The Cheapest Large Caps Right Now: A P/E Screen of 10 Value Stocks

A deep dive into 10 large-cap stocks with P/E ratios under 8, separating genuine value plays from fundamental traps.

How we screened

We filtered the market for large-cap equities with market capitalizations exceeding $10 billion and P/E ratios below 8.0. This screen prioritizes companies currently ignored or punished by the broader market.

The objective is to distinguish between stocks that are cheap due to temporary sentiment shifts and those that are cheap because their business models are in terminal decline. We categorize these as either earned or unearned discounts.

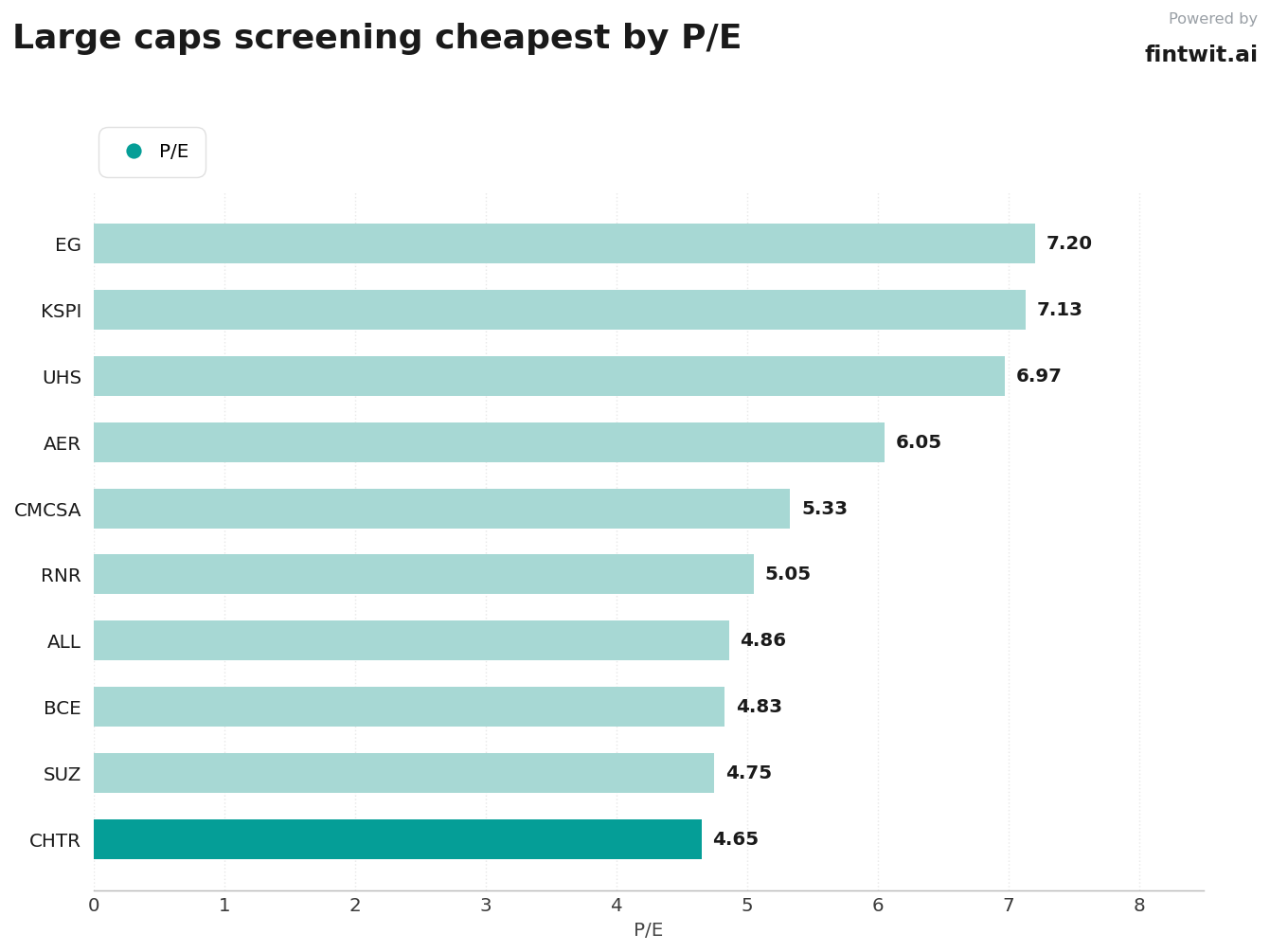

The list

The following list highlights 10 companies currently trading at low multiples, evaluated based on their fundamental health and market positioning.

- CHTR: P/E 4.65. Cheap due to broadband subscriber losses and debt. JPMorgan notes competitive intensity is challenging cable operators.

- SUZ: P/E 4.75. Cheap due to pulp price volatility. Seeking Alpha highlights a trend of lower profitability for producers.

- BCE: P/E 4.83. Cheap due to shrinking subscriber growth. The Motley Fool Canada notes the dividend is being cut and the valuation is not dirt-cheap.

- ALL: P/E 4.86. Cheap due to catastrophe-loss sensitivity. BofA analysts view the discount as unwarranted given 12% revenue growth.

- RNR: P/E 5.05. Cheap due to soft pricing concerns. Quartz notes the P/CF ratio is attractive compared to the industry average of 11.52.

- CMCSA: P/E 5.33. Cheap due to broadband losses and streaming competition. FAST Graphs notes pressure from inflation and declining TV viewership.

- AER: P/E 6.05. Cheap due to OEM delivery delays. Investing.com highlights the firm's financial flexibility as a key asset.

- UHS: P/E 6.97. Cheap due to skepticism regarding earnings durability. Stock Analysis 2026 points to margin recovery and behavioral health improvements.

- KSPI: P/E 7.13. Cheap due to regulatory and currency headwinds. Seeking Alpha notes the market is pricing it as a declining business despite domestic growth.

- EG: P/E 7.20. Cheap due to underperformance. Public.com notes consistent underperformance relative to the equal-weighted S&P 500.

Caveats

Low P/E ratios are often a signal of a value trap rather than a bargain. Investors must account for the following risks when analyzing these names.

- High debt loads can render a low P/E irrelevant if interest expenses erode free cash flow.

- Regulatory or political headwinds in specific regions, such as those affecting KSPI, can create permanent valuation discounts.

- Industry-wide cyclicality, particularly in insurance and paper products, can make trailing P/E ratios misleading indicators of future earnings power.

- Dividend yields, such as the 9.64% at BCE, may signal market anticipation of a future payout reduction.

How to use this screen

Use this data as a starting point for fundamental analysis rather than a buy list. A low P/E is a snapshot of the past, not a guarantee of future performance.

Focus on the free cash flow yield to verify if the earnings are backed by actual cash generation. For instance, ALL maintains a 21.61% FCF yield, which supports its current valuation thesis better than companies with negative or volatile cash flows.