Lennar Corporation (LEN) Q2 Earnings Preview: What to Watch

Lennar Corporation (LEN) faces a difficult Q2 2026 earnings report as mortgage rates and affordability concerns weigh on the homebuilder's margins.

The setup

Wall Street sentiment has shifted toward caution as Lennar navigates a volatile residential construction environment. Analysts are closely monitoring how the company balances its production-first strategy against the reality of high interest rates.

The firm is currently transitioning toward an asset-light model to mitigate balance sheet risk. Investors remain skeptical about whether this pivot can effectively offset the current headwinds in the housing market.

- Keefe, Bruyette & Woods downgraded Lennar to Underperform with an $86 price target.

- BTIG maintains a Sell rating and a $73 price target, citing elevated completed inventory.

- Independent analyst Dilantha De Silva remains bullish, suggesting Q1 may have been the trough for margin compression.

Consensus numbers

Expectations for the second quarter reflect a challenging environment for residential developers. Revenue and earnings estimates have been revised downward as the market accounts for reduced buyer demand.

The company's ability to maintain profitability in its homebuilding and financial services segments will be the primary metric for institutional investors.

- EPS estimate: $1.23.

- Revenue estimate: $8.01 billion.

- Guidance: 20,000 to 21,000 home deliveries expected for Q2.

- Beat/Miss probability: 30% beat, 50% miss, 20% inline.

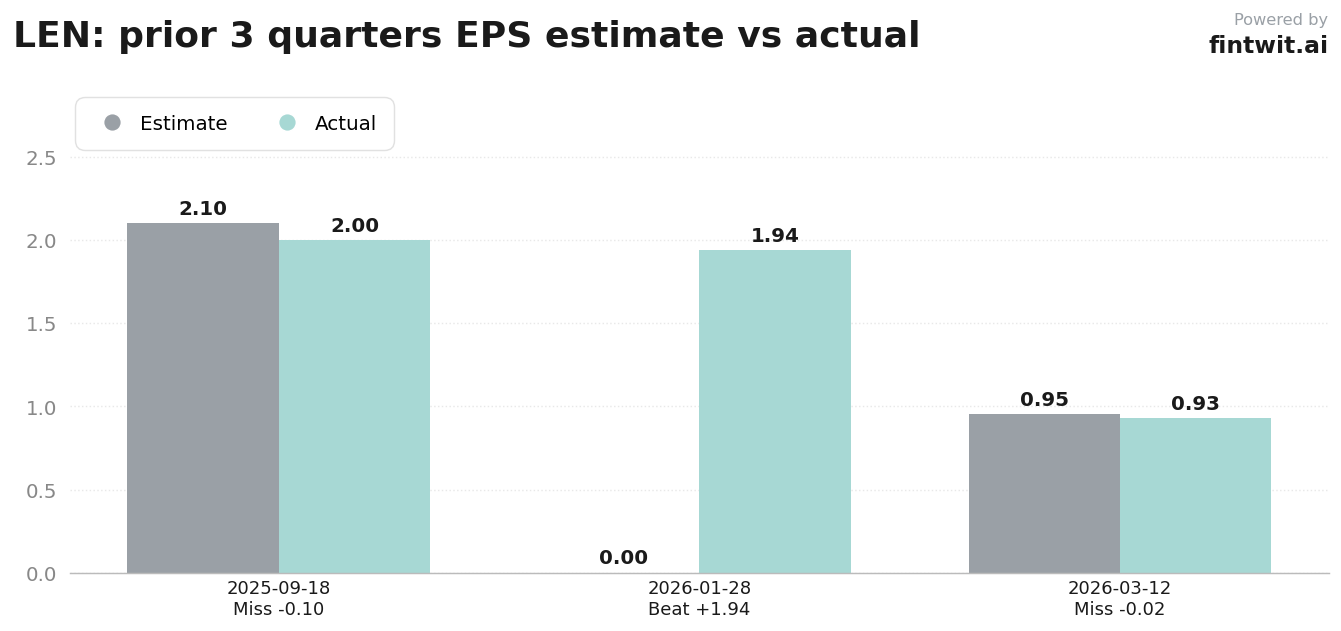

- Q1 2026 actual EPS: $0.93 vs $0.953 estimate.

What we'll watch on the call

Management's commentary on sales incentives will be critical to understanding the true state of demand. Investors need to know if these incentives are eating into gross margins at an unsustainable rate.

The financial services segment's performance will also be under the microscope. Maintaining mortgage origination volumes in a high-rate environment is a key indicator of the company's competitive positioning.

- Current level of sales incentives utilized to sustain volume.

- Impact of elevated mortgage rates on new order trends and cancellation rates.

- Gross margin outlook given current land and labor cost pressures.

- Effect of the asset-light transition on free cash flow and balance sheet flexibility.

Fintwit's AI verdict

The algorithmic analysis of Lennar's current market position suggests a high probability of continued downward pressure on valuation multiples. While the company's operational shifts are strategic, the macro environment remains a significant headwind that may not be fully priced into current consensus estimates.

Investors should weigh the potential for a negative surprise against the company's historical ability to manage inventory. The technical and fundamental indicators currently point toward a cautious stance for the upcoming quarter.