Should You Buy CASY Right Now? Analyzing the Casey's General Stores Surge

Casey's General Stores (CASY) hit record highs after a blowout Q4. Is the momentum sustainable or is the stock overextended?

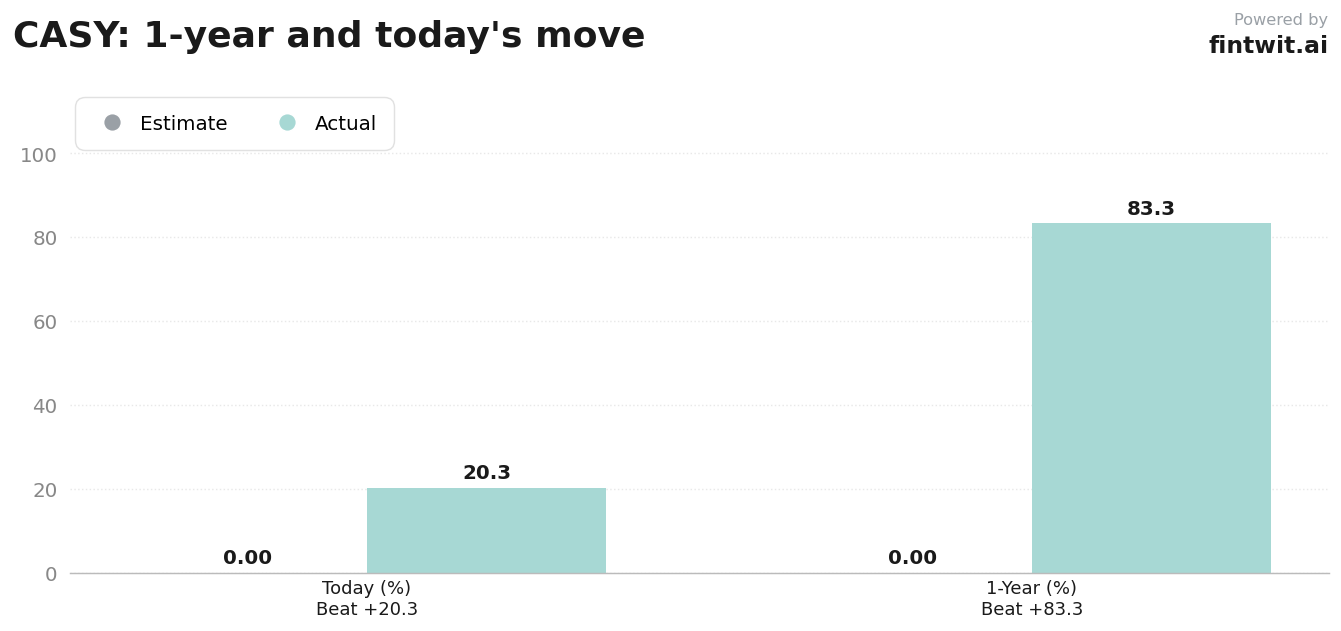

What just happened

The market reacted aggressively to the fiscal Q4 report, which showcased both top-line growth and improved operational efficiency. Investors responded to the combination of a 14% dividend hike and a new $1 billion share repurchase authorization.

The stock's 83.29% return over the past 12 months reflects a sustained period of institutional accumulation. This latest move represents a significant breakout from previous trading ranges, fueled by high volume and positive sentiment regarding the company's core fuel and food margins.

Bull case

The bullish argument centers on the company's aggressive expansion strategy and its ability to maintain high margins in a competitive retail environment. Analysts point to the following drivers for continued growth:

- Planned expansion of 120 new stores for fiscal 2027 through organic builds and strategic M&A.

- Successful integration of the CEFCO acquisition, which is expected to drive further operational efficiencies.

- A 'pizza-forward' food strategy that continues to command high margins compared to traditional convenience store offerings.

- Jefferies maintains a Buy rating with a $1,040 price target, citing the company's strong value proposition.

- Wells Fargo maintains an Overweight rating and recently raised its price target to $910.

Bear case

Despite the strong performance, valuation concerns are becoming increasingly prominent among market observers. The following risks warrant caution for new investors:

- The stock is currently trading at a P/E ratio of approximately 37.9x, which sits well above historical norms for the specialty retail sector.

- UBS analyst Mark Carden maintains a Neutral rating, suggesting that much of the near-term upside may already be priced into the shares at current levels.

- The dividend yield remains modest at 0.33%, which may not satisfy income-focused investors looking for higher cash flow returns.

- Execution risk remains high as the company attempts to integrate 120 new units while maintaining its current service standards.

Fintwit's AI verdict

The quantitative models are processing the recent volatility and the gap-up price action to determine if the current trend has legs. While the valuation is stretched, the fundamental momentum and the upcoming strategic roadmap provide a unique backdrop for the stock's next phase.

Investors are currently weighing the impact of the upcoming fiscal year targets against the reality of a high-multiple environment. The following assessment synthesizes the current market sentiment and technical setup.