Marvell Technology Group Ltd (MRVL): The Deep Dive

Marvell Technology Group Ltd (MRVL) shares dropped 16.74% to $263.47. We examine the firm's AI-driven connectivity strategy and market sentiment.

Why it's trending

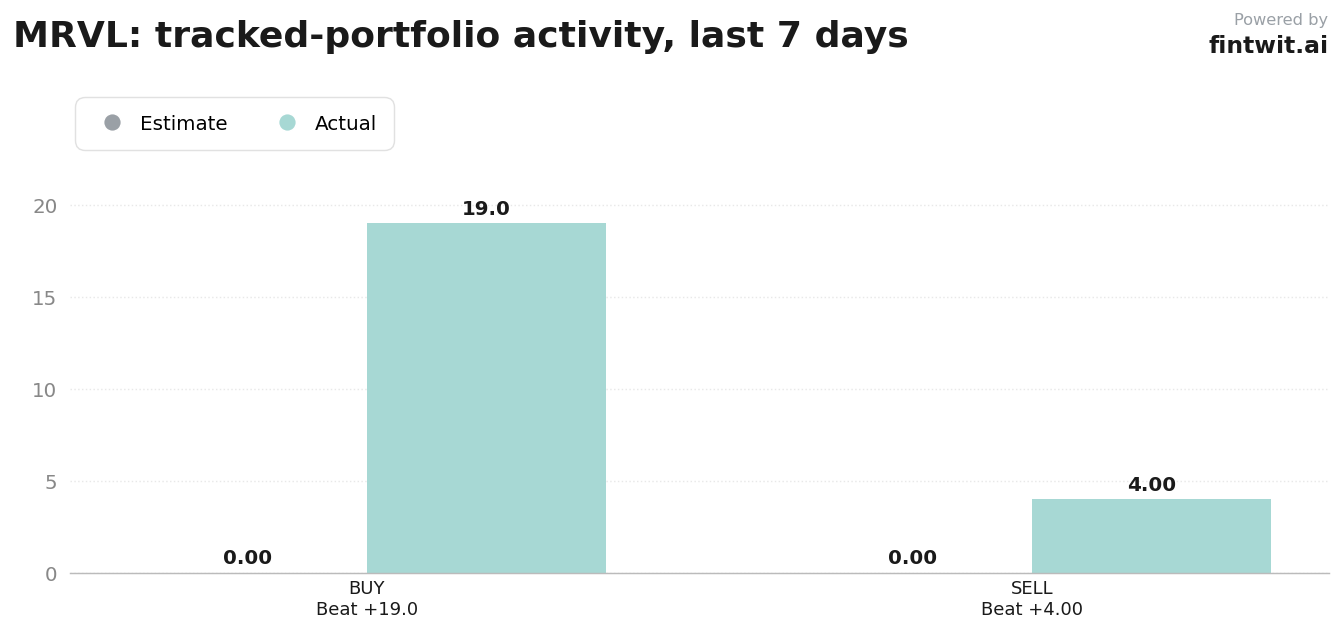

The recent price action reflects a broader rotation out of high-beta semiconductor names following extended rallies. Institutional interest remains high, as evidenced by the 19 buys versus 4 sells recorded among tracked holders over the last seven days.

Market participants are closely monitoring the firm's ability to maintain its AI-adjacent connectivity lead. The current volatility provides a test of the support levels established during the stock's 166% run over the past six months.

- 19 buy orders executed by institutional holders in the last 7 days.

- 4 sell orders executed by institutional holders in the last 7 days.

- 16.74% single-day price decline marks a significant correction from recent highs.

- 166.37% price appreciation over the trailing 180-day period.

The business in numbers

Marvell operates with a diversified revenue base, though its enterprise and carrier segments remain the primary anchors for cash flow. The company's strategic pivot toward high-speed Ethernet and AI-adjacent infrastructure is designed to capture higher margins in a competitive landscape.

- $76.86 billion current market capitalization.

- 26% revenue share attributed to Enterprise Networking, Carrier, and Automotive segments.

- Stable to moderate growth trajectory in core networking segments.

- Strategic focus shifting toward high-speed Ethernet for AI data centers.

Bull vs bear

The bull case centers on the company's indispensable role in the AI data center architecture, where high-speed connectivity is a bottleneck for compute performance. Bears point to the valuation premium and the cyclical nature of the carrier and enterprise networking markets.

Bull arguments: Marvell's custom ASIC business is gaining traction with hyperscalers; the company holds a dominant position in optical interconnects; AI infrastructure spending is expected to remain elevated through 2025.

Bear arguments: High valuation multiples relative to historical averages; potential for inventory corrections in the carrier segment; intense competition from specialized networking chip providers.

Fintwit's AI verdict

Sentiment analysis across financial social media platforms indicates a persistent optimism regarding the firm's long-term positioning in the semiconductor supply chain. Traders are viewing the recent 16.74% drawdown as a potential entry point rather than a fundamental shift in the company's growth narrative.

The consensus among active market participants emphasizes the durability of the AI-driven demand cycle despite short-term price volatility.