NVIDIA Corporation (NVDA): The AI Infrastructure Powerhouse

NVIDIA (NVDA) remains the foundational architect of global AI. We break down the financials, competitive moat, and the latest analyst sentiment.

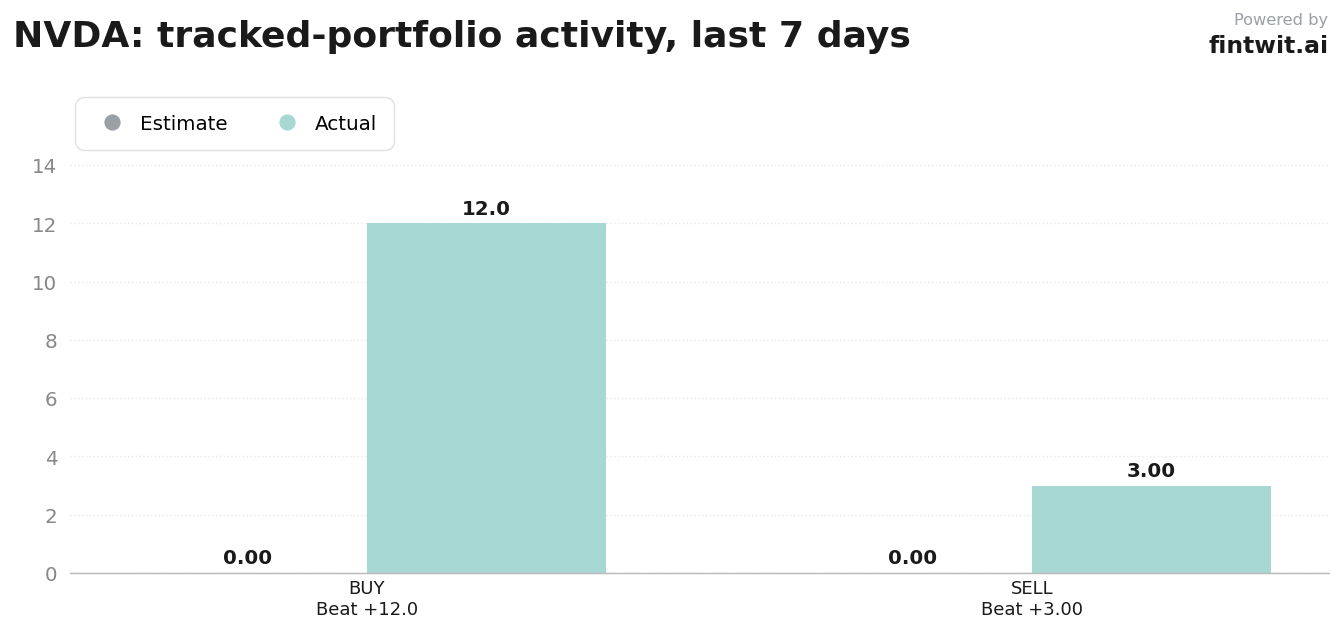

Why it's trending

NVIDIA is currently the focal point of institutional capital flows, evidenced by a high volume of recent trading activity. Over the last seven days, the stock saw 12 buy orders compared to only 3 sell orders among tracked institutional holders.

The company's transition from a gaming-centric GPU provider to the architect of AI factories continues to drive market interest. Investors are closely monitoring the sustainability of hyperscaler capital expenditure, which remains the primary engine for the firm's revenue growth.

- Current price: $215.33

- 180-day performance: +20.38%

- Institutional holders tracked: 14

- 7-day buy/sell ratio: 4:1

The business in numbers

NVIDIA's financial performance is defined by its dominance in the Data Center segment, which now accounts for the vast majority of total revenue. The company's ability to maintain high margins while scaling production is a direct result of its full-stack hardware and software integration.

Capital allocation remains aggressive, with the company prioritizing both R&D and shareholder returns. Management recently authorized an $80 billion share repurchase program to signal confidence in long-term cash flow generation.

- Data Center revenue share: 89.7%

- Data Center YoY revenue growth: 92% (Q1 FY2027)

- Gaming revenue share: 7.4%

- Professional Visualization & Automotive share: 2.9%

- FY2026 Free Cash Flow: $96.7 billion

- Forward P/E ratio: 30.5x

Bull vs bear

The bull case centers on the massive total addressable market for AI infrastructure and the entrenched nature of the CUDA software ecosystem. Analysts argue that the company's rapid architectural innovation cycle, including Blackwell and Rubin, creates a durable moat.

The bear case highlights risks related to supply chain concentration and the potential for hyperscalers to shift toward custom silicon. Skeptics also point to the cyclical nature of the semiconductor industry and the possibility of an AI spending air pocket.

- Bull: Vivek Arya (Bank of America) targets $320, citing a $1.7 trillion AI data center TAM by 2030.

- Bull: Harlan Sur (JPMorgan) maintains Overweight with a $280 target, citing 70% hyperscaler capex growth.

- Bull: Todd Campbell (TheStreet) targets $235, emphasizing the strategic importance of networking.

- Bear: Jay Goldberg (Seaport Research) targets $140, citing margin pressure from cloud compute rebates.

- Bear: Simply Wall St model suggests a $185.60 fair value, implying 20.4% overvaluation.

- Bear: 24/7 Wall St (Baker) targets $192.60, warning of a potential CoWoS packaging overbuild.

Fintwit's AI verdict

The consensus among quantitative models and market analysts remains heavily skewed toward the company's long-term growth trajectory. While valuation concerns persist, the fundamental strength of the Data Center segment continues to outweigh short-term cyclical risks.

The integration of networking equipment and software suites provides a recurring revenue layer that traditional hardware companies lack. Investors are currently weighing the impact of export controls against the sheer scale of global AI adoption.