AutoZone Inc (AZO) Q3 Earnings Preview: What to Watch

AutoZone reports Q3 2026 earnings on May 26. We break down the consensus estimates, key segment growth, and the impact of LIFO charges on margins.

The setup

AutoZone is navigating a complex environment defined by a repair-not-replace mentality among consumers. High new-vehicle prices and elevated interest rates continue to drive demand for older vehicle maintenance.

Management is currently executing an aggressive expansion strategy, targeting 90-95 new global store openings in the third quarter alone. This brings the full-year guidance to a range of 350-360 new locations.

Despite this growth, the company must contend with structural cost increases. Elevated SG&A investments and ongoing tariff-related pressures remain primary concerns for institutional investors.

- Management expects mid-single-digit same-SKU inflation through the remainder of the fiscal year.

- Ticket growth is projected to reach its peak during the fourth quarter.

- LIFO accounting charges are expected to remain a consistent headwind at approximately $60 million per quarter.

Consensus numbers

Wall Street remains cautiously optimistic, though analysts are closely monitoring the impact of margin-muddying LIFO charges on bottom-line performance. The consensus reflects a steady, if tempered, growth trajectory.

The following figures represent the current market expectations for the upcoming fiscal third quarter results.

- EPS Estimate: $36.21

- Revenue Estimate: $4.86 billion

- Commercial Segment Growth: Analysts are looking for a reacceleration toward 12% growth rates.

- DIY Retail: Focus is on stabilization of transaction volume after Q2 declines.

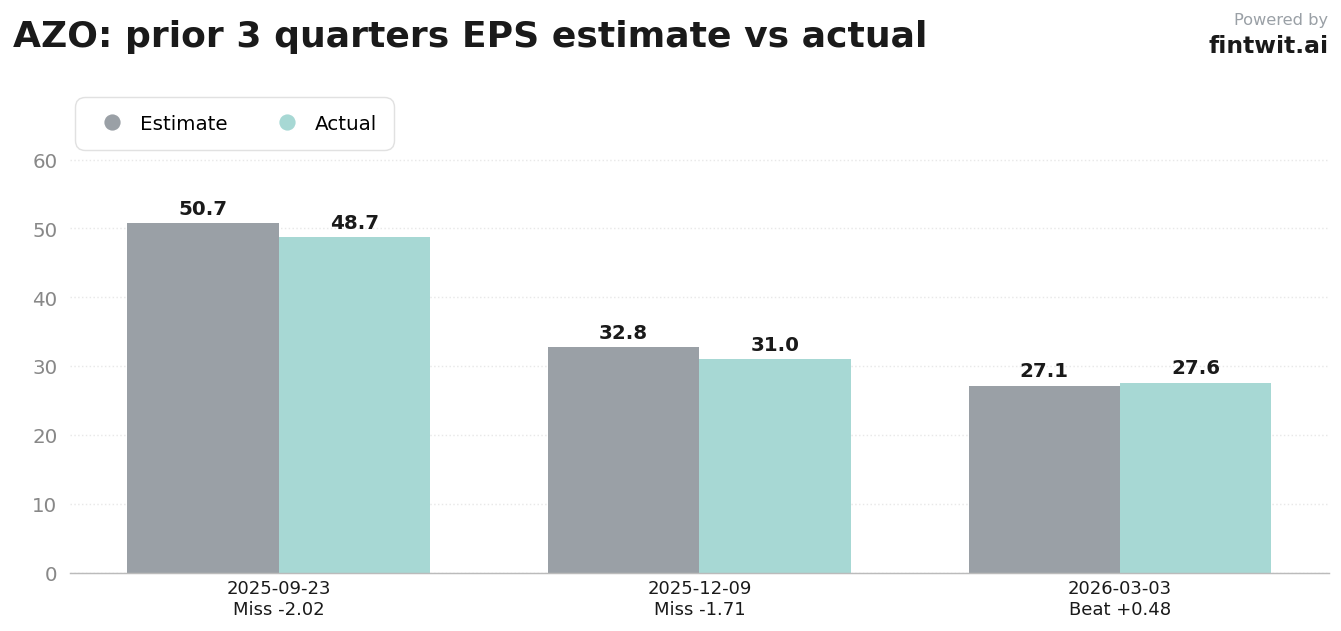

- Beat History: The company missed EPS estimates in the last three consecutive quarters.

What we'll watch on the call

Investors are looking for clarity on whether the commercial wholesale segment can successfully offset ongoing headwinds in the DIY retail space. The success of the Mega-Hub expansion strategy is central to this narrative.

Gross margin performance remains a focal point given the persistent tariff-related costs. Analysts will be listening for commentary on how these costs are being passed through to the consumer.

- Can commercial segment growth successfully offset ongoing DIY traffic headwinds?

- What is the expected timeline for returns on the current accelerated SG&A and CapEx investment cycle?

- How are tariff-related costs impacting gross margins beyond the anticipated LIFO charges?

- Justin Purohit of Seeking Alpha notes that while a spring rebound is expected, shares appear fairly priced.

Fintwit's AI verdict

The current market sentiment surrounding AutoZone is characterized by a tug-of-war between structural growth and margin compression. While the company's ability to capture demand from an aging vehicle fleet is well-documented, the persistent impact of LIFO charges and SG&A spending creates a complex valuation picture.

Our analysis suggests that the market may be underestimating the long-term efficacy of the current store expansion cycle. Investors should weigh the potential for a positive surprise against the backdrop of historical earnings misses.