Caseys General Stores Inc (CASY) Q4 Earnings Preview: What to Watch

Casey's General Stores (CASY) reports Q4 2026 earnings on June 9. Analysts expect $3.32 EPS. We analyze the pizza-forward strategy and Fikes/CEFCO integration.

The setup

Wall Street maintains a constructive outlook on Casey's as the company navigates a complex retail environment. Analysts are focused on whether the firm can maintain its high-margin prepared foods growth while managing the integration costs associated with recent store acquisitions.

Management's fiscal 2026 guidance remains the primary benchmark for investors. The company previously targeted inside same-store sales growth of 3.5% to 4.5% and inside margins between 41.5% and 42.5%.

- UBS maintains a Neutral rating with a price target raised to $805 from $706.

- Wells Fargo holds an Overweight rating and recently increased its price target to $910.

- Gordon Haskett maintains a Buy rating and lifted its price target to $850 from $800.

- Macro headwinds include fuel price volatility and inflationary pressures on operating expenses in rural markets.

Consensus numbers

The consensus estimate for fiscal Q4 2026 sits at $3.32 per share on revenue of $4.27 billion. Recent history shows a pattern of earnings surprises, with the company exceeding estimates in two of the last three quarters.

The following data points summarize the current market expectations and recent performance history.

- EPS estimate: $3.32.

- Revenue estimate: $4.27 billion.

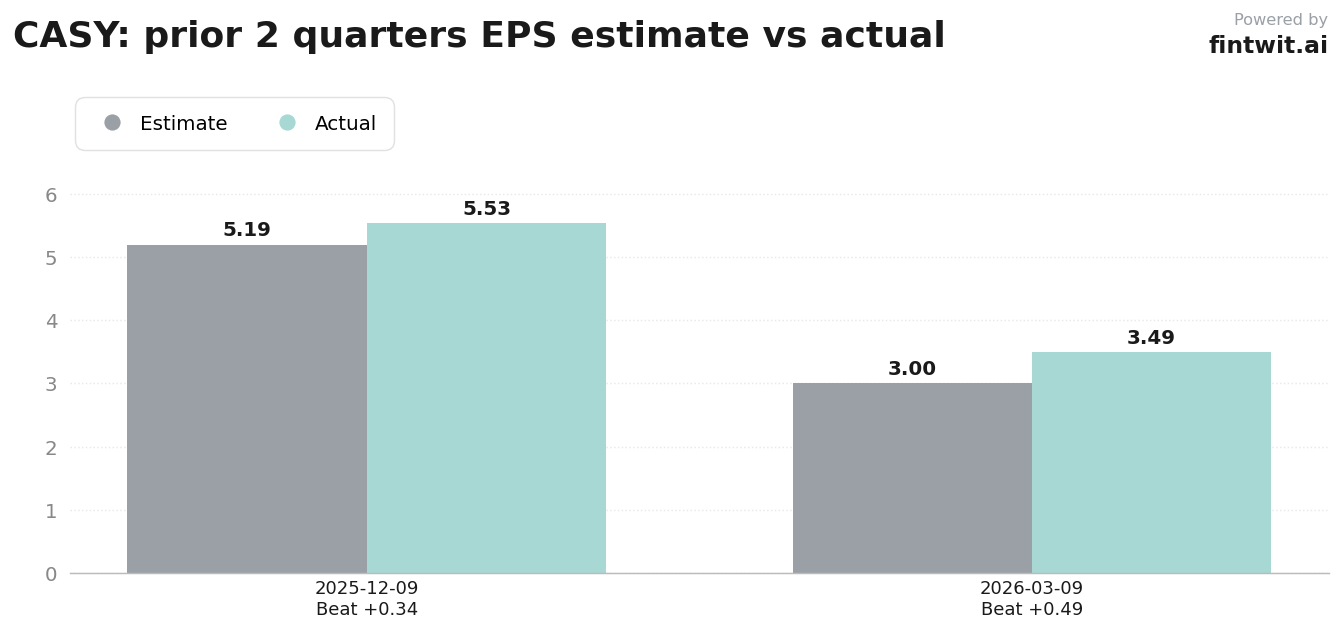

- Q3 2026 actual EPS: $3.49 versus $3.00 estimate.

- Q2 2026 actual EPS: $5.53 versus $5.19 estimate.

- Beat probability: 65%.

What we'll watch on the call

Investors are looking for granular detail on the integration of the Fikes/CEFCO acquisition. The market wants to know if these new units are diluting inside-store profitability or if they are tracking toward the company's internal margin targets.

The 'pizza-forward' strategy remains the primary engine for margin expansion. Analysts will scrutinize whether this segment can continue to grow volume despite potential consumer trade-down behavior in rural markets.

- Impact of acquisition-related costs on near-term inside margins.

- Consumer traffic trends comparing rural versus urban market segments.

- Sustainability of prepared food margins amid rising ingredient costs.

- Updated capital expenditure plans for the 80+ new stores targeted for fiscal 2027.

- Management commentary on fuel margin sensitivity to geopolitical tensions affecting oil prices.

Fintwit's AI verdict

The quantitative models suggest that the market may be underestimating the long-term margin benefits of the recent store expansion. While fuel volatility presents a near-term risk, the operational efficiency of the core food business provides a significant buffer against broader retail weakness.

Investors should monitor how the company balances aggressive store growth with debt management in the upcoming fiscal year. The current setup indicates a favorable risk-reward profile for those betting on continued operational execution.