Children's Place Inc (PLCE) Q1 2026 Earnings Preview: What to Watch

Children's Place (PLCE) faces a critical Q1 2026 earnings report on June 12. We analyze the margin-recovery plan and persistent macroeconomic headwinds.

The setup

The Children's Place enters its Q1 2026 earnings report under significant pressure, with analysts maintaining a Hold consensus as the company struggles with a turnaround strategy. Persistent macroeconomic headwinds continue to weigh on the firm's ability to stabilize revenue and manage liquidity.

Management has previously flagged execution issues and marketing inefficiencies in its digital channels. Investors are now looking for signs of stabilization or recovery in these segments as the company attempts to navigate a competitive, mall-centric environment.

- Management is prioritizing operational discipline and inventory management to preserve liquidity.

- The company has expressed cautious optimism for sequential improvement later in the year.

- Success remains contingent on stabilizing consumer demand and the execution of a margin-recovery plan.

Consensus numbers

Market expectations for the upcoming quarter reflect a cautious outlook, with analysts anticipating continued bottom-line pressure. The company has a history of consecutive earnings misses that have contributed to the current negative sentiment.

The following data points summarize the consensus expectations and recent performance history.

- Q1 2026 EPS Estimate: -$2.146

- Q1 2026 Revenue Estimate: $198.32 million

- Beat Probability: 15%

- Miss Probability: 70%

- Inline Probability: 15%

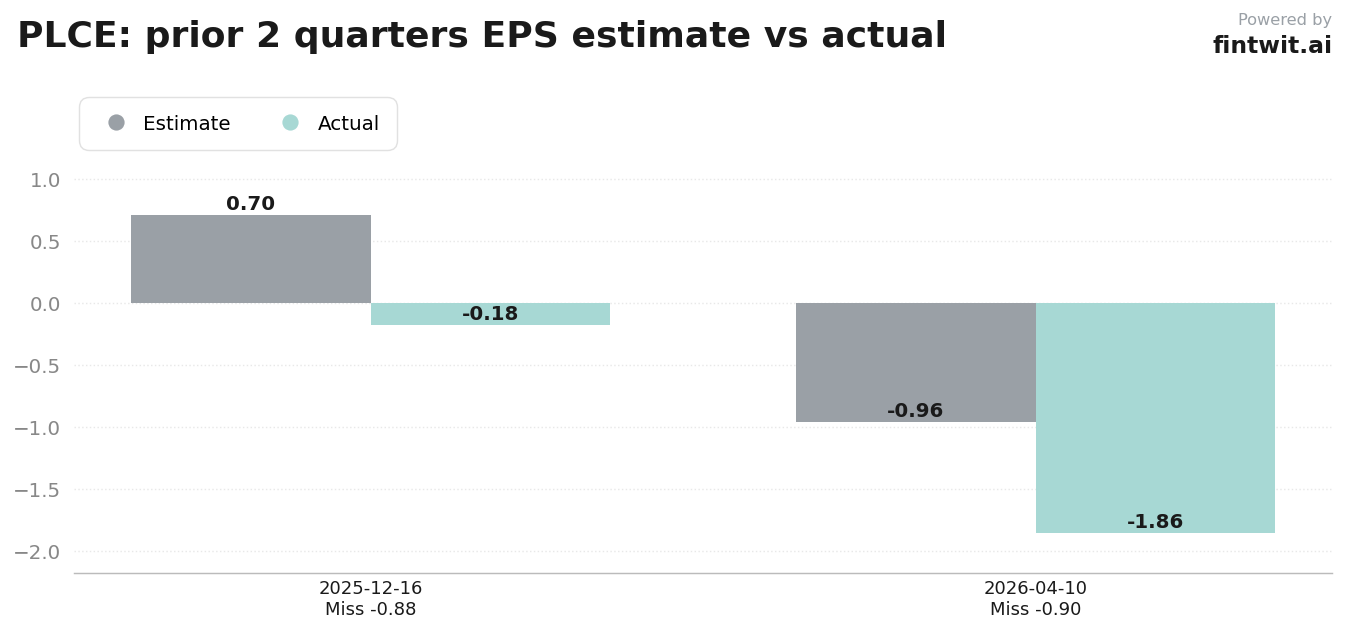

- Q4 2025 EPS: -$0.18 vs $0.703 estimate

- Q4 2025 Revenue: $339.47 million vs $366.60 million estimate

- Q1 2026 (Prior) EPS: -$1.86 vs -$0.963 estimate

- Q1 2026 (Prior) Revenue: $329.23 million vs $358.27 million estimate

What we'll watch on the call

Analysts are focused on whether the company can successfully execute its margin-recovery plan to offset current profitability headwinds. The impact of inflationary pressures on middle-income families remains a primary concern for forward guidance.

The following items represent the key areas of focus for the upcoming earnings call.

- Status of the margin-recovery plan and its specific impact on profitability.

- Impact of recent tariff pressures and inflationary trends on middle-income consumer demand.

- Progress in resolving marketing inefficiencies and e-commerce execution issues.

- Updates on the store footprint optimization strategy in a competitive retail environment.

- UBS analyst Jay Sole maintains a Neutral rating with a $3.50 price target.

- General consensus maintains a Hold rating with a $4.00 price target.

Fintwit's AI verdict

The quantitative models analyzing the company's recent performance history and current market positioning suggest a challenging path forward. The combination of persistent earnings misses and the broader macroeconomic environment creates a difficult hurdle for the stock to clear in the near term.

Investors are weighing the potential for a successful turnaround against the reality of compressed margins and ongoing competitive threats. The upcoming report will provide the necessary data to determine if the current strategy is gaining any traction.