Is Kinross Gold Corporation (KGC) Undervalued? A Valuation Verdict

Kinross Gold (KGC) appears undervalued based on P/E ratios and free cash flow, but rising costs present a challenge. Explore the investment case.

The headline number

Kinross Gold Corporation (KGC) reported record attributable free cash flow of $837.5 million in Q1 2026, more than doubling from $381 million in Q1 2025.

The company maintains a robust balance sheet with $1.4 billion in net cash as of Q1 2026 and total liquidity of $3.9 billion.

KGC is on track to meet its 2026 guidance for production (2.0 million gold equivalent ounces), cost of sales ($1,360 per ounce), and all-in sustaining costs ($1,730 per ounce).

- Q1 2026 Production Cost of Sales: $1,397 per ounce (up 34% YoY)

- 2026 Capital Expenditure Guidance: $1,500 million

- Potential impact of $10/barrel oil price increase: $10/ounce cost increase

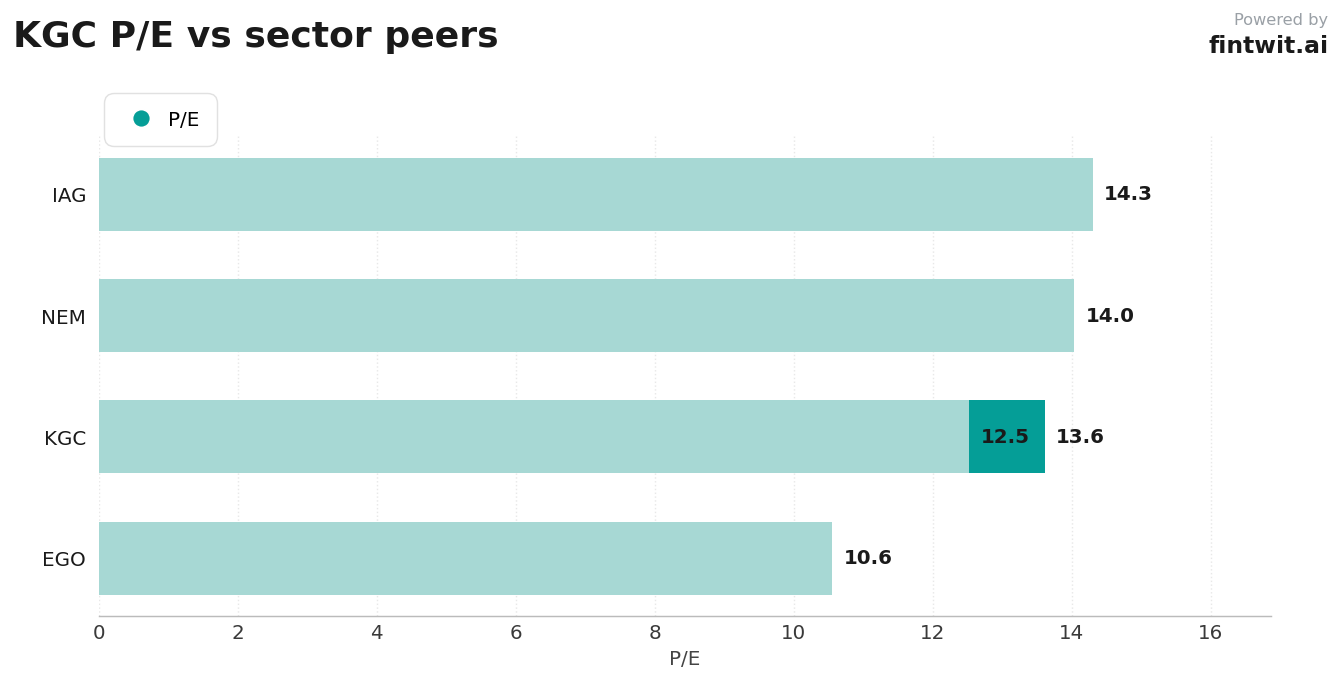

Peer comparison

Kinross Gold (KGC) trades at a P/E ratio of 12.52, positioning it favorably against some industry peers.

The company's P/E ratio is below the Basic Materials sector average of 24.19.

This valuation suggests potential upside if operational efficiencies and cash flow generation continue.

- Eldorado Gold Corp. (EGO): P/E ratio of 10.55

- Kinross Gold Corp. (KGC): P/E ratio of 12.52

- Newmont Corp. (NEM): P/E ratio of 14.03

- Iamgold Corp. (IAG): P/E ratio of 14.30

Bull vs bear

The bull case for Kinross Gold (KGC) centers on its strong free cash flow generation, robust balance sheet, and disciplined capital allocation, including returning 40% of free cash flow to shareholders in 2026 via buybacks and dividends.

Growth projects like Great Bear and Lobo-Marte are expected to bolster future production, supporting analyst 'Buy' ratings and price targets indicating significant upside.

However, the bear case highlights increasing production costs, with cost of sales per ounce rising 34% year-over-year to $1,397 in Q1 2026, and projected all-in sustaining costs of $1,730 per ounce for 2026.

- Bull Case: Undervalued P/E, record free cash flow, strong liquidity, growth projects.

- Bull Case: 40% free cash flow return to shareholders in 2026.

- Bull Case: Analyst consensus 'Buy' rating.

- Bear Case: Rising operating costs and input inflation.

- Bear Case: Significant 2026 capital expenditure guidance of $1,500 million.

- Bear Case: Potential overvaluation based on GF Value™ estimate ($16.46 vs. current price).

Fintwit's AI verdict

Analysis suggests Kinross Gold (KGC) presents a compelling investment profile, underpinned by substantial free cash flow generation and a solid financial position.

While cost pressures are a noted concern, the company's strategic growth initiatives and shareholder return policies are viewed favorably by many analysts.