Should You Buy Guardant Health (GH) After Its 17% Post-Earnings Surge?

Guardant Health shares surged 17% on strong Q1 results. We break down the bull and bear cases for this high-growth diagnostics player.

What just happened

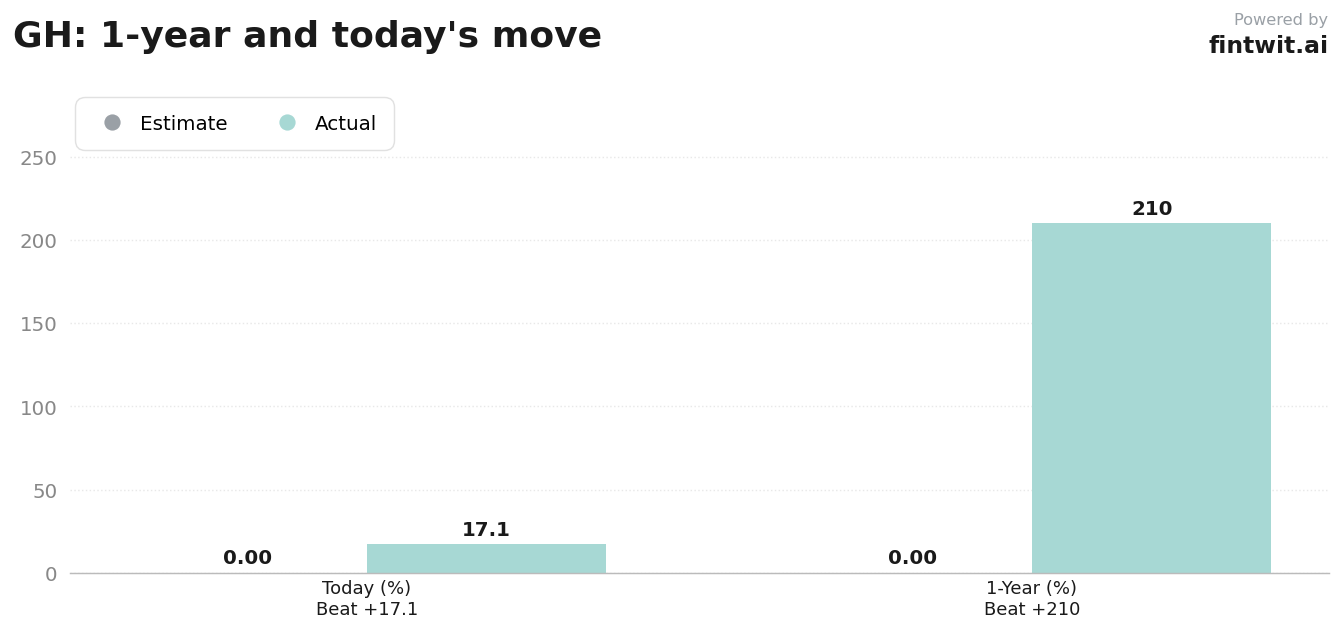

The stock price jumped to $114.97 following the release of Q1 results that exceeded market expectations. Investors responded to the explosive adoption of the Shield colorectal cancer screening test, which saw volume growth exceeding 600% year-over-year.

This rally pushed the stock out of its previous consolidation range of $80 to $95. The company is now trading at its highest levels in over a year, supported by 48% year-over-year revenue growth.

Bull case

Bullish analysts point to the company's dominant position in the liquid biopsy market as a primary driver for long-term valuation expansion. The firm is successfully scaling its oncology testing business while simultaneously penetrating the broader screening market.

The following factors support the current bullish momentum:

- JPMorgan analyst Casey Woodring maintains an Overweight rating with a $135 target, citing leadership in next-generation sequencing.

- Barclays analyst Luke Sergott holds an Overweight rating and a $120 target, highlighting strong execution in liquid biopsy.

- Shield screening volumes grew over 600% in Q1 2026, signaling rapid market adoption.

- The new nationwide collaboration with Quest Diagnostics is expected to accelerate Shield adoption further.

- The company is transitioning to the more efficient NovaSeq X sequencing platform.

Bear case

Despite the revenue growth, the company remains unprofitable and continues to burn cash as it scales its operations. Investors focused on fundamental value or near-term profitability may find the current valuation difficult to justify.

Key risks and concerns include:

- Evercore ISI Group analyst Daniel Markowitz maintains a Hold rating with a $95 target, citing ongoing losses.

- The company currently has a P/E ratio of 0.00, reflecting its lack of net income.

- Significant cash burn remains a hurdle as the company scales its screening and MRD businesses.

- The path to cash flow breakeven remains a primary concern for conservative investors.

- Regulatory and guideline changes, such as potential American Cancer Society updates, could impact future demand.

Fintwit's AI verdict

The market's reaction to the Q1 earnings report suggests that investors are prioritizing top-line growth and market share expansion over immediate profitability. With the stock breaking out of its long-term consolidation range, the technical setup aligns with the fundamental momentum seen in the Shield screening business.

Our proprietary analysis weighs the rapid adoption of liquid biopsy technology against the persistent cash burn and lack of bottom-line earnings. The following assessment reflects the current risk-reward profile for the stock.