MercadoLibre Inc. (MELI): A Deep Dive Into Latin America's Digital Engine

MercadoLibre's integrated commerce and fintech ecosystem is growing at 49% YoY, but margin compression remains a key concern for investors.

Why it's trending

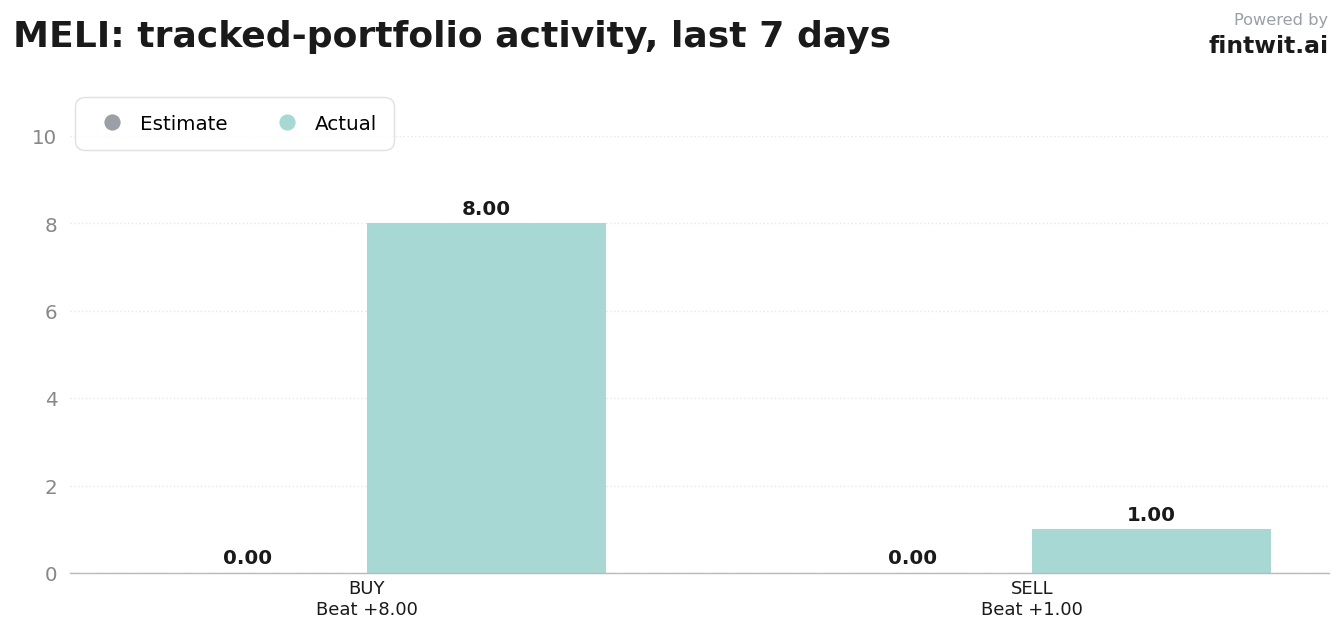

The stock has faced significant selling pressure recently, down 24.50% over the last 180 days. Despite this, institutional and retail sentiment remains active, with 8 buys recorded against only 1 sell in the last 7 days.

Investors are currently reconciling the company's massive revenue expansion with the margin compression resulting from its 'wartime' capital allocation strategy. The market is closely watching whether the $14.6 billion credit portfolio can scale without further deteriorating asset quality.

- Recent 7-day activity: 8 buys vs 1 sell.

- 180-day price performance: -24.50%.

- Current market capitalization: $82.93 billion.

The business in numbers

MercadoLibre operates a dual-pillar model where high-frequency fintech interactions drive commerce engagement. The company's logistics infrastructure, Mercado Envios, acts as a primary barrier to entry against regional competitors.

Financial results from Q1 2026 highlight the scale of this operation. Revenue grew 49% year-over-year, though operating margins compressed to 6.9% due to heavy investment in the credit and logistics segments.

- Commerce segment revenue growth: 47% YoY.

- Fintech (Mercado Pago) revenue growth: 51% YoY.

- Credit portfolio size: $14.6 billion, up 87% YoY.

- Non-performing loans (NPLs): 8.0%.

- Forward P/E ratio: ~38.9x.

- EV/FCF multiple: 6.1x.

Bull vs bear

The bull case centers on the massive untapped potential of the Latin American digital market. Analysts point to the low penetration of online shopping as a structural tailwind for long-term growth.

Conversely, the bear case focuses on the sustainability of the current investment cycle. Critics argue that the high P/E ratio and margin dilution pose significant risks to near-term earnings stability.

- Bull: Trey Thoelcke (24/7 Wall St.) targets $2,177, citing low online purchase frequency in LatAm.

- Bull: Jefferies identifies the current valuation as a rare entry point with a $2,600 target.

- Bull: Morgan Stanley maintains a Buy rating, citing dominance in digital transformation.

- Bear: Zacks Research downgraded to a strong sell, citing concerns over margin sustainability.

- Bear: J.P. Morgan downgraded to Neutral, citing caution over margin-dilutive investments.

- Bear: MarketBeat consensus notes a $1,750 target, highlighting valuation risks relative to earnings.

Fintwit's AI verdict

The current market environment presents a classic growth-versus-value dilemma for MercadoLibre. While the margin compression is a legitimate headwind, the underlying growth metrics in the fintech and commerce segments remain significantly ahead of regional peers.

Investors should weigh the long-term structural runway against the immediate volatility of the credit book. The following assessment reflects the current consensus on the stock's potential for recovery.