Should You Buy MRNA Right Now? Moderna Stock Analysis

Moderna shares are up 143% over the last year. We break down the recent FDA briefing, analyst sentiment, and the path forward for the mRNA pipeline.

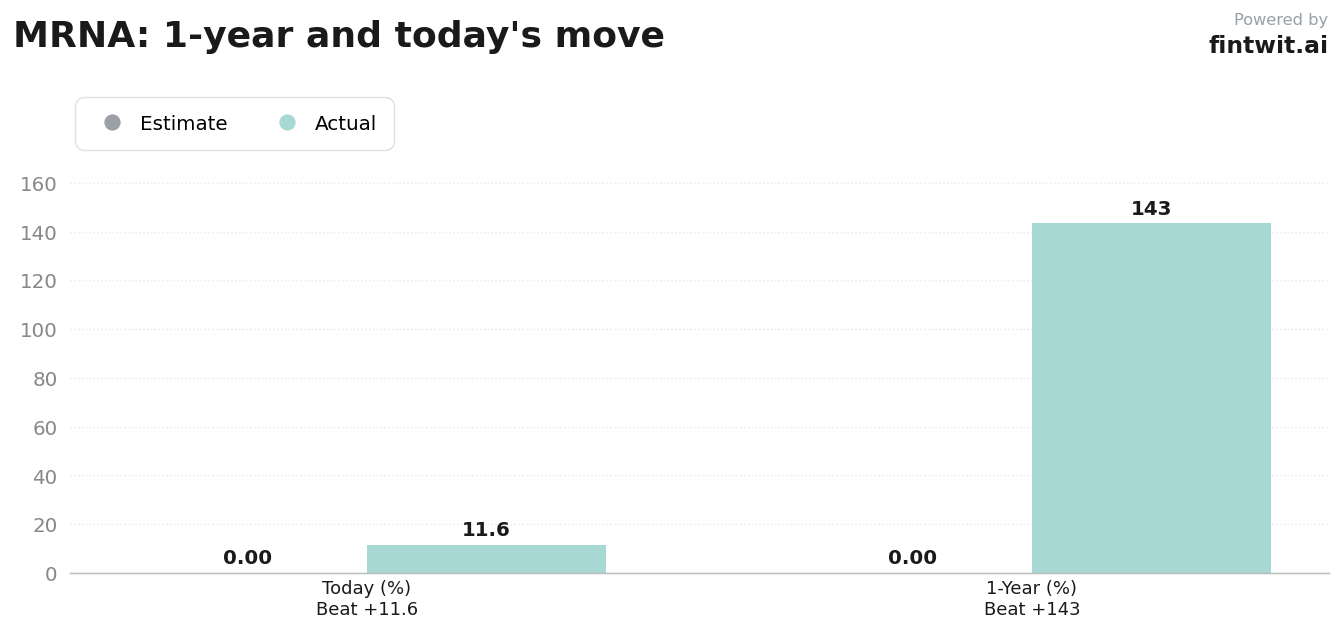

What just happened

The market reacted sharply to the release of FDA briefing documents for mRNA-1010, Moderna's seasonal flu vaccine candidate. The documents suggested that the clinical data provided by the company was sufficient to support the regulatory review process ahead of the June 18 advisory committee meeting.

This development serves as a critical milestone for Moderna as it attempts to diversify its revenue stream beyond the COVID-19 franchise. The stock's 143% gain over the past 12 months highlights a significant shift in market sentiment regarding the company's long-term commercial viability.

Investors are now looking toward the June 18 committee meeting to confirm if the FDA will maintain this positive trajectory. The current price action suggests that the market is pricing in a high probability of a successful advisory panel vote.

Bull case

The bull thesis centers on the successful transition of Moderna from a single-product company to a diversified mRNA platform. Analysts point to the pipeline depth as the primary driver for sustained valuation growth.

Key pillars of the bull case include:

- Successful Phase 3 interim results for the mRNA-4157 melanoma vaccine are expected in H2 2026.

- The company has undergone a leadership restructuring specifically designed to improve commercial scaling and operational efficiency.

- The PDUFA target action date for the seasonal flu vaccine (mRNA-1010) is set for August 5, 2026.

- Moderna's cash position remains strong, allowing for continued heavy reinvestment into high-potential R&D projects.

- The company is scheduled to host an Investor Science Day on June 25, 2026, which may provide further clarity on platform expansion.

Bear case

Skeptics argue that the current valuation is disconnected from near-term revenue realities. Despite the recent surge, the company remains unprofitable with a P/E ratio that is currently not applicable due to negative earnings.

Concerns from the analyst community include:

- Jefferies maintains a Hold rating with a $45 price target, citing balanced risks regarding the flu vaccine's commercial potential.

- Bank of America analyst Dimple Gosai maintains an Underperform rating with a $34 price target, despite acknowledging the positive FDA briefing.

- UBS analyst Eliana Merle holds a Neutral rating with a $45 target, noting that significant revenue from the melanoma program is not expected until 2026.

- Some technical indicators suggest the stock may be overbought following the 143% year-to-date rally.

- The company faces intense competition in the respiratory vaccine space from established players with larger commercial footprints.

Fintwit's AI verdict

The algorithmic consensus for Moderna is currently leaning toward a specific directional bias, driven by the recent influx of positive regulatory data and the company's aggressive pivot toward oncology. While the valuation metrics remain stretched by traditional standards, the model prioritizes the momentum of the pipeline catalysts over current earnings deficits.

The following assessment synthesizes the interplay between the upcoming June 18 advisory committee meeting and the long-term potential of the mRNA-4157 program.