Kinross Gold (KGC) Stock: Undervalued Miner with Strong Cash Flow

Kinross Gold (KGC) appears undervalued based on P/E, cash flow, and analyst sentiment. Discover if this miner is a buy.

The headline number

Kinross Gold Corporation (KGC) is currently trading at a Price-to-Earnings (P/E) ratio of 12.52. This valuation metric is notably lower than the broader gold industry average of 22.1x and the average P/E of its direct peers, which stands at 26.4x.

This significant discount suggests that KGC may be undervalued relative to its competitors and the overall market. The company's financial performance and future prospects appear to be priced at a lower multiple than comparable entities in the gold mining sector.

- KGC P/E Ratio: 12.52

- Gold Industry Average P/E: 22.1

- Peer Group Average P/E: 26.4

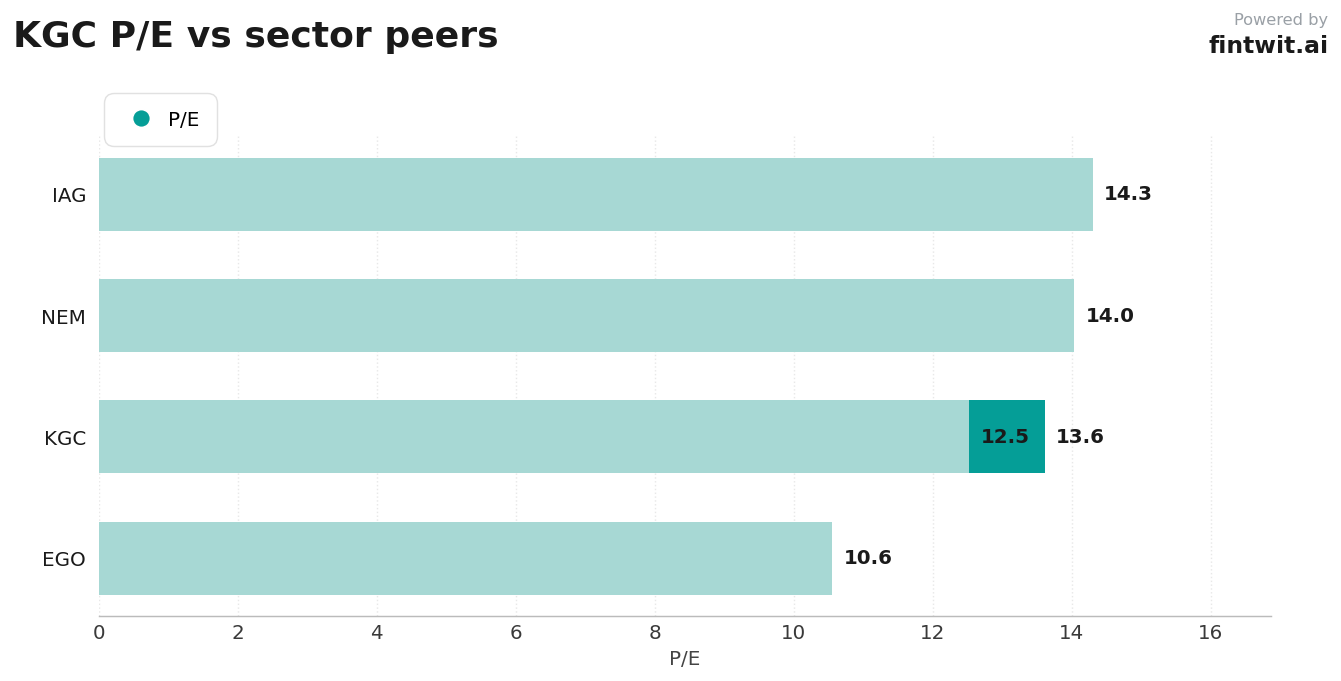

Peer comparison

Kinross Gold (KGC) presents a compelling valuation case when compared to its industry peers. Its P/E ratio of 12.52 is substantially lower than several key competitors, indicating potential for upside.

While Eldorado Gold (EGO) trades at a lower P/E of 10.55, Kinross's P/E is significantly below Newmont Corp. (NEM) at 14.03 and Iamgold Corp. (IAG) at 14.3.

This disparity in valuation multiples, particularly against larger players like Newmont, suggests that the market may not be fully appreciating Kinross's current assets and future growth potential.

- Kinross Gold (KGC) P/E: 12.52

- Eldorado Gold (EGO) P/E: 10.55

- Newmont Corp. (NEM) P/E: 14.03

- Iamgold Corp. (IAG) P/E: 14.3

Bull vs bear

The bull case for Kinross Gold (KGC) centers on its attractive valuation, strong free cash flow generation, and a robust project pipeline. Analysts have set an average price target of $44.02, implying a 52.79% upside from current levels, with multiple 'Buy' and 'Strong Buy' ratings.

The company reported $838 million in free cash flow for Q1 2026 and maintains a healthy balance sheet with $1.4 billion in net cash. Future growth is expected from projects like Great Bear and Lobo-Marte, with stable production guidance of 2.0 million gold equivalent ounces annually through 2028.

Conversely, the bear case highlights concerns about KGC's modest projected earnings growth of 0.3% annually, which lags the broader market. Significant capital expenditures of $1,500 million are planned for 2026-2028, which could temporarily impact free cash flow. Rising operating costs, particularly for production cost of sales per ounce, and a heavy reliance on sustained high gold prices are also key risks. Sensitivity analysis indicates that a $10 per barrel change in oil prices could impact costs by $10 per ounce.

- Bull: P/E of 12.52 significantly below industry and peer averages.

- Bull: Analyst consensus price target of $44.02 suggests 52.79% upside.

- Bull: Strong Q1 2026 free cash flow of $838 million and $1.4 billion net cash.

- Bull: Growth pipeline includes Great Bear and Lobo-Marte projects.

- Bull: Stable production guidance of 2.0 million gold equivalent ounces annually through 2028.

- Bear: Projected annual earnings growth of only 0.3%.

- Bear: High capital expenditures of $1,500 million per year from 2026-2028.

- Bear: Rising operating costs and sensitivity to gold price fluctuations.

- Bear: Potential impact of oil price volatility on operating costs.

Fintwit's AI verdict

Analysis of Kinross Gold Corporation (KGC) suggests a compelling investment case driven by its current valuation metrics and operational strengths. The company's P/E ratio stands out as particularly attractive when benchmarked against both the broader gold industry and its direct competitors.

Furthermore, Kinross's demonstrated ability to generate substantial free cash flow, coupled with a solid balance sheet and a clear pipeline of growth projects, underpins its financial resilience and future potential. Analyst sentiment generally aligns with this positive outlook, with price targets indicating significant upside.