Micron Technology Inc (MU): The AI Memory Infrastructure Play

Micron Technology (MU) is a critical AI infrastructure partner. We break down its valuation, growth drivers, and the risks of the current memory cycle.

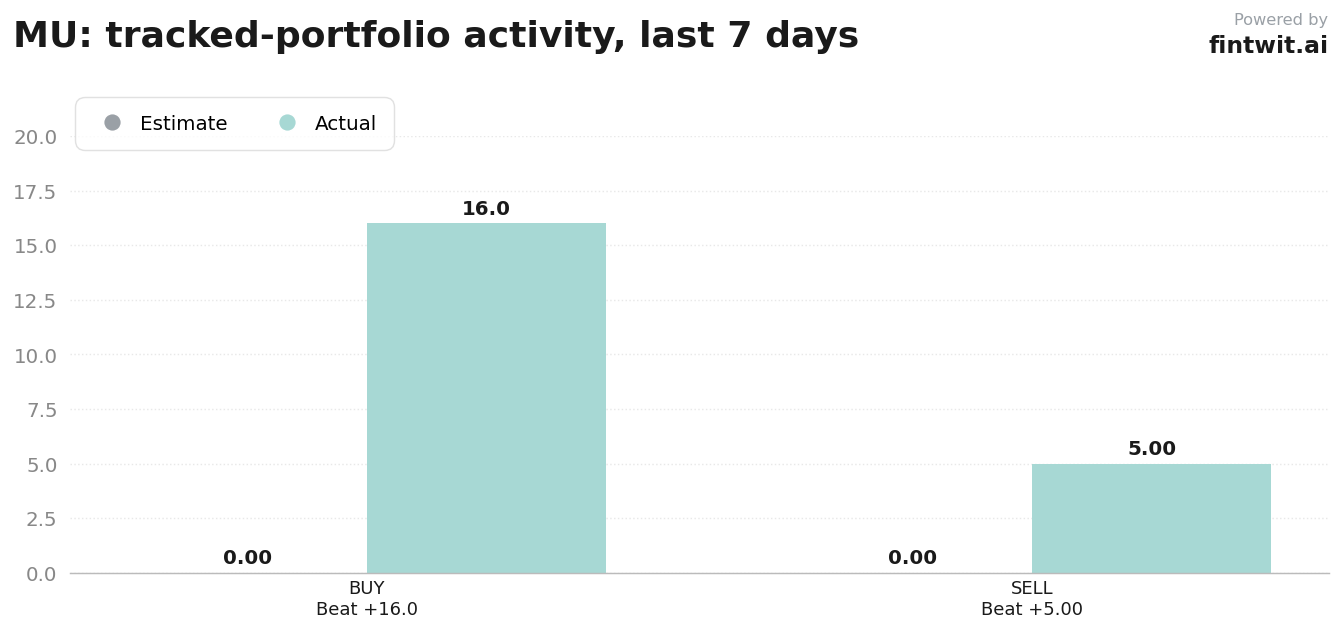

Why it's trending

Micron is currently seeing intense institutional interest, with 16 buy orders recorded against only 5 sells over the last seven days. This activity follows the company's strategic pivot toward high-bandwidth memory (HBM) and long-term supply agreements with hyperscalers.

The market is attempting to determine if Micron's current earnings trajectory is a permanent structural upgrade or a temporary cyclical peak. Sentiment remains divided between those betting on sustained AI demand and those fearing a 2028-2029 supply glut.

- 16 buy orders vs 5 sell orders in the last 7 days

- 310.61% price appreciation over the last 180 days

- 20 institutional holders currently tracked in recent activity

The business in numbers

Micron's financial profile has been transformed by its transition into high-value memory segments. The company is prioritizing aggressive capital expenditure to maintain its technological lead in 1-gamma DRAM and G9 NAND.

Valuation metrics suggest a disconnect between current earnings power and market expectations. While the broader IT sector trades at a 21x forward P/E, Micron remains priced at approximately 10x.

- Forward P/E ratio: 10x

- IT sector average P/E: 21x

- Semiconductor ETF average P/E: 28x

- FY26 projected capital expenditure: $20B-$25B

- Primary growth driver: Compute and Networking (CNBU) segment

Bull vs bear

The bull case centers on the scarcity of HBM production capacity and the stability provided by long-term fixed-price contracts. Analysts argue that the current valuation fails to account for the backlog of orders and the technological moat surrounding advanced memory nodes.

The bear case emphasizes the historical volatility of the memory market and the risk of oversupply as competitors like Samsung and SK Hynix expand capacity. Skeptics argue that the current cycle is nearing its limit and that capital intensity will eventually erode free cash flow.

- Bull: Timothy Arcuri (UBS) targets $1,625, citing improved pricing visibility.

- Bull: Kevin Cassidy (Rosenblatt) targets $500, highlighting DRAM/NAND price trends.

- Bear: Michele Manganelli (Seeking Alpha) targets $700, warning of 2028-2029 oversupply.

- Bear: EcoMoat AI targets $650, citing high capex requirements and tapering FCF growth.

- Bear: Kevin Hincks (Schwab Network) describes current price target increases as speculative hyperbole.

Fintwit's AI verdict

The quantitative consensus on the platform remains heavily skewed toward the potential for further upside, despite the vocal minority warning of cyclical exhaustion. The model processes the current valuation gap relative to the broader semiconductor index as a primary indicator of mispricing.

The following assessment synthesizes the current order flow, analyst sentiment, and fundamental valuation metrics to provide a final outlook on the ticker.