The Cheapest Large Caps Right Now: A P/E Screen

A deep dive into ten large-cap stocks with low P/E ratios to determine if they are genuine bargains or structural value traps.

How we screened

We filtered for large-cap equities with market capitalizations exceeding $10 billion that currently trade at single-digit price-to-earnings multiples. This screen prioritizes companies where the market has assigned a significant discount relative to historical averages.

The objective is to distinguish between 'unearned' discounts—where market sentiment has overcorrected—and 'earned' discounts, where structural headwinds justify a lower valuation. We evaluated each ticker based on free cash flow yield, debt levels, and industry-specific risks.

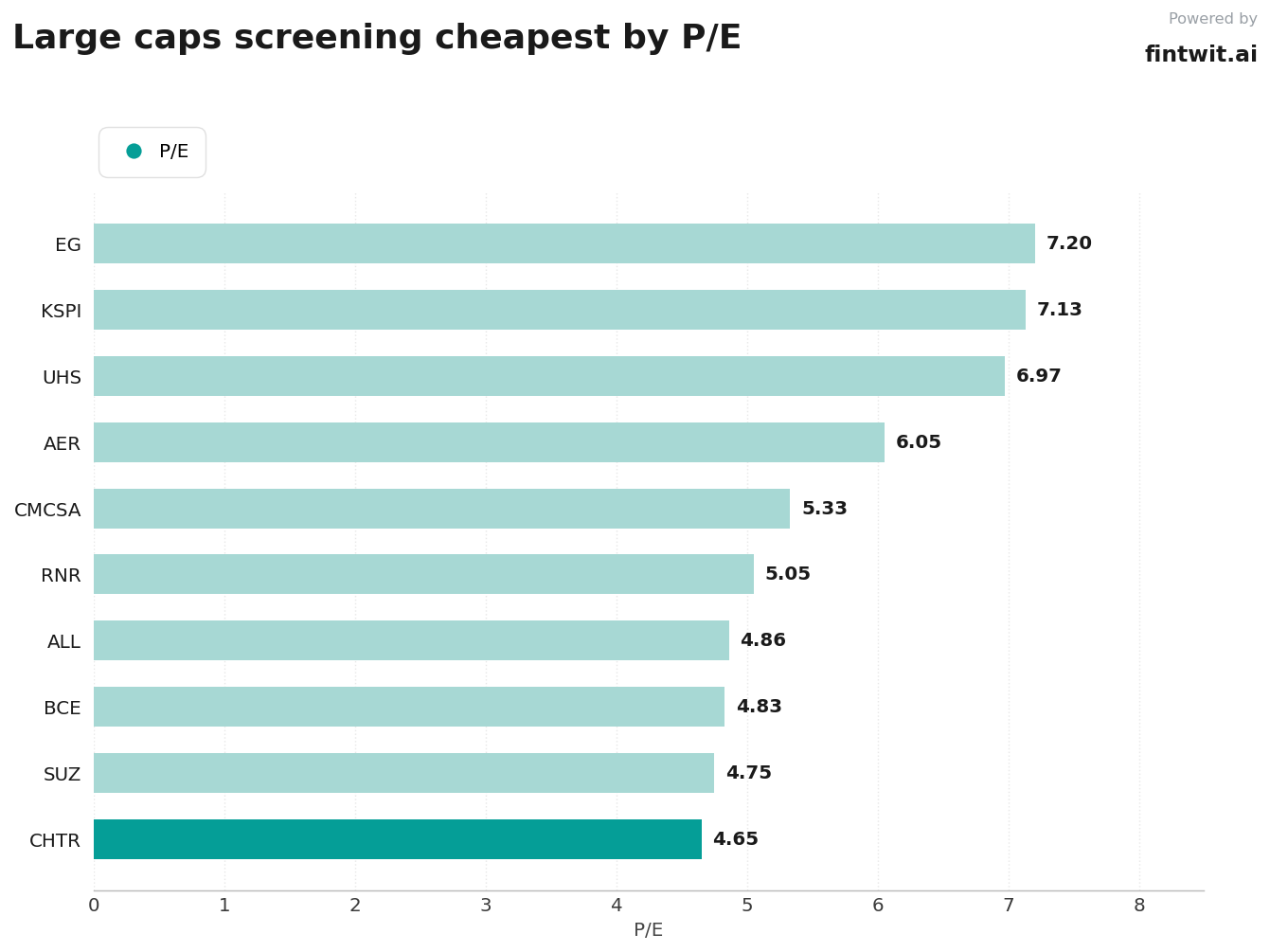

The list

The following tickers represent some of the lowest P/E valuations currently available in the large-cap space. Each entry includes the current P/E ratio and the primary rationale for the current market pricing.

- CHTR (4.65 P/E): Market fears of permanent broadband subscriber decline; analyst view: broadband remains a resilient utility.

- SUZ (4.75 P/E): Cyclical pressure on pulp prices; analyst view: valuation reflects stress, though downside is limited by cost position.

- BCE (4.83 P/E): Heightened competition and dividend cut concerns; analyst view: growth is pressured by market saturation and debt.

- ALL (4.86 P/E): Revenue headwinds and catastrophe loss volatility; analyst view: turnaround story remains underpriced at 5x earnings.

- RNR (5.05 P/E): Concerns over soft reinsurance pricing; analyst view: strong underwriting performance and diversification reduce volatility.

- CMCSA (5.33 P/E): Subscriber losses in cable and media flux; analyst view: structural headwinds like cord-cutting are real.

- AER (6.05 P/E): Skepticism regarding aircraft lessor cyclicality; analyst view: strong fundamentals and supply shortages support returns.

- UHS (6.97 P/E): Reimbursement risk and labor volatility; analyst view: hospital operators structurally trade at discounts.

- KSPI (7.13 P/E): Regulatory and macroeconomic risks in Kazakhstan; analyst view: market ignores strong domestic growth.

- EG (7.20 P/E): Earnings volatility due to hurricane season; analyst view: reinsurance earnings are inherently volatile.

Caveats

Low P/E ratios are often a reflection of underlying business deterioration rather than a mispricing by the market. Investors must distinguish between temporary cyclical troughs and permanent structural decline.

The following risks are inherent to the companies listed above:

- Debt-to-equity ratios for telecom and utility-adjacent firms like BCE and CHTR remain elevated in a higher-for-longer interest rate environment.

- Reinsurance firms like EG and RNR face unpredictable catastrophe loss cycles that can wipe out annual earnings in a single quarter.

- Hospital operators like UHS face persistent labor cost inflation that continues to compress operating margins.

- Geopolitical risk premiums, as seen in KSPI, can remain compressed indefinitely regardless of fundamental performance.

How to use this screen

This list should serve as a starting point for fundamental analysis rather than a list of immediate buys. Investors should prioritize companies with high free cash flow yields, such as ALL at 21.61% or RNR at 33.35%, over those with negative or low cash conversion.

Focus on the 'earned' versus 'unearned' distinction. If the discount is earned through structural decline, the P/E will likely remain low for years. If the discount is unearned, the valuation gap may close as the company proves its resilience to the market.