Amazon.com Inc (AMZN) vs Walmart Inc. (WMT): Which Is the Better Buy in 2026?

Amazon's cloud-driven margin expansion faces off against Walmart's physical store efficiency. We break down the data to find the superior retail play.

The matchup

Amazon operates as a diversified technology and logistics conglomerate. Its primary growth engine remains AWS, which continues to benefit from enterprise AI infrastructure demand.

Walmart relies on its physical store network to serve as efficient fulfillment nodes. The company is currently scaling its advertising platform, Walmart Connect, to offset lower retail margins.

Both companies are competing for the same consumer wallet, but their underlying business models diverge significantly in profitability and scalability.

- Amazon Q1 2026 revenue growth: 17% YoY.

- Walmart Q1 2026 revenue growth: 7.3% YoY.

- Amazon's moat: Dominant cloud infrastructure combined with a massive e-commerce logistics network.

- Walmart's moat: Massive physical store footprint and deep grocery market dominance.

Numbers side by side

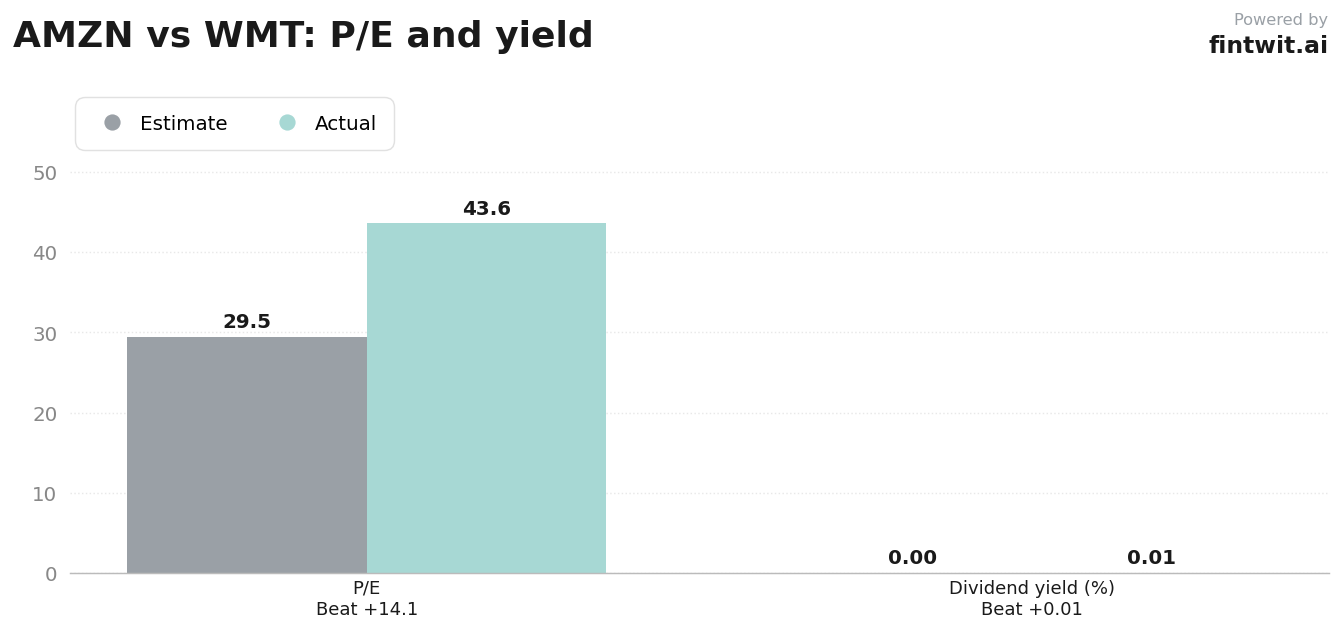

Valuation metrics reveal a clear divergence in how the market prices these two retail giants. Amazon trades at a P/E of 29.49, while Walmart commands a higher P/E of 43.60.

Amazon's recent performance shows a 13.26% return over the last year, compared to Walmart's 27.07% gain over the same period.

The following data highlights the fundamental differences in their current financial standing.

- Amazon Market Cap: $2.27 trillion.

- Walmart Market Cap: $948.88 billion.

- Amazon P/E Ratio: 29.49.

- Walmart P/E Ratio: 43.60.

- Amazon 90-day price change: 15.26%.

- Walmart 90-day price change: -3.85%.

- Walmart Dividend Yield: 0.78%.

Bull and bear on each

Analysts remain divided on the long-term trajectory of both companies. The bull cases center on margin expansion, while bear cases focus on capital expenditure and macroeconomic sensitivity.

Amazon's analyst consensus includes targets from $175 to $370, reflecting uncertainty regarding AI-related spending.

Walmart's analyst consensus ranges from $112 to $155, highlighting the tension between its retail stability and its pivot to digital advertising.

- AMZN Bull Case: AWS reacceleration driven by AI demand.

- AMZN Bull Case: Operating margin expansion via high-margin revenue streams.

- AMZN Bear Case: Massive AI-related capital expenditure pressure on free cash flow.

- AMZN Bear Case: Regulatory and antitrust scrutiny regarding market power.

- WMT Bull Case: Successful pivot to high-margin advertising and marketplace growth.

- WMT Bull Case: Omnichannel retail dominance and grocery resilience.

- WMT Bear Case: Limited pricing power due to value-based retail strategy.

- WMT Bear Case: Macroeconomic sensitivity and potential margin erosion from fuel and labor costs.

The verdict

Amazon's superior margin expansion potential, driven by its high-growth AWS and advertising engines, outweighs Walmart's stable but lower-margin retail-centric model. The structural shift toward higher-margin segments provides Amazon with a more robust path to earnings growth over the next 24 months.

Walmart remains a defensive powerhouse, particularly if macroeconomic pressures dampen consumer discretionary spending. In such a scenario, Walmart's grocery dominance would likely outperform Amazon's premium-heavy retail mix.