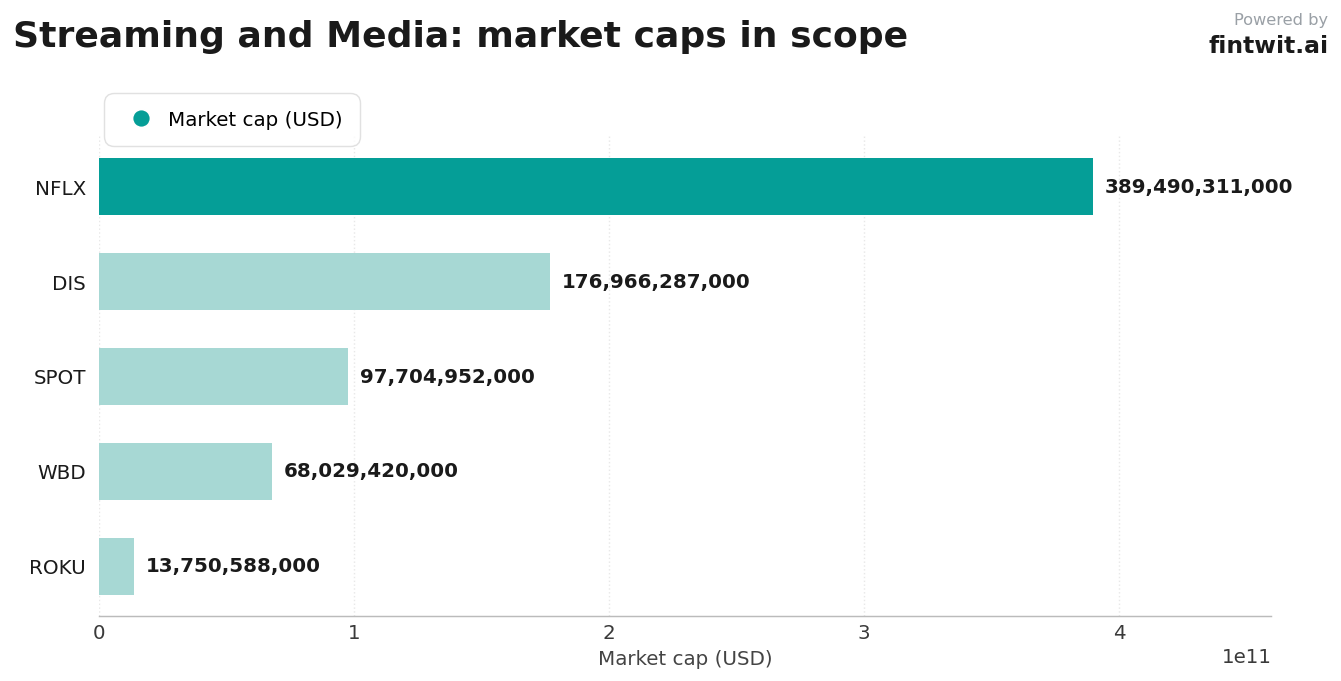

Market capitalization data for these firms is summarized in the chart below.

- Netflix (NFLX): The scale leader, setting industry standards in content and ad-supported growth with a market cap of $389.49 billion.

- Walt Disney Company (DIS): The legacy pivot, leveraging a vast IP library and sports assets to build a profitable streaming ecosystem worth $176.97 billion.

- Warner Bros Discovery (WBD): A critical M&A target whose studio and streaming portfolio is central to the industry's structural realignment, currently valued at $68.03 billion.

- Spotify Technology (SPOT): The audio aggregator, benefiting from the trend of bundling non-video services to combat subscription fatigue, with a $97.70 billion market cap.

- Roku (ROKU): The infrastructure gatekeeper, benefiting from the shift toward OS-level discovery and the expansion of free ad-supported streaming television (FAST), valued at $13.75 billion.

Risks that break it

Investors should monitor several structural headwinds that could derail the current path toward profitability.

These risks are primarily centered on competitive dynamics and regulatory hurdles.

- OS-level AI gatekeepers are shifting discovery power away from individual streaming apps, reducing direct audience control.

- Intensifying subscription fatigue and market saturation are forcing an over-reliance on lower-margin ad-supported tiers.

- Regulatory and competitive hurdles in M&A activity remain a significant barrier for subscale players attempting to achieve necessary economies of scale.